We do get a lot of emails through our works in the non-profit African Institution of Technology. Also, I get questions regularly via LinkedIn from founders and entrepreneurs. But recently, I have noticed a pattern from our young African entrepreneurs especially the female founders: they tend to think that their works are inferior. That is a big problem which has to be addressed.

Why it is desirable to benchmark, in my experience, the best way to achieve any greater state is to have self-confidence. There is a huge difference between pursuing perfection and thinking that you cannot even compete. Sending us a link and immediately pointing out a Silicon Valley company that does what you are trying to do better will not really help your personal drive. While you can learn from the Silicon Valley company, your motivation must come with understanding that you can adapt the idea to meet the needs of a local market.

I call this problem Comparative Inferiority where people are always comparing themselves with others and always putting themselves at a lower barometer. You think you went to the wrong school, you worked in the wrong company, and came from the wrong country. Get a break! The biggest asset in your company is not your history: it is you. And the future is unbounded and unconstrained. The implication is that despite any past, you can achieve what you have dreamt for your company. But that can only happen if you believe. Beginning with the mindset of being inferior will put you in a position to lose even before the game starts. Confidence is not an absence of weakness. It is simply a testament that you have made progress despite the obvious fact that you have more works ahead.

In this video, I address that Comparative Inferiority. My thesis is that people have to be confident in any state they are, even as they pursue a higher state. You have already achieved something by starting something. Your work is not inferior but it can be improved upon. You need to find a way to communicate confidence and put brilliance in your work even when you are not satisfied of its current state, knowing that you need to continue to improve.

If you know the edge people you are comparing yourself have, you will certainly appreciate how far you have come. They need to inspire you, motive you but you must not be intimidated by them. I want legends to inspire you. But you must not be intimated by them.

Guys…let’s not pretend you don’t know what this post is going to be about. Anyone who has worked in, or run,a small business has felt the urgly sting of inferiority complex to their largest rivals at some point. Sure, having your own business is liberating and rewarding and a life changing. But sometimes it would be nice to get corporate card back and walk into a new business opportunity knowing without a doubt that everyone in the room had already heard of your company.

Of course, that’s an overly Rosy picture of what it is to work for a large company – but you get the picture. The thing is, when it comes to this infiriority complex that many small business owners and employee might feel, it typically only comes down to three things: Perceived lack of size, Perceived lack of experience, and perceived lack of resources. The irony of each of these is that what is holding you back from confidence in your own business in each area is probably the same thing that is making that issue a barrier for your business in the first place.

The good news about that is if you can Address this question for your potential customers, you can likely solve it for yourself and your staff as well. Let’s tackle each of them one by one….?

Bottomline: In this piece, I present five phases which are necessary to build high performing technology-enabled companies in Africa. Indeed, the thesis goes beyond technology but to any specific industrial sector. I also explain that one of the key elements of high performing companies is arriving in the market with new ways of doing things. […]

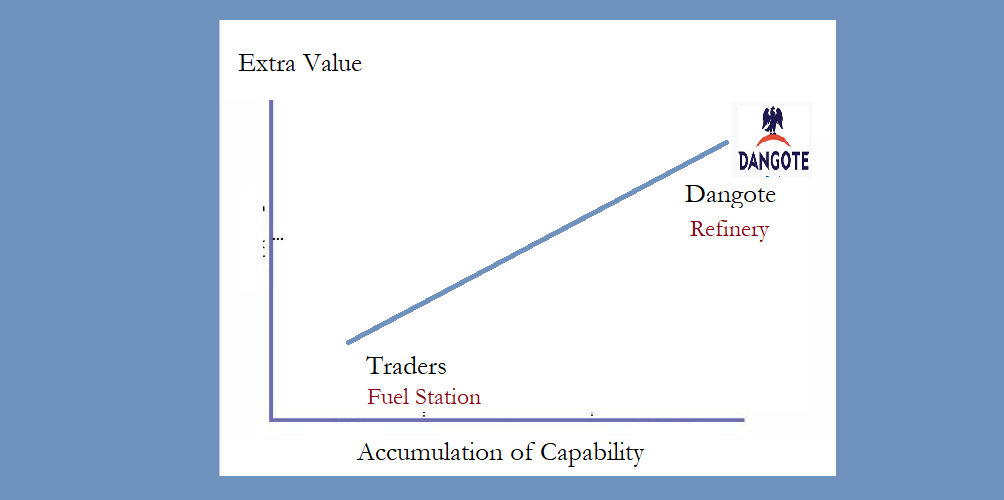

In these videos, I explain the Accumulation of Capability Construct and how makers of Indomie Noodles used the same strategy which Aliko Dangote uses in Africa to defeat Dangote Group in the noodle business. I did make a case that anyone can use the same technique to execute a winning strategy in business. The key is operating at the upstream level of business. Read this interview from APO newswrie: Dangote essentially validates what I had noted on his business philosophy.

At the Financial Times’ 4th annual Africa Summit at Claridges in London, editor in chief Lionel Barber conducted an extraordinarily candid public conversation with Nigerian Aliko Dangote, Africa’s most successful business leader, …

Mastering detailed production statistics and highly-compelling demographics on promising sectors of the African economy, Dangote outlined the key to his success: self-sufficiency and backward integration, a manufacturing strategy that extracts value from entire processes. “We are not going to import anything any longer,” he said. “In Nigeria we are learning how to produce the entire value chain.” Once a heavy importer of fertilizer, Nigeria is now gearing up to produce 3M tonnes of locally manufactured fertilizer, transforming the nation into one of the largest fertilizer exporters in Africa.

In 2007 Nigeria was the second largest importer of cement after the US, Dangote reminded the audience of business elites. “Today, we have not only satisfied domestic needs; we have become a leading exporter of 6-7M tonnes of cement,” he added.

Diversifying into agriculture, Dangote has eyes on the dairy industry motivated by the fact that “98% of all milk consumed in Nigeria is imported.” Same for rice. Dangote Group has invested heavily in rice production by investing in local farmers and then offering to buy back the 1M tonnes at open market prices that they are growing. “Soon we will be able to feed not only Nigeria but the entire 320M large West African market.”

Dangote’s business accumen was on rare exhibition as FT editor Lionel Barber himself seemed impressed with the business mogul’s quick familiarity with the nuts and bolts of his businesses. “Are we going to continue to import everything?” Dangote asked. “Freight rates are now cheap but they will go up soon. A population of over 200M cannot continue to import basic needs on a daily basis,” he answered himself.

By 2100 Dangote stated Africa will represent 49% of the world’s population, up from 30% today. “If you don’t think big we won’t grow at all,” he said. “In Africa you have to play long-term.”

Aside from Nigeria, which African nations do you think are good growth opportunities? Barber asked Dangote. “Aside from Nigeria?” the business leader repeated and smiled. “I’d have to pick Nigeria. I am a big fan of Nigeria. We are only using 8% of our land.”

Simply, Dangote is attacking all the elemental production phases, looking for values. By the time he has improved and perfected them, removing all possible wastes and inefficiencies, no new player can find further avenues to compete. By going to rice farming, he makes sure that he can control the value chain and improve the whole production systems of rice. He will improve the rice farming business and remove any inefficiency therein. Once done, a competitor cannot enter the market through that angle.

Dufil Prima Foods, the maker of Indomie, built schools, invested in farming, produced their electricity, etc making it nearly impossible for any further improvement to have material impact on noodle pricing. Through the efficiency they have in the system, there is nothing left for Dangote Group to improve upon. Unlike in the past, Dangote Group could have reduced cost through electricity generation, raw material production, distribution etc. But Dufil had done all those things. In other words, when Dangote Group joined the noodles business, it was essentially doing what makers of Indomie were already doing.

But Dufil had more scale with a known brand. It has all the advantages and there was nothing Dangote Group could do. Over time, Dangote Noodles sold to Dufil.

We have shifted the date for the launch of the Cybersecurity Africa book to Oct 30th. One of the technical reviewers could not finish on time. He is a Chief Information Security Officer in an African bank and certainly has his main priorities. The other reviewers came on time. So, we have given the CiSO more time, and he is certain he would round up on time for us to launch by Oct 30, 2017.

Over the last eighteen months, I have noticed a clear architectural redesign in the Nigerian banking sector. Our banks are increasingly playing at higher levels with innovations in the mobile space. While new fintech (financial technology) companies continue to focus on payment and remittance sub-sectors, a new dimension has also started emerging. With Paylater,ng and Piggybank, we now have startups providing small loans to Nigerians without deep collateral burdens. Depending on how you see it, these startups are pioneering a new age in Nigeria’s financial sector: a credit-based economy.

The decision by the Central Bank of Nigeria (CBN) and the Bankers Committee to establish the Bank Verification Number (BVN) is producing a clear virtuoso moment in the banking sector. While Nigeria may not have the equivalent of the U.S. FICO score which scores citizens’ credit worthiness, we do now have histories of financial transactions of citizens via NIBSS (Nigeria Inter-Bank Settlement System Plc). This makes it easier to take lending risks with these citizens, even without collateral as you can easily model their re-payment capacities. Prior NIBSS and BVN, our banking industry had no memory of these transactions even though they were occurring. The push to cashless society by the central bank is a strategy that is going to pay positively for Nigeria in many ways.

Paylater with the CBN certification has access to BVN of customers. It is possible that it evaluates credit worthiness through data pooled from NIBSS (Nigeria Inter-Bank Settlement System Plc) which handles transaction details of Nigerian bank customers. .

With the knowledge of the citizens’ financial transactions, small credits can be given to them. I also believe that the companies will also build credit profiles of these citizens as they take the loans and repay. Though there is no national harmonized system for this, BVN provides a trusted apparatus to leverage to build credit-based solutions. This is still at infancy, but the foundations are very noticeable to any ardent observer: the dawn of a credit-based economy is being built right now in Nigeria.

A New Era in Nigerian Banking

One of the most important companies in Nigeria in the area of digital banking is Interswitch. Interswitch is now taking action to take advantage of its position in the sector and lead the acceleration of what Paylater and Piggybank are doing. The Nigerian digital payment pioneer is working with six banks and three startups to begin a new era in Nigerian banking sector. The banks will provide the data while the startups will help deliver the products. Interswitch will stay at the back to make sure the data integrity is there. It will also over time build the credit score. The product is named Interswitch Lending Services (ILS). ILS is a very powerful product in the Nigerian financial sector which can bring many citizens into the sector through micro-lending and financial inclusion.

To bridge the gap in accessing unsecured short-term micro-loans in Nigeria, Interswitch in partnership with six lending banks and three innovative credit providers has introduced a lending services platform.

The lending platform, named Interswitch Lending Services, is an intervention, which essentially resolves the challenge by providing credit analysis and scoring based on customer historical transaction data which bank and non-bank credit providers can leverage to provide collateral free micro and nano loans to individuals and small businesses across the channels

This is going to become the most important product Interswitch will be launching. I do expect ILS to be bigger than the present Interswitch, and over time, may have the present Interswitch folded into it. If the company executes this well, it will have the most important product in the Nigerian financial sector. Nigeria’s credit sector is untapped and any leader that pioneers it will reap huge benefits.

Interswitch has accumulated capabilities with products like Verve (credit: pulse)

It is starting with FirstBank, UBA Bank, Heritage Bank, Unity Bank, Fidelity Bank and Ecobank. The lending partners are Paylater, Kwikcash and Ferratum. I expect the pool of the banks to expand in coming months. There is no need for a bank to be outside this league. Yes, it needs to cover all the banks. Provided it is working with NIBSS, ILS can have a very good view of any Nigerian banking customer, preparing the data for the lending partners to make loan. Possibly, the partner banks will have only their customers participating initially.

The Interswitch Tax

ILS is leapfrogging here with no need for brick-and-mortar credit system, moving immediately to the digital-first domains. Internet is going to anchor this vision with the unbounded distribution channels it offers. This makes this product scalable. ILS will serve as an aggregator of data. ILS is a pure aggregation construct business with a high scalable advantage. It aggregates data created by banks and using that data to package a product used by the lending partners. With Internet, the marginal cost of this business goes low which makes it extremely scalable, for Interswitch. As it accumulates more data, ILS gets better and grows. This becomes a positive continuum. The end result is a virtuoso circle of innovation that will have implications in the Nigerian banking sector especially in the retail space. All banks will join and just like that Interswitch Lending Service will become the national credit bureau. With that, everyone will pay Interswitch tax, to tap into that data. ILS may consider some of my suggestions as it becomes a vehicle for the new financial system of Nigeria.

The alignment of the interests of the banks, credit bureaus and citizens will be catalytic in establishing a functioning credit ecosystem in Nigeria. This is not included in the current CBN’s guidelines for establishing credit bureaus in Nigeria. We cannot do it the way the Americans have done it. We need a system that provides a citizen element so that credit bureaus have clear incentives to deliver good services. You cannot be selling people’s data and yet have no incentives to serve the people and protect their data. With this proposed model, the oligopolistic system that runs in the credit bureau industry will be dismantled in the Nigerian model. The outcome will be a virtuoso credit bureau system that secures customers data as it serves its core customers, the banks.

The Aggregator-Bank

With the use of BVN, in future, loans can be offered to non-bank customers. All ILS has to do is to synchronize the BVN of a customer with its phone data. And through the phone, it can even offer loans. So, you can see people getting small loans delivered through their mobile phones with phone/recharge card agents becoming cash agents. The key thing here is the availability of data which provides deeper insights. Banks are not necessarily critical to execute this, though they will be important to initiate it. Interswitch makes that clear in its statement when it noted that “non-bank lenders” can be supported. If Interswitch can effect the loans to non-bank customers, it simply means that it is indeed a bank! But a better bank without the burdens of capital adequacy and financial ratios usually imposed by the regulator, the CBN. Sure, Interswitch is already an entity registered and regulated by CBN, but of course, not as a bank.

The solution focuses on enhancing financial inclusion by providing a tested and reliable end-to-end credit administration infrastructure, which is open and flexible enough to accommodate both bank and non-bank lenders.

The Platform has been integrated by Interswitch to what is perhaps the largest customer database, allowing almost 16 million Nigerians (which includes active customers on Quickteller) to be assessed for possible qualification for a loan. Interswitch had formed strategic partnerships with a number of credit providers to efficiently target customers who are available on those partner platforms, offering nano-loans at attractive interest rates and based on available credit history and predictive analytics through information technology to determine credit-worthiness

Under the aggregation construct, the lenders take the risks. Others supply the data; ILS simply aggregates and packages the data. This positions this company to become one of the most important firms in the nation in coming years. Interswitch is playing at the upstream here, relying on its downstream partners in the Interswitch ecosystem and 16 million people in its database. It has a brilliant vision.

The $1 Billion Business

Interswitch is now moving on its vision to become a truly indigenous unicorn, technology-enabled business with at least a billion dollar in valuation. I do think an effective execution of this business model will put it in that league. ILS will not just grow revenue; it will also bring more customers to the Interswitch ecosystem. Watch out for growth in Interswitch associated debit cards, quickteller and businesses of its bank partners. People will begin to make decisions on how they can be in ILS network in order to build histories that will qualify them for loans. The company will execute this growth at largely minimal risks. The lending partners take the risk but benefit through expanded access to higher pool of customers. The banks will also get a cut for providing the data. Over time, I expect some of the banks to open their own micro-lending products to compete with Paylater and others. At the moment, the business may be small for the cost model the banks can effectively serve. For the banks to play here, especially in the sub-one million naira credit services, they will need to build new ways of doing things. They will have to become more digitalized to save business costs, and serve customers who are usually not within their crosshairs.

All Together

Interswitch has accumulated capabilities in the digital payment sector over the last few years. Now, it is unleashing that data, creating new products. Interswitch has the capability to change the basis of competition in the Nigerian banking sector. That will be transforming and disruptive. It is at the edge of a smiling curve and is just getting started. When companies accumulate capabilities, they see themselves operating in the segments of markets with higher value (usually upstream) compared with where their lower-end competitors operate (usually downstream). In the Nigerian financial sector, Interswitch has moved upstream and is extremely positioned to control most elements of the financial systems with the data it controls.

The internet business is not necessarily who generates the most data. It is who can make sense of it. Aggregators like Interswitch are at the centers making sense of all the data passing through the financial system. Google does that for our web businesses. It waits for us to create the contents. It then aggregates them and serves them to its customers and advertises, abstracting the content creators. Facebook does the same to our photos and feeds, providing a platform for us to post them. It then serves them to our friends and families. Because the data is too much, the value is not really about who has the most data, but who can make sense of the data which is constantly changing in volume, variety and velocity. That is where Interswitch has an advantage over the banks as it can see everything going through its networks from multiple players. You may decide to work with First Bank or GTBank, but those will give you a partial view of the data. Interswitch delivers more and that is why we do not visit BBC or New York Times for major news, we go to Google which then curates and prepares the best content for us. Google has access to all new networks in the world, making sense of the best to serve you. BBC and NY Times are limited even though they could be one of the companies Google will have as destinations. The BBC and NY Times have been abstracted out by Google. Today, Interswitch is doing same for the banks when it comes to retail lending. NIBSS seats at even a better position than Interswitch since all BVN banking data go through NIBSS.

I am so happy for this Interswitch strategy. I wrote many months ago that it should buy Unity Bank to get into lending. It has simply done it in a better way without spending any money. Also, it is not taking any risk. But it is clearly seeding a new era in the Nigeria’s financial sector.

Interswitch should acquire a lending license from Unity Bank. That will help it begin to build a credit system in Nigeria in partnership with NIPSS. Post-acquisition, it will focus on digital banking, closing some branches of Unity Bank and dedicate its efforts to build Nigeria’s first internet-only bank. Through this, the bank will use the data from its ecosystems to perfect lending systems which will help drive it growth.

With small blessing from NIBSS, it provides a clear roadmap to the future of Nigeria’s credit-based economy. The hangover is over, this digital pioneer is back and that is a good thing for Nigeria.