In mid November, FTX International became effectively insolvent. The FTX saga, at the end of the day, is somewhere between that of Voyager and Celsius.

Three things combined together to cause the implosion:

a) Over the course of 2021, Alameda’s balance sheet grew to roughly $100b of Net Asset Value, $8b of net borrowing (leverage), and $7b of liquidity on hand.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

b) Alameda failed to sufficiently hedge its market exposure. Over the course of 2022, a series of large broad market crashes came–in stocks and in crypto–leading to a ~80% decrease in the market value of its assets.

c) In November 2022, an extreme, quick, targeted crash precipitated by the CEO of Binance made Alameda insolvent.

And then Alameda’s contagion spread to FTX and other places, similarly to how Three Arrows etc. ultimately impacted Voyager, Genesis, Celsius, BlockFi, Gemini, and others.

Despite this, very substantial recovery remains potentially available. FTX US remains fully solvent and should be able to return all customers’ funds. FTX International has many billions of dollars of assets, and I am dedicating nearly all of my personal assets to customers.

JUST IN: ?? Bahamas Securities Commission says it's holding FTX deposits worth over $3.5 billion.

— Watcher.Guru (@WatcherGuru) December 30, 2022

Notes

- Here is my record of FTX US’s balance sheet as of when I handed it off:

FTX International was a non-US exchange. It was run outside the US, regulated outside the US, incorporated outside the US, and took non-US customers. In fact, it was primarily headquartered, run from, and incorporated in The Bahamas, as FTX Digital Markets LTD.

US customers were onboarded to the (still solvent) FTX US exchange.US Senators have raised concerns about a potential conflict of interest from Sullivan & Crowell (S&C). Contrary to S&C’s statement that they “had a limited and largely transactional relationship with FTX”, S&C was one of FTX International’s two primary law firms prior to bankruptcy, and were FTX US’s primary law firm. FTX US’ GC came from S&C, they worked with FTX US in its most important regulatory application, they worked with FTX International on some of its most important regulatory concerns, and they worked with FTX US on its most important transaction. When I would visit NYC, I would sometimes work out of S&C’s office.

S&C and the GC were the primary parties strong-arming and threatening me into naming the candidate they themselves chose as CEO of FTX–including for a solvent entity in FTX US–who then filed for Chapter 11 and chose S&C as counsel to the debtor entities.

Despite its insolvency, and despite processing roughly $5b of withdrawals over its last few days of operation, FTX International retains significant assets–roughly $8b of assets of varying liquidity as of when Mr. Ray took over.

JUST IN: ?? Bahamas Securities Commission says it's holding FTX deposits worth over $3.5 billion.

— Watcher.Guru (@WatcherGuru) December 30, 2022

-

In addition to that, there were numerous potential funding offers–including signed LOIs post chapter 11 filing totaling over $4b. I believe that, had FTX International been given a few weeks, it could likely have utilized its illiquid assets and equity to raise enough financing to make customers substantially whole.

Since S&C pressured FTX into Chapter 11 filings, however, I worry that those pathways may have been abandoned. Even now, I believe that if FTX International were to reboot, there would be a real possibility of customers being made substantially whole.

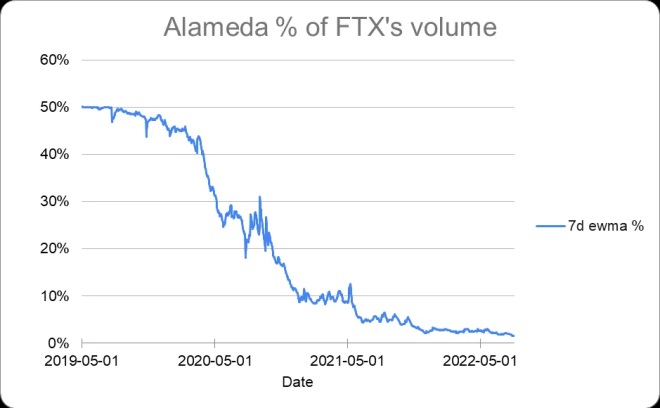

While FTX’s liquidity had started off in 2019 as largely dependent on Alameda, by 2022 it had greatly diversified, with Alameda falling to around 2% of volume on FTX.

I didn’t steal funds, and I certainly didn’t stash billions away. Nearly all of my assets were and still are utilizable to backstop FTX customers.

I have, for instance, offered to contribute nearly all of my personal shares in Robinhood to customers–or 100%, if the Chapter 11 team would honor my D&O legal expense indemnification. FTX International and Alameda were both legitimately and independently profitable businesses in 2021, each making billions.

And then Alameda lost about 80 percent of its assets’ value over the course of 2022, due to a series of market crashes–as did Three Arrows Capital (3AC) and other crypto firms last year–and after that its assets fell even more from a targeted attack. FTX was impacted by Alameda’s decline, as Voyager and others were earlier by 3AC and others.

Note that, in many places here, I’m still forced to make approximations. Many of my personal passwords are still being held by the Chapter 11 team–to say nothing about data. If the Chapter 11 team wants to add their data to the conversation, I would welcome that. Also–I haven’t run Alameda for the past few years.

So much of this is pieced together post-hoc, coming from models and approximations, generally based on data that I had prior to resigning as CEO and modeling and estimations based on that data.