Good people, the Super Eagles coach has released the names of the 23 men who would represent Nigeria in Russia 2018 World Cup. As you study the names and how the coach would deploy them for glory in Russia, you may need to go back to the database of history. A new book – The History of Football in Nigeria – is available to help you. This book by Dr. Wiebe Boer chronicles our national passion in a very insightful and entertaining way. Get your copy here for N5,000.

The Book Summary

A Story of Heroes and Epics: The History of Football in Nigeria tells the hugely significant story of the rise of football in colonial Nigeria as a unifying cultural force in the country. The origins of the game in Nigeria, the history of organised football, the institutions that produced the early football stars, the first Nigerian players to play abroad, Nigeria’s first international matches, the earliest rivalries and narratives on football’s incursion into the southern and northern regions, are some of the subjects that form the basis of this incredible social history of Nigeria.

Lucid, entertaining and insightful, the writer introduces you to key historical characters ranging from the colonial officers, western missionaries and school principals to the Nigerian political leaders and founding fathers who influenced the rise of football as both a popular pastime and a unifying force for the country.

After undertaking the difficult task of researching Nigeria’s colonial era, conducting dozens of primary interviews, and collating documented history on the roots of football in the country from local and foreign archives, Dr. Wiebe Boer came up with a fabulous book that is destined to become an essential read for understanding Nigeria’s intriguing relationship with football and how the game has played such an important role in the construction of Nigeria’s national identity.

Everywhere we look, technology is being touted as the enabler of a new era of African agricultural prosperity. The exciting world of possibilities offered by blockchain, IoT, machine learning and the like has made companies, governments and policy-makers sit up and take notice of how such technologies can be applied to foster greater innovation, efficiency and economic and social progress.

But how should we as a continent approach the adoption of these technologies across the agricultural value chain – a process we commonly refer to as digital transformation – especially in an industry that the World Bank estimates employs two-thirds of the continent’s workforce and produce a third of its total GDP?

I would argue that quality data is the single most important building block toward establishing a smart agricultural sector for Africa.

Data feeds digital transformation in agriculture

The African agricultural sector is dominated by smallholder farmers. According to the International Fund for Agricultural Development, there are an estimated 500 million smallholder farmers in Africa and South-East Asia, providing as much as 80% of the food consumed in these regions and supporting up to two billion people financially.

Many of the difficulties these smallholder farmers experience are directly or indirectly related to the availability of quality information and data mainly because of infrastructure. Such data includes information about buyers and exporters; information about inputs, such as soil types, growing best-practice, weather, and pest control; information about markets, such as pricing and local, regional or global demand; traceability information related to food safety and certification to increase the market value of goods produced; information regarding storage and logistics; and access to financial services in the form of micro-loans or insurance.

In many instances, the lack of information has a direct impact on African smallholder farmers’ outputs and, by effect, livelihoods. Only 5% of cultivated land in Africa, for example, makes use of irrigation, compared to 38% in Asia, leading to lower yields and limiting their income-earning ability. And while agricultural performance has improved over the past decade, it is not yet sufficient to meet the demands of a population that is expected to grow by 1.3 billion people in Africa alone by 2050. A technological intervention is needed.

Reimagining Africa’s agricultural sector

According to a 2017 report by the Alliance for a Green Revolution in Africa (AGRA), the continent’s food system requires an agricultural transformation that is focused on more than just agricultural production and encompasses the entire food system. The report further points to promoting the growth of smallholder farms and SMEs involved in Africa’s food systems, and providing assistance to smallholder farmers that commercialises viable farm business prospects and capabilities.

One view to a smart agricultural sector involves establishing a sustainable and inclusive agricultural model that promotes equitable value distribution across the value chain; creates jobs; allows the increase of productivity and improvement of logistics and storage capacities while remaining cost-effective and respectful of the environment; and implementing and monitoring effective and efficient public policies.

We believe that the bedrock of such a model is the capturing in real time of all relevant data produced by each of the different stakeholders within the agricultural value chain, so that their decisions are as rational and efficient as possible. Here, technology has a clear role to play.

A technology platform designed for smallholder farmers

In 2009, SAP embarked on the development of a solution that would enable better management of smallholder farms by tracking and collecting data related to farms, cultivated plots (via GPS coordinates), crops, farmers, and farm gate selling processes. A prototype of this solution was developed in cooperation with the GIZ, a partner of the German Federal Ministry for Economic Cooperation and Development (BMZ), and piloted in 9 African countries reaching more than 100 000 small-scale producers.

Called SAP Rural Sourcing Management, the solution is operated in the SAP Cloud Platform and delivered as Software-as-a-Service to farmers who access it via their mobile phones, negating the need for costly technology infrastructure investment. Rural Sourcing Management is used by the world’s largest chocolate producer, Barry Callebaut, and the Kalangala Palm Oil Grower’s Trust in Uganda, where 80% of the population is involved in agriculture.

The Rural Sourcing Management solution is helping the KOPGT grow and expand, improve efficiency, and keep all major players in the value chain connected digitally. This is shining a path toward prosperity in Uganda and supporting the government in its aspirations of moving its citizens to a middle-income status by 2040. We believe that by providing African smallholder farmers with technology tools designed to improve their day-to-day farming operations, we are creating an ecosystem of benefits across the agricultural value chain that will take the continent one step closer toward realising a brighter and more food-secure future for generations to come.

Dr Gilbert Saggia was speaking at the 2018 Smart Agri Congress Africa held in Nairobi, Kenya.

I am in Brussels, the heart of Europe and would be working here all through the week. The event I am attending began yesterday. It is a carnival to examine innovation and build pillars and models for growth in Europe. When I checked into the hotel which the European Commission had booked for me, my name popped up: the associate said “Welcome, you are a regular”. Yes, I have been coming to this event and Europe did great, upgrading me from Business Class to First Class this time. Certainly, they do appreciate the value we are adding through Fasmicro Group (my company) and African Institution of Technology (my non-profit).

Today, we had a conversation with some of the leading European Banks. It was coming out of the open banking legislation in the United Kingdom. In my talk, I presented three core pillars (and product frameworks) for what I have called Platform-Banking Era. (I will not share that publicly, yet, as I have a talk coming up in South Africa with clients and would not want it to be boring to them. They need to hear me live first before the “declassification”).

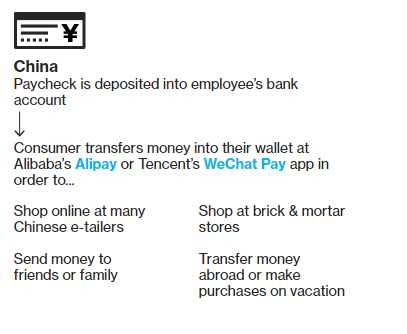

Tomorrow, I will be speaking on the nature of work and the day after, I will talk on global technology. Most times, I present the fusion of global and Africa, helping those without African operations to understand how change is happening. For example, MPESA remains a mystery and WeChat confuses many bankers in Western hemisphere.

Banks Never Make a Cut

The future of consumer payment has been built in China. Yes, Alipay and WeChat have demonstrated that digital companies can build a payment system where no bank could get a cut of the action. That is just the beginning.

The future of consumer payments may not be designed in New York or London but in China. There, money flows mainly through a pair of digital ecosystems that blend social media, commerce and banking—all run by two of the world’s most valuable companies. That contrasts with the U.S., where numerous firms feast on fees from handling and processing payments. Western bankers and credit-card executives who travel to China keep returning with the same anxiety: Payments can happen cheaply and easily without them.

Even as Nigerian banks are falling over themselves to work with Visa and MasterCard, China has already moved past the era of cards. And I do think the future is going to be where no one would need a debit or credit card to do consumer transaction. Simply, banks would be the entry elements into the ecosystems and once the money is there, customers can move the money to their digital wallets from where they would pay for things. As they do that, there would not be a need to do anything with banks. If that happens, banks become dump pipelines just as telcos have become dump pipelines for Skype and WhatsApp. That would happen if the banks do not take actions. It happened in China, and many banks have paid heavily with erosion of value.

WeChat payment process (source: Bloomberg)

The interesting thing in WeChat and AliPay is that they are making it easier for users to stay longer in their ecosystems through different solutions, services and products they offer to customers. And if they do just that, the need for the typical banking fades. This is already causing major problems with some small Chinese banks where liquidity has become a challenge.

Specifically on that, the Chinese banking regulator has to request that the BAT( Baidu, Alibaba and Tencent) move funds from their wallets to their bank accounts within 72 hours as local banks were having liquidity issues [yes, that does not help local banks. It only helps the banks where the BAT bank].

Alipay and WeChat command 520 million and one billion monthly active users, respectively. Together, both moved $2.9 trillion in 2016. That number has been estimated to be excess of $3.5 trillion for 2017 [the companies do not disclose the numbers].

The Nigerian Opportunity

The payment system in Nigeria is anchored on our banks. That is expected as we are mirroring U.S. and Western Europe in our strategy. That is why every payment connects back to banks, from cheque, debit, credit (where available) and fintechs. For the fintechs, the systems are largely designed to tie directly to the banks. The implication is that it is still the banks. The element of abstraction and disintermediation is not real because our banks are still at the center of the hubs.

Breaking that hold on banking is where the opportunity lies. But it would not be easy. Anyone that does that in Nigeria would win it all. The Chinese experiment makes that very clear. Yes, I am not sure we hear of Chinese banks, but we know of WeChat and Alipay because these ecosystems are huge and growing.

In Africa, Facebook and Instagram are potential suspects if regulations would allow them. They are already working with Nigerian banks.

The banks are doing what they have to do: with Facebook Corp, there is no other alternative – you either fall in line or you go extinct. This is going to be the future of banking in Nigeria. No one goes to a bank in China; most go to WeChat to do banking. Facebook has a plan for that in Nigeria. The plan is now under execution.

Yet, besides the technology, one has to change the attitude of Nigerians. For this to work, Nigerians would be open to park their cash into apps from their bank accounts. That may not be easy; we are yet to become believers of digital ecosystems [blame Yahoo boys for that]. But where that happens, it means the digital ecosystems would use that money to lend, extending their powers over banking institutions.

Meanwhile, Chinese consumers are starting to park more of their savings with the apps. In 2013, Alipay began offering money-market accounts. By last year, it had built that business into the world’s largest money-market fund with about $243 billion. For banks, that’s yet another bite. They traditionally hold customer deposits and use that money to fund loans—generating significant profits. If U.S. consumers were to start storing their extra cash with apps, banks would have to find an alternate—probably more expensive—source of funding.

This Will Make You Very Rich

If you are looking for wealth online, do not look further: a platform like WeChat is what will deliver the glory. Just as MPESA in Kenya is trying to transmute its solution into an ecosystem, expect many Nigerian banking apps to have the same plans. GTBank (Nigeria) wants to do the same thing as noted in its grand strategy by the CEO. Yes, GTBank wants to meet your basic needs, not just the banking needs, digitally.

To “create a platform and partner anybody who has a service to offer. So that if as a customer, one comes into our ecosystem, you can do just anything. You could do your banking business, buy your tickets, insurance, travel; if you wanted a 10-day pay day loan, you can do it. So, really we want you to come into our ecosystem, maybe five times a day to do different things other than banking.”

You would have to beat Mr. Segun Agbaje [very tough indeed] if you want to get the glory. But what needs to be done is very clear: banking will be part of social connections, and going forward, would not be measured by one-off transactions, at consumer level.

List of Nigeria's 23-Man Squad to Russia 2018 World Cup

The coach of the Super Eagles of Nigeria, Gernot Rohr, has released the names of the 23 men he has chosen to represent Nigeria in the Russia 2018 World Cup.

Goalkeepers: Ikechukwu Ezenwa (Enyimba), Daniel Akpeyi (Chippa United) and Francis Uzoho (Deportivo La Coruna).

Defenders: William Troost-Ekong (Bursaspor), Leon Balogun (Brighton and Hove Albion), Kenneth Omeruo (Kasimpasa), Bryan Idowu (Amkar Perm), Chidozie Awaziem (Nantes), Abdullahi Shehu (Bursaspor), Elderson Echiejile (Cercle Brugge) and Tyronne Ebuehi (Benfica).

Midfielders: John Obi Mikel (Tianjin Teda), Ogenyi Onazi (Trabzonspor), John Ogu (Hapoel Be’er Sheva), Wilfred Ndidi (Leicester City), Oghenekaro Etebo (Las Palmas) and Joel Obi (Torino).

Forwards: Odion Ighalo (Changchun Yatai), Ahmed Musa (CSKA Moscow), Victor Moses (Chelsea), Alex Iwobi (Arsenal), Kelechi Iheanacho (Leicester City) and Simeon Nwankwo (Crotone).

Nigeria is in the same group (D) with Croatia, Iceland and Argentina.

List of Nigeria’s 23-Man Squad to Russia 2018 World Cup

MTN Group is a South Africa-based category-king multinational mobile telecommunications company with presence in many African, Asian and European nations. It is a leading Africa brand, serving approximately 221.3 million people in 22 countries. Its vision is to deliver a bold, new digital world to its customers. MTN Nigeria is the leading mobile operator in Nigeria with approximately 54.5 million subscribers. According to reports, about 30% of MTN Group’s revenue comes from its Nigerian operation where it holds at least 35% of the market share. For financials of MTN Nigeria, I have analyzed them here: the company (i.e. MTN Nigeria) made either N81.4 billion or N248.3 billion in Q1 2018 depending if you believe the Group financial report published in the Johannesburg Stock Exchange or another report hosted by MTN.

What is the Value of MTN Nigeria?

As MTN Nigeria plans to list on the Nigerian Stock Exchange, investors would model how much the company is worth. I did try using available numbers in the past here.

Option A: I concluded that MTN Nigeria would be worth $4 billion (30% of the company would be $1.2 billion).

So, if MTN Nigeria should sell 30% of its value and MTN Ghana sells 38% and both generate $1 billion, I would see that as a discount. Let us assume that MTN Ghana brings in $300 million while MTN commands $700 million. Using that we can say that 30% of MTN Nigeria is $700 million. (Bloomberg noted $500 million for 30% though that was not the most current number on this).

But from 9Mobile sale price (not certain until it is done), I had modelled 30% of MTN Nigeria to command $1.2 billion. So, if they are going for $700 million, it means MTN Nigeria is coming at a big discount. If that is the case, investors would go for it.

Option B: I used the market cap of MTN Group to arrive at the value of MTN Nigeria (MTN Group market value has lost value since the piece was published but it is insignificant to change the analysis).

About 33% of MTN Group revenue comes from Nigeria. Also, Nigeria commands more than 25% of its total subscriber base. Largely, Nigeria is perhaps the most profitable market for MTN Group. If you take the subscriber base alone, you can put MTN Nigeria at a market cap of $4.25 billion (25% of the $17 billion). By the time taxes are taken, the value of MTN Nigeria can down as $4 billion.

MTN Group market cap, June 2018 (figures in Rand)

MTN Nigeria Value – Reuters

This piece from Reuters provides solid numbers on the value of MTN Nigeria: $5.23 billion.

MTN plans to list its Nigerian unit worth $5.23 billion by July in a debut IPO on the Lagos bourse and will raise fresh funds to reduce debt, according to pre-IPO presentation seen by Reuters.

[…]

MTN shares are currently traded over-the-counter in Nigeria at $13, giving it a market value of $5.23 billion, down from $25 billion in 2015 before a Nigerian government fine, sources said.

MTN Ghana – Updated

This is the most authentic data we can use since MTN Ghana had indeed filed the paperwork with the regulators. It is selling 35% of the business for $745 million. Certainly, the old reports are wrong since MTN cannot be seeking $1 billion from both Nigeria and Ghana, and Ghana is contributing already $745 million.

Through the Initial Public Offer, MTN Ghana seeks to raise about of GHS3.48 billion (over US$745 million) with each share sold at GHp75. The offer is expected to end on July 31 and possibly list on the Ghana Stock Exchange on September 5, 2018.

MTN Ghana on the 20th of April, 2018, received approval from regulatory bodies including the Securities and Exchange Commission (SEC), Ghana Stock Exchange (GSE) and the Ghana Investment Promotion Council (GIPC) to proceed with the 35 per cent IPO which forms part of MTN’s 4G LTE license requirement in which the company had to sell 35% of its shares to Ghanaians by June 2018.

MTN Nigeria Value

MTN Ghana has 17.8 million subscribers and commands a market share of 47.6%. MTN Nigeria has 54.5 million subscribers with a market share above 35%. Neglecting the market positioning and focusing on the subscriber base, 35% of MTN Nigeria should give 3.06x of the $745 million from Ghana (i.e. $2.3 billion). With this number, MTN Nigeria would be worth $6.57 billion. But since MTN Nigeria does not have the same market positioning as it has in Ghana (48% vs 35% market share), we would drop $1 billion from the number. That brings the market value of MTN Nigeria to be $5.57 billion. Post-IPO, that would give it about 13% of the total value of the Nigerian Stock Exchange, depending on the exchange rate you use.