Do not waste your time on music streaming business (music-tech). It has a lousy unit economics which makes it very challenging to attain profitability. Though video business is very technically challenging (those bandwidths and associated costs), music streaming business is terrible if you do it as the only business. But where you use it to sell hardware like Apple does, there is no issue. I have made this case before. The problem with music is the way you acquire the products. Unlike video which is not bounded to the number of users [you buy the rights and it is not tied to the number of people that watch the video], music pricing is directly linked to how many listen. It is the IP system’s fault which seems to protect music more than anything. But it makes music-tech entrepreneurs to be in challenging positions.

Running a business that streams video will always be a better business than one that streams music. The reason is simple: marginal cost. As I explain here, when you pay for video rights, it is uncorrelated to volume watched. But for music, your cost changes depending on the number of listeners. So, more listeners more royalties even though you may enjoy discount which improves unit economics. If a Zen master comes to you and offers these: take one of these startups – one streams video, the other music. Go with video. You have a better chance of scaling faster and making money. You see, you may need to take accounting class as your success can be bounded by unit economics even before you begin.

And many others have made similar points also.

The upshot is, no matter how many subscribers they add, the companies will never enjoy the fat profits of other tech firms. Right now, the streaming services have yet to make any money and, if they ever do, it’s a safe bet the music industry will find a way to claw it back in the form of higher royalties. It’s much like the baker being totally beholden to a flour supplier that raises its prices every time donuts are on the verge of being profitable

Do not worry about Spotify, its market is different from Africa. It can keep losing money because it can keep getting new ones to spend. But where you need to build as we do in Africa with path to profitability, you cannot recreate Spotify easily. Spotify has lost about $1 billion in the last two years. It “reported a total operating loss of €41 million ($49 million)” in Q1 2018.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

Spotify stock officially opened at $165.90 per share, fluctuating briefly in afternoon trading before closing at $149.01 per share. This closing price valued Spotify at $26.5 billion, which ranked it as the eighth-largest tech IPO after one day of trading, directly behind Google and and Snap, according to Dealogic. Since then, the stock has climbed as high as $171.23 per share and dipped as low as $135.51 per share.

Simply, this type of business (music streaming) will not thrive in Africa – no one will give you that kind of money to be losing. That was what brought Konga, a pioneering Nigeria’s ecommerce company which was sold, down! No matter how you see it, this is the summary of music-tech (streaming) business model: keep losing money!

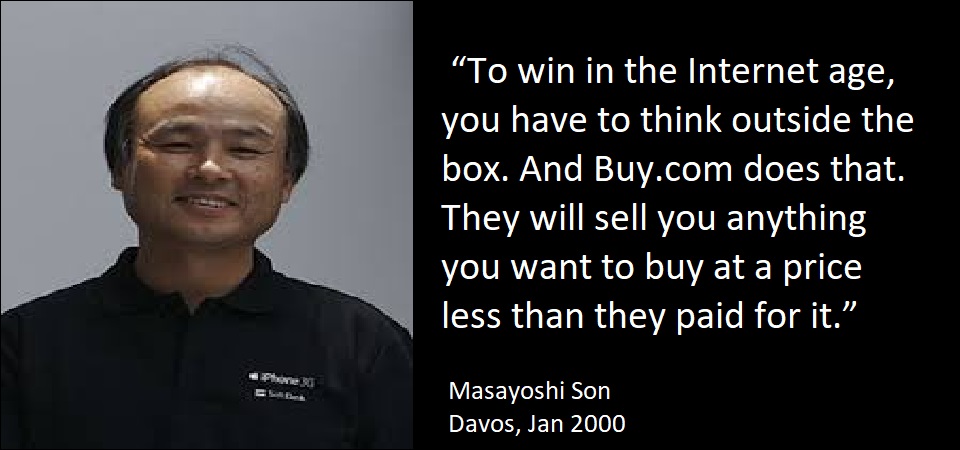

Buy.com later crashed. Of course Mr Son is a legend and a billionaire even though that one did not work

---

Connect via my

LinkedIn |

Facebook |

X |

YouTube