I wrote about the Nigerian Banking Market Cap Paradox a few days ago. This paradox is thus: banks continue to break revenue and profit records but are yet to see decent bumps in their market caps.

Our largest bank by market cap, GTBank, had fallen from N1.3 trillion to now N741 billion even in a time it has been declaring massive profits and growing revenues. Simply, there is no reason why that should happen. But it is happening due to market perceptions. Look at those numbers; it is only in Nigeria that a bank will deliver such, and yet nothing great happens on its stock (see the figure). Tell me, if massive profits do not deliver the glory of market cap bumps, what will?

Godbold Promise on LinkedIn has done the real professional work needed on the numbers to understand what is happening here. Read his full thesis below.

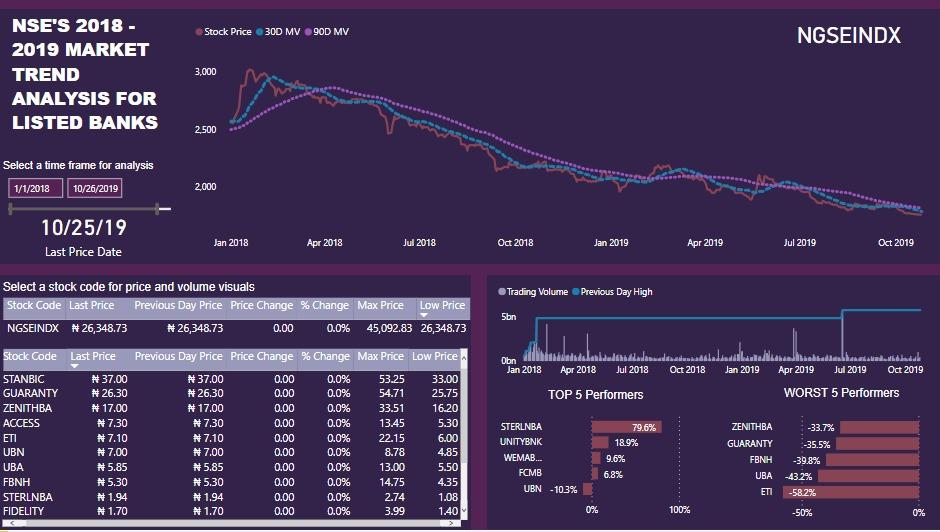

After reading a post by Ndubuisi Ekekwe today, I decided to run a 2 year analysis using #powerbi on the Nigerian Stock Exchange index and also on all the banks listed in the Stock Exchange to really understand the stock price performance over a 2 year period.

The result of the Analysis are as follows;

*The NSE index sheds 16.2% in 2019 against 14.0% decline in 2018. The index started flattening from Feb 2018 after then the index hasn’t recovered, it has been flattening till date.For the Tier 1 banks, almost all the Tier 1 banks lost price momentum YoY save Access Bank.

There performance is as follows:

* Gtb dips by 23.7% in 2019 against 9.2% decline in 2018.

*Access bank increased by 7.4% in 2019 against 23.9% decline in 2018.

*Zenith Bank dips by 26.2% in 2019 against 7.6% decline in 2018.

*UBA dips by 24.0% in 2019 against 22.3% decline in 2018.

* FBNH dips by 33.3% in 2019 against 6.8% increment in 2018.It happens that all Tier 1 banks relatively performed poorly YoY and 4 of them were worst performers save Access Bank from Jan 2018 to 25th Oct 2019.

This analysis still leaves us with same question by Ndubuisi Ekekwe which is; despite large profit, why are these banks losing price momentum.

The link to the dashboard is in the comment…

On what is happening in the sector, here are some comments from the LinkedIn thread.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

-

One thing you should know is that investors are not only concerned about the huge positive numbers but also look inwards as to what’s contributing to those numbers. In a case where the drivers of the profit are not sustainable, then huge sell-offs will ensue and share price starts declining. Maybe you should check the financials and see if banks huge profits is as a result of an increase in SPREAD in their core business of financial intermediation or as a result of other factors investors feel that are not quite sustainable in the future. That maybe the only reason to justify why there’s a share price decline despite posting huge PBT on their comprehensive income statement.

-

Very apt! There are so many factors beyond financial performance that should be considered. E.g. Corporate governance framework, including but not limited to, controls around the eported numbers & Risk Management procedures, country risk (political & market)- as investors aren’t only Nigerians etc.

-

See, why an investor would buy MTN Nig shares and not Airtell or GTB is simply the same reason why an American investor would buy a Fitbit share now that Google has acquired the company and not before the acquisition. Last generation of investors invested based on the present state of the company… that was the generation where banks and other heavy assets companies did good, but this current investors are concerned about potentials, tomorrow’s state.

-

I had postulated the arrival of MTN. Yet, it is not clear.

---

Connect via my

LinkedIn |

Facebook |

X |

YouTube