Anthemis Group, one of the leading actors in the world of innovative financial services, has laid off 28% of its workforce, which is 16 employees, as it completes restructuring at the company.

The company disclosed that the downsizing of its workforce was necessitated in a bid to better reflect current market conditions and to set up the business for future growth against its strategic priorities.

Anthemis however failed to disclose which roles were impacted, but an insider familiar with the incident disclosed that a former managing director of the firm was among the group that was laid off.

Since the layoffs, the company has made two new hires, an Investment Principal and the Head of Intellectual Capital, and currently has a team of 43 people across Europe and North America.

The VC firm which currently has $1.5 billion in assets under management in late 2021 raised $700 million for embedded fintech startups, in what a spokesperson described as a collection of capital it closed across strategies from its venture studio through to its Venture growth fund.

Founded in 2010, Anthemis is a global platform that cultivates change in the financial system by investing in growing and sustaining businesses committed to resiliency, transparency, access, and equity. In 2016, the firm made the first close of their inaugural fund at $60m, with the aim of reaching $100m to exclusively invest into FinTech companies.

The venture investment platform is founded on three guiding principles which are authentic collaboration, virtuous cycle outcomes, and diversity and inclusivity. The firm has had a concerted interest in FinTech throughout the years for its investments, accruing over 20 investments into the space since inception.

Regional focus has been restricted to Europe and North America thus far for Anthemis’ FinTech investments. The firm has also been expansive regarding FinTech subsector investments, with their investments spanning most of the subsectors within the industry

Anthemis has made more than 150 investments in fintech firms which include Betterment, eToro, Currency Cloud, The Climate Corporation, Carta, Happy Money, and many more. Its Early stage investments include Pipe, a recurring revenue trading platform; Weavr, an embedded banking provider for digital innovators and fintech; and Atomic, an investing API for fintech and banks. Venture investments include Branch, which bundles home and auto insurance; Eigen, an intelligent document processing provider; and LocoNav, a telematics-based fleet management platform.

Anthemis heavily promotes its progressive values of diversity and inclusivity. Its vision statement includes building “one of the world’s leading diversified financial services companies, with a commitment to diversity, equity, and inclusion as a blueprint for the economy.”

By creating fertile ground for a diverse group of startups, investors, entrepreneurs, institutions, academics, and visionaries to cover, Anthemis believes it can solve the financial system’s most pressing challenges faster, better, and for the benefit of all.

One of the biggest challenges with working within the payments ecosystem in Nigeria is you tend to see things differently. For instance; while all most people see is a POS agent at a junction, the first thing that usually comes to mind when I see a POS agent is “Who is acquiring those transactions?”. When I see a mobile payments application (from an unlicensed fintech), the first thought is “Who is their wallet API provider?”, and when I see a pay with bank transfer implementation on a payments gateway, my first idea is “What is informing their choice of this specific service provider?”. This is why when news of certain fintechs being a reliable fallback option when bank networks were failing in the heat of the cash scarcity dilemma came to light (considering most fintechs runs on the same real-time rails (NIP by NIBSS) the banks process transactions with), I figured one or more of three things were happening:

Banks were having issues with their core banking: A core banking is at the heart of every bank’s operations, it is basically the central operational point for all banking transactions and is the module that controls debit and credit updates within a bank. The theory that the sudden increase in transaction volumes (984% QoQ growth in transaction volumes) overwhelmed the core banking of most banks and caused a lot of transactions to fail makes a lot of sense. In all likelihood, there are banks who probably run on outdated core banking software (which is usually not the case with new-age fintechs), and that may be a key reason for failures on their end.

P.S: replacing a bank’s core banking is not very simple, it’s a very delicate process that takes time and requires expertise. I’d liken it to a heart transplant – if you did a heart transplant, there’s a risk of death, but if you had the option of managing a heart condition with medications and drugs, you’d probably want to take that option. This Twitter user also alluded to core banking failures being at the heart of Zenith Bank’s issues.

Zenith Bank was notorious in Industry IT circles for using a Core Banking Application (and other key IT platforms) the were different from what the rest of the players used. This gave them an edge in that folks hardly poached their tech staff because the domain experience… /1 https://t.co/685PEUoO79

Side note: Zenith Bank recently announced a revamp of their software stack.

Certain fintechs have multiple settlement account arrangements:The Nigerian payment system is designed in such a way that banks play a very key role in transaction processing primarily because they act as key sponsors to other non-bank financial institutions who want to process transactions on the Nigerian real-time payments rail.

Certain fintechs (depending on their licensing type) use settlement accounts across banks to process transactions. If a fintech has multiple settlement accounts across multiple banks when their customers wants to process fund transfers to a bank they have a settlement account with, that transaction can be structured as an on-us transaction that runs on the bank’s internal system (no need to pass through an interbank payment rail).

For instance, if Fintech A has a settlement account with a couple of banks of which Access Bank is one of them, and Fintech A’s customer wants to send money to someone with an Access Bank account, Fintech A will pass an instruction to Access Bank to debit their (Fintech A’s) settlement account within Access Bank and subsequently credit the beneficiary (who is also an Access Bank customer).

Transactions of this sort are cheaper, faster, and in most cases rarely fail (they are internal ledger updates within the bank). Executing this however has huge reconciliation implications and every reconciliation person reading this is probably hoping their boss doesn’t see this, but I digress.

Some fintechs run on other third-party rails: NIP is not the only real-time payment processing rail in Nigeria. While other fintechs like Remita (via RITS), Interswitch, and eTranzact have other solutions in this market, NIP is the most dominant player, primarily because of its high efficiency and cordial relationship with the banks. NIP is also the default payment processing engine for most banks in Nigeria.

There are however alternative payment rails that other fintechs may have been riding on, and If these fintechs didn’t have multiple settlement arrangements across multiple banks, and banks weren’t having issues with their core banking, this would probably be the major reason they were able to process transactions while the banks were failing at their ends.

SINGLE POINTS OF FAILURE

At the SystemSpecs Maiden Tech Innovation Series Titled Cashless Policy: Sustaining Digital Payments Beyond the Currency Redesign, the MD of Remita, said and I quote –

“In summary, we just had a national UAT for cashless, so we need to ask who was the product manager, where was the national operating center, where was the national crisis center” – ‘DeRemi Atanda

The occurrences of the last couple of weeks (failing digital transactions etc.) were basically a User Acceptance Test to show if we’re ready for a fully cashless economy. We aren’t. And amongst a list of reasons, one of them is our overarching reliance on a single interbank payment rail.

NIBSS (Nigerian Interbank Settlement System) is one of the most important players in our fledgling payments ecosystem. NIBSS provides the much talked about NIP (NIBSS Instant Payment service) product that powers real-time payments across multiple banking providers nationwide. On a global scale, NIP is ranked as the 6th real-time payment rail by transaction volume, just behind the United Kingdom and steps ahead of the United States. In 2022 alone, NIP processed what amounted to N387trn (US$840.5bn) in transaction value and 5.2 billion in transaction count.

According to Bloomberg, about 90% of transactions in Nigeria’s informal economy are conducted using cash, in other words, Nigeria has only digitized 10% of its transactions – To be clear, NIP is a stable solution that works 99.9% of the time, but in a world where 50% of transactions occur digitally (5x more pressure on NIP), do we wait for NIP to bulk under pressure (as it may have done these past couple of weeks) or do we need to provide redundancies to ensure our payment systems stay up and running regardless of who has a downtime? I think the latter is the better option.

Our heavy reliance on NIBSS for payment processing puts a lot of fintech players under pressure when things tend to go wrong. Some months back, PiggyVest, a leading digital savings and investment platform in Nigeria couldn’t process disbursements to its customers. At the root of the problem was an issue at NIBSS end, unfortunately, customers don’t know what NIBSS is, what they know is I saved money with you, I need to withdraw and now you’re speaking gibberish because that’s what NIBSS means to a person who urgently needs his N50,000 (US$108) and you’re telling him stories.

Beyond the core payment processing engine failing, a downtime on other ancillary services on the NIBSS platform can also influence payment processing. A good example is the Name Inquiry service – payments in Nigeria are so designed that if a beneficiary’s account number and bank name are not verified on the database, those transactions will not go through, this helps avoid transfers to the wrong account – make person no see your wrong transaction call am miracle alert lol. However, this also means in situations where the Name Inquiry API is down, transactions will not go through, even though the payment engine is working just fine.

I’ll restate that NIP is an efficient service and works most of the time, but if Nigeria is going to build a cashless economy that runs on digital payments, digital payments cannot work most of the time, they need to work all the time. We need to build redundancies.

BUILDING REDUNDANCIES

The major reason we need redundancies is to foolproof our payments system. Another side reason may be to democratize opportunity. If I owned a switching company acting as a redundancy to NIP, just looking at the number of transactions processed on the NIBSS platform alone and trying to model what my revenue would look like, I would probably be driving a 2022 Mercedes G63 or a Tesla Model X by now, in fact, I’d be writing this article from the study of my private use US$2.5million Sujimoto Apartment, but I digress.

There are two ways the CBN can go around building redundancies within our payment system:

Open the Doors: There are presently 16 licensed switching and processing companies in Nigeria – a switching license allows you to extend your fintech business to offer products in the PSSP, Terminal Issuance, Switching, and Super Agency Business. Fintechs like Remita, Interswitch, Flutterwave, Paystack, and TeamApt are holders of this license. Most holders of this license use it to extend their offerings, but rarely ever to build a switch.

The challenge with building a core switch is that it requires more than just coding, it requires some kind of touchpoint with a bank’s core banking, and as we shared earlier, a core banking is the heart of a bank’s operations. The same way you will not just open your heart to anyone and fall in love with them (unless they drive a 2022 Mercedes G63, then you should probably be falling in love with them) is the same way banks do not just open their core banking to anyone to interface with.

A system that allows CBN to choose certain providers (maybe two players), give them stringent security and compliance criteria to meet, and MANDATE the banks to open up their systems for them to connect with will create more potential players for redundancy plays.

Mandate the banks: At a high level, the CBN has two key responsibilities – tell players what to do (in the best interest of the payment system) and mandate them to do it. I personally feel that things move forward quickly when the CBN mandates key players to do certain things as against keeping it open (like they did with crypto). This is also why I’m not bullish on CBNs recently released operational guidelines on Open Banking. While the document creates a clear standard for open banking implementation in Nigeria, it doesn’t mandate the banks (key API Providers) to do anything. In the UK where Open Banking is dominant, the top 9 retail and SME banks aren’t advised to adopt Open Banking, they’re mandated to, Open Banking in the UK is not a revenue conversation, it’s a compliance conversation.

In the same way, deposit money banks should be mandated to employ redundancies within their payment processes, and be allowed to choose from amongst the fintech players who already have these rails, and those who will hopefully be able to build in the future.

This doesn’t mean NIP will not continue to process the majority of transactions, it will, but in the few cases it fails, the banks will have a second and maybe third option to push transactions to in the advent of a failed transaction.

The banks can then build routing mechanisms on these redundancy options. So, for instance, if a transaction times out in 15 seconds, when a bank passes an interbank payment transaction through NIP, if by the 10th second NIP is still unable to touch the beneficiary banks environment, the bank can immediately route that transaction to its secondary switch to try and reach the beneficiary bank, if that fails and a third option is utilized, we can safely assume the beneficiary bank is having an issue, and that can be relayed to the sender along with the reversed debit transaction.

The implication of this is that fewer transactions will fail, and those that do fail will be because there was really no alternative way to get it processed.

CONCLUSION

The events of recent weeks have proven to us that beyond educating the masses and providing payment touchpoints, building redundancy into our payments system to withstand increased transaction volumes that emanate as a result of the cash-to-digital migration is a key next step to building resiliency into our payment ecosystem, and maybe, just maybe we may finally have a business case for building alternative payment rails in Nigeria.

In 2000, Abia State unemployment rate was 4.2%. By 2019, it had risen to 32.5%. The question is: how do we get the unemployment rate to a single digit? In other words, how do we get Abians back to work?

This is a very important issue because I met Aba, the heart of the state, when it was still working. As an intern in NNPC Nigerian Gas Company (Moscow Road, PHC), my duty station was Owaza Gas Flow station. Weekly, from Owaza, I would go and read gas meters in Aba Glass Industry, etc, which received gas from the flow station. Those pipelines were there and from Owaza, NNPC supplied gas to Aba industries.

Today, we are talking of providing gas pipelines to power companies in Aba. But decades ago, there were working pipelines! What happened to those infrastructures? Big question indeed.

Good People, a new Abia is coming and we need your support to build new industries and get young people back to work! Mr. Governor-elect, Dr Alex Otti, made that promise and we’re confident he will fulfill it to young people and all Abians. As part of helping his playbook, share your answer on “how do we get the unemployment rate to a single digit in Abia State?”

Prof Ndubuisi Ekekwe

Co-Chair, Abia State Economic Transformation Transition Council

Comment

My proposals

All this can be achieved in less than 8 years.

Some less than 4 years

It is possible.

We just need to stimulate the catalyst for growth which is what I focused on. pic.twitter.com/Zgphh6s8gp

My Response:I have read the 50 year plan two times. Great work. But notice that it omitted clearly how to fund these elements. Abia does not have the luxury of listing every nice cookie without how to pay for it. Government does not need to run a bank. But the government should make it easier for private banks to do their jobs. With billions of naira in debt, a spending-based strategy will not pick up. We’re exploring how we create and improve ease of doing business so that companies/investors can see the opportunities and come.

My Response:in Igbo culture, you do not ask your host for kola because you have none. In consultative leadership, seeking inputs to refine ideas cannot be a sign of weakness. The problems are known. Some solutions are at work. But engaging communities to architect their futures has always worked because when people are part of designing the system, the execution is always better. We do not want to stay in one room, write and push on the citizens. So, we’re speaking with community leaders and we’re confident that a transparent honest conversation will help to shape priorities.

Comment 3: Prof Ndubuisi Ekekwe, I strongly believe you and your esteemed team have all it takes to reduce unemployment rates in Abia State, Nigeria, to single digits. The state’s unemployment rate rose from 4.2% in 2000 to 32.5% in 2019, making it important to create new industries for job opportunities.

To tackle unemployment in Abia State, solutions include:

Promoting and supporting entrepreneurship (by providing support programs, training, and funding to enable young people to start their businesses), attracting investments (local and foreign investors), developing infrastructure (to enhance transportation, communication, and energy supply), encouraging public-private partnerships (PPP) (The government can work in partnership with the private sector to provide support and investment in critical sectors of the economy), and improving education and skills development (The government can invest in education and skills development programs that will equip young people with relevant skills for the job market.)

Comment 4: There has to be a way to move Micro Enterprises into Small and Medium enterprises by helping them grow, Having access to what’s needed

I’ll opine there should be a functional business school in Aba where thorough knowledge of how to build aright, can be shared

Open up The Technology Incubation Centres and industrial parks to serve as sandbox for various industries… food, leather, fashion etc… where ideas can be birthed and place some government owned Enteprise support fund [Part Loan, Part Grant or Part Equity]. The industrial hub should have its own power or dedicated power lines

Aba Needs Indigenous Tech startups that can digitize ecosystems and Capture values and employ people in large volumes. But more importantly, facilitate transactions – I think the tech ecosystem needs to be built for startups incubation, harnessing of its Higher Education students for localized and remote works

Can we Gamify SME support!? and reward get getting

Financial services company Klarna has redesigned its app to introduce TikTok-like features, powered by Artificial Intelligence (AI) to enhance users’ experience.

The fintech company disclosed that its new design would help users find items they want by using more advanced AI recommendation algorithms, while merchants will be able to target customers more effectively.

Based on the shopping behaviors of Klarna shoppers and their favorite brands, the AI tool will create a personal profile for them. Thus, these shoppers will receive recommendations from Klarna’s 500,000 retailers including some of the top players like H&M, Nike, etc.

Speaking on the rollout of Klarna TikTok-Like AI-Powered Features, the company’s Chief marketing officer David Sandstrom stated that the inspiration was gotten from Chinese firms, as he noted that top shopping platforms in China have been leveraging the use of AI-driven shopping which has been effective.

In his words,

“In China, a couple of years ago, 90% of transactions started with a search. Nowadays, less than 50% of purchases start with a search because recommendations are so tailored to them. Our ambition is to basically offer people products and brands before they knew they wanted them”.

Sandstrom further stated that it would be naïve to compare Klarna’s features to TikTok’s recommendations. He said it would be a blatant lie that the company is close to the short-form video-sharing platform, however, Klarna has the prerequisites to do that.

Previously, the fintech company also launched the ability to integrate OpenAI’s Chatbot ChatGPT into its service along with a plugin that allows users to ask the chat or platform for shopping inspiration. Instead of relying on AI alone, Klarma looks to personalize its services further and recently launched the “Ask Klarna” feature, which allows shoppers to chat with or seek video advice from specialists.

Among the other features Klarna is rolling out is a resale option that lets people sell used clothing, electronics, and other items through a partner platform. Klarna joins a host of other tech firms that are incorporating AI-powered technologies into their products to enhance users’ experience.

Founded in 2005 in Stockholm, Sweden, to make it easier for people to shop online. With technology rapidly evolving, Klarna has continued to upgrade its services with its mission to make paying as simple, safe, and above all, smooth as possible.

Klarna is the leading global payments and shopping service, providing smarter and more flexible shopping and purchase experiences to 150 million active consumers across more than 500,000 merchants in 45 countries. The company offers direct payments, pay-after-delivery options, and installment plans in a smooth one-click purchase experience that lets consumers pay when and how they prefer to.

The Crypto Industry last weekend experienced a sharp decline in the price of Bitcoin the world leading decentralized digital asset and other major coins like Ethereum, Solana, Binance coin BNB slightly decline in price. Bitcoin started last week Monday with record high above $30,000 per BTC, Ether around the $1.8k zone and BTC currently trading at $27,450.

Some analysts anticipated such an outcome and even predicted a significant pullback. But is a strong pullback below $20,000 probable if those predictions are correct?

Here’s what we know so far based on recent data. The latest Glassnode alert revealed that the amount of Bitcoin supply that was active in the last two to three years just soared to a 2-year high.

This meant many individuals holding BTC had started moving their coins. Such an outcome suggests that many of them might be selling their coins in anticipation of higher sell pressure.

The bearish expectations also reflected the current state of the market. BTC just concluded a bearish week characterized by whale outflows.

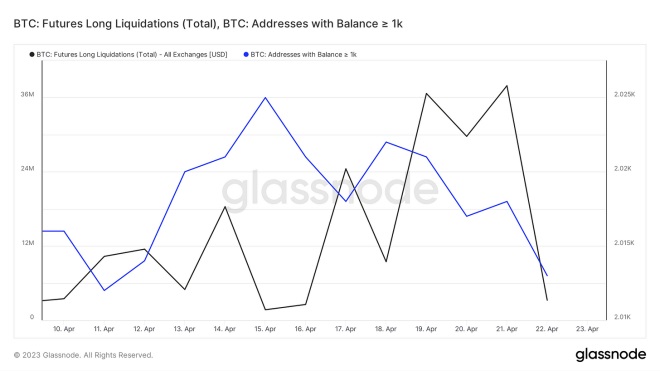

Whales were trimming their balances since mid-April according to the addresses with balances equal to and greater than 1000 BTC.

Source: Glassnode

Meanwhile, futures long liquidations increased since mid-April but dropped off from 21 April. Why is this important? Well, the initial surge in liquidations may have fueled more sell pressure as leverage traders were forced to sell.

However, the drop-off in long liquidations indicated that sell pressure might slow down.

BTC exchange inflows have dominated compared to outflows since mid-month. Exchange outflows also increased, likely due to investors buying the dip. The rate of flow for both has been slowing down in the last two days.

Source: Glassnode

Interestingly, the latest exchange flow data revealed that BTC exchange outflows were slightly higher than inflows. This was a sign that demand was starting to outweigh sell pressure. But does this reflect the price action?

BTC price action

Bitcoin’s $27,557 press time price hovered above its 50-day moving average which may act as a psychological buy zone. But is a strong bounce-back possible at this point? Yes, but so is the possibility of an extended downside.

BTC has been trading within a support and resistance range. Its latest pullback since mid-April came after the price retested the ascending resistance line indicated in the chart below.

Source: TradingView

So, what should investors watch out for? A strong resurgence in demand for the 50-day moving average may signal a strong bounce back. Weak demand may pave the way for extended sell pressure.

The second outcome may encourage more selling which will eventually push toward the ascending support range. Such an outcome would lead to the next significant support retest near the $22,900 price range.