Being out of employment over a time and job hunting is a reality most professionals will face at a certain point in their lives. Different people react to this almost inevitable season of their lives in varying ways. Some go into depression. Others immerse themselves in all forms of entertainment or even excessive drinking to escape reality. A few, however, have a natural tendency to be calm and calculated. They turn their period of lack of employment into a soul searching and career improving moment.

During this period, what you do or fail to do may end up determining how long you stay out of job and what happens afterwards. It also impacts on the financial situation for those who don’t have the privilege of having excess savings to sustain them through these unpleasant moments (yes, it is usually advised you set aside up to six months of your average financial upkeep to live on in the event of loss of job).

How do you, then, maximize that period between the time you stop working and when you regain employment?

Put your house in order. I do not literally mean house, I mean your inner or spiritual amour house. That part of you that sustains and determine your external outlooks. Know that being out of employment is not the end of the word and is just a phase that shall come to pass. Yes, please, mourn if you will but just for a short while. Then, it is time to find strength from within. It is time to find believe and steer yourself again. Take an assessment of what the events of your past job and internalize learning. If you are honestly reflective, there is always something to learn. Thing not to do again; cycle not to repeat; or better ways of handling similar future situations.

It’s time to brush up or acquire skills. Identify new skills and latent personal attributes that can improve your employability and productivity. Go online, research and sign up on free platforms where you can learn digital marketing, excel, graphics, coding, presentation, communication, writing, baking, cooking, or whatever skills that’s important in your current or aspired career path. Take a personal strength finder test on a paid platform if you can afford it. A similar free test is on www.high5test.com. That new skill may just be the catch for your next job – created by you or offered to you. Going through this process may just open your eyes to things about you that others may be willing to pay for via consultation or part-time engagements. A new business may also be born.

Make your job search a full time job as soon as you resign or are relieved of your engagement, except if you are taking a recovery break. If your aim is to get back in quickly. Re-activate your subscriptions on www.indeed.com ; www.jobberman.com ; www.myjobmag.com ; www.naijahotjobs.com ; www.jobgurus.ng.com and of other online job platforms. Get active on www.linkedin.com make your profile visible through optimization, post contents that project you positively, engage with others, ask for recommendations and referrals, and apply for jobs daily. Also, optimize your CV and Cover letter to be ATS compliant and relevant to your field of interest. Again, apply daily for openings you are qualified for. Note that you will feel frustrated if you are applying for jobs you’re not qualified for or your CV is not projecting you strongly. Sign up and get linked up with recruitment service providers like eRecruit, Ascentech, Michael Stevens, Lorache or as per relevant in your part of the country.

Get away from time wasters. Some emotional distractions for a lot of unemployed persons are excessive sleep, entertainment, hanging out with friends, sexual overindulgence and alcoholism aside other mental and emotional opium. Those have never helped anybody interested in bouncing back quickly. Complacency is not same as contentment. Contented people hold their activities in check to ensure they are channeling their lives’ outcome in the desired direction. The only mental and emotional distractions I recommend are healthy books. Get closer to your God, if you have one.

Gather references from professional network. I have found that my best references come from former bosses. By asking former bosses for written references, I found they highlighted other skills and attributes I thought I wasn’t so good at. Employers find them more credible because they have managed you and can give near accurate analysis of your strengths and weaknesses. Aside Bosses, there must be other senior colleagues in your last and previous place of work that you that you still maintain good relationship with. Network with other professionals and engage them respectfully in your job search. Don’t bore them with calls as if they have jobs stored somewhere. Written relevant professional endorsements are superb attachment as cover letter.

Earn petty income along the way. You may need it for upkeep during the course of your dry season or as transport fare for the next interview invite. Part time ‘runs’ can keep you running until you are gainfully employed again. Commission selling, day rate jobs, content writing, etc. In Nigeria, if you have been out of work for up to three months, you can access 25% of your Retirement Savings with your pension administrators. Ensure you approach them with evidence of your last disengagement, means of identification and passport photographs. It is unfortunate that there is no such thing as filling for unemployment in Nigeria. Our government has no unemployment support system so it is up to you to find local businesses that may be interested in your services on day rates.

Whatever you do, strive to keep a positive outlook going forward. What goes up must come down is a sure saying. It’s only a season and seasons come and go. See you at the top soon!

Often times I write from my own perspective , the construction industry. And sometimes it is difficult to say if some of the things I have written still hold in other industries or broader still, in other facets of life.

There are so many reasons why subordinates could be difficult to deal with, a lot of them. This does not necessarily mean that they are not willing to work, even though there are times when this could be the case. On one particular occasion while working in the Niger Delta, I was left with a group of angry poorly motivated workers some of whom were ex-militants. This was the case as the Senior Engineers could not handle them because of the threat of violence and the difficulty in dismissing them. The terrain was daring; being left alone in a bush hundreds of miles away from the base, with a group of “armed strangers” to work alongside with, was something worth preparing for. I took my chance anyway.

First of all, there are reasons why subordinates could be difficult to work with, and they include the following :

When they have a history of violence or rebellion:A worker with a history of violence or rebellion will find it difficult taking instructions from anyone. Sometimes, it doesn’t matter what is done to them, they tend to naturally return to the means of resolution or communication they are accustomed to when in seemingly difficult times.

When they realize how difficult it will be to let them go:People know when they are indispensable. There was an instance where a particular crane operator bragged about how nobody could fire him as he was the only available person who at the moment could operate that brand of crane. The previous operator was an expatriate who left years ago. This gave him the rare privilege of tolerated insubordination. Another similar case is where a worker is related or close to someone of great importance to the organization.

Poor remuneration: Workers who are poorly paid are rebellious in nature and subordination in this instance is also extremely difficult.

Extreme pay inequality between the upper hierarchy and the lower hierarchy: Extreme pay inequality could be a disservice to any organization. The general feeling amongst the lower hierarchy would be that they are the one’s doing the work, where other who barely do anything are getting all the reward. The bigger the gap, the more unrest there is likely going to be . A typical case of “monkey dey work, baboon dey chop” (monkey works, Baboon eats) .

Lack of career growth:When loyal workers have put in many years of service in a firm with little or nothing to show for it in terms of career growth, it leads to dissatisfaction. And this dissatisfaction is spread or transmitted to even new employees, who having heard stories of how loyal employees were treated in the past, tighten their seat belts for insubordination .

Bad Management:Bad managers can make even good workers lose motivation. Acts like lack of professionalism, abuse of power, lack of empathy, not following due process etc can strangle out the order in an organization.

Pride:Pride can make a worker exaggerate his influence and can even make him reluctant to respecting leadership .Instead of seeing work to be done, he sees a personality to attack.

I tried to highlight possible causes of rebellion in the workplace by listing the items above based on my personal observations. So, now going back to the scenario at the beginning of this article, I will highlight also the techniques I employed to manage the situation. The point here is that it worked in the end. I was able to keep them motivated and working even though they may have done so reluctantly. I was safe, they worked, we delivered. These are practical steps I applied that really worked in handling workers in extremely volatile situations.

Erase or suppress the feeling of fear: Yourbody language matters a lot. Fear could be seen as a sign of weakness, and people could read and smell fear from the way you talk, walk or even react to simple situations . Many of them are experienced in capitalizing on it to their advantage. Try anything legal that gives you the maximum confidence you need to meet them every morning .

Play along as a victim too: Playing along helps to. Be sympathetic to their plight and try to understand what life is from their end, or at least pretend to understand. Make them understand or think that you don’t necessarily like what you have to do, but just that you have no choice. That all of you have a common “enemy”.

Never isolate yourself even in the midst of tension: If eventually there is tension, never isolate yourself. It is seen as evidence of fear and could be taken advantage of. Rather integrate and come as close as possible to the scene. It also gives the impression that you aren’t always just thinking about yourself.

Try some sense of humour: Good old jokes can help lighten situations. It works a lot of times. Just don’t do it in every given moment. Timing is key.

I have written this down based on personal experience gathered from working in the field, it is left for the reader to use his discretion to know if this works for him. All the best.

I had set out for Ahia-Ohuru open Market in Aba that fateful Saturday morning with my monthly grocery list. After driving around for a while in search of parking space, I finally managed to squeeze in somewhere at the back of Enyimba Sports Stadium and started the short walk towards the market.

Up ahead, my attention was quickly drawn to gathering of people ahead of me. Whatever was going on there seems to have its audience enchanted.

As I drew closer, the crowd erupted into frightened shouts.

Chineke!

Ogbu o le ya!

Jesus!

Some ran away temporarily only to return. Curiosity killed my cat and I joined the circle of onlookers.

At the centre, what looked like a skillfully cut-out human tommy sat face down on a semi-open discarded Peak Milk carton. A half-clad Medicine Man, eye ringed in white chalk, was muttering incantations in Igbo with his legs spread over the tummy.

A teenage boy who looked like an apprentice pick-pocket nudged me at the bum. I instinctively transferred my wallet from my back pocket to my left hand, where it is safer.

Some fellow onlookers, converted to customers, were buying piece of herbs and roots from the Medicine Man’s Assistant at to the right from where I stood.

Apparently, the magic of turning his second assistant into a seating tommy has convinced them of the efficacy of the Medicine Man’s wares. As the white eyed man was slowly pulling out a live python from underneath the seating tommy amidst momentary shrieks, my attention is drawn to smaller crowd that had just gathered beside the bigger one.

Being a lazy Saturday, I overcame my temptation by joining the smaller crowd.

Forget about the Bollywood movie, I had planned to watch when back from the market, this was a live Nollywood scene. Why not? There in front of me was an elderly man of about sixty-something just won wades of clean N5,000 notes simply by putting down N500 and then identifying the Joker among three cards placed face down after a clever shuffling of hands by the Artist.

I volunteered a mere N200 and won N1,000. Venturing further, another N500 earned another N5,000. Business was sweet. This artist guy must be a fool, I thought. It was so easy sporting the right card if you have attentive eye.

The guy then placed on his make-shift table a hundred thousand naira – mint bundle of one thousand notes with its bank paper wrap still intact. He invited us to play with N10,000.

Greed called my name, I resisted.

My village people muttered words of encouragement. But I was adamant still.

I resisted every temptation to go further, stuffed my profit into my wallet and started quietly meandering my way to where I was going. Nobody made any attempt to woo me back.

God bless Mama Nkeiru!

As always, she helped source all the things on my list while I seat reading a newspaper. She was pretty fast today. My bill was N35,550.

I dug into my wallet only to pull out wades of neatly folded plain papers. Gang…gang!

No, the devil himself must have carefully arranged these god forsaken papers where the money I left home with this morning and my card profits were supposed to be resting. I realized immediately that an exchange must have taken place between I and the card guy whom I thought was a fool. I was the fool really and have always being! I sat down to recover my nerves.

I offered Mama Nkeiru the option of returning the items or driving with me home for her money. She wisely went for the later. As we walked to where I packed my car, the crowd seemed to have disappeared into thin air. How can I tell Mama Nkeiru this was where I subjected myself to African Abracadabra – a Saturday morning show of ‘the more you look the less you see?’

How can I?

That was in my other life many years ago.

I learnt to be wary of trading money for money after my reincarnation. Or so I thought until…until…wait for this!

After my reincarnation, I decided that the best place to make profit was earning unambitious interest on my meager savings in then Gulf Bank as a student aspiring for admission. The savings was started two years earlier to raise money for my school tuition. But in 2004, Gulf Bank went underground just at the point I got admission.

I prayed and fasted to no avail. I was forced to source my tuition from other avenues until three years later when Uncle Charles Soludo skillfully connived with UBA to return my money that was trapped in Gulf Bank. Indeed, God answers prayer! I started believing again in regulatory agencies such as CBN and Dora Akuyili’s reformed NAFDAC.

Buoyed by the successful return of my money by CBN through UBA, I picked up a savings (I don’t view it as an investment as it was basically a way of keeping money I didn’t want to touch) product that same 2008 with AIMS Assets Management Ltd in Kano. After four years of monthly savings with AIMS Assets, I turned up one day at their Kano office to stare back at some giant padlocks staring back at me.

Several phone calls to my account Manager and AIMS Assets head office ended in a frustrated attempt to seek redress from Security and Exchange Commission (SEC) in 2012. As I write, SEC has not been able to do anything about that.

Being an incurable belligerent he-goat, I still got myself into another financial dilemma by taking up an assurance policy with Industrial & General Insurance (IGi) in 2013. After several unprintable poor customer experiences, I decided I had had enough and surrendered for claim in October 2018. After three months of silence from IGi, my lawyer sent in a letter. Within the same period, IGi sent me a penalized value voucher for early surrender. It is now over 9 months since I surrendered for claim and IGi is yet to pay my money.

Their Kano office is also in locks. My account officer has joined a competitor. The current Branch Manager has no idea of what customer service is. Head office contact lines will not pick calls. Except for two occasions, mails are not being responded to.

For an industry that is viewed with an unbelievable skepticism by Nigerian, one will at least expect the insurance industry in Nigeria will raise the bar to build positive customer experience. Alas, the reputation of that sector is such that almost all employees in that industry wear a certain look of dissatisfaction. I had my compulsory undergraduate industrial attachment in this industry. So, I know they even struggle to attract quality professionals.

The job of their salesmen has become such a horrible daily experience due to the difficulty of convincing Nigerian to take up policies. Abroad where industry outlook are far better owing to better regulations and practice, insurance sales persons still grapple with negativism not to talk about a place like Nigeria where the word insurance is dreaded. A search on social media such as Twitter and Facebook will shock you at the number of people recounting their unpleasant ordeals in the hands of insurance companies in Nigeria.

The industry regulatory body, National Insurance Commission (NAICOM), like their counterparts in several other industries remains in an unbelievable docility proving unable to help ordinary citizens that have ventured to put their trust in them. There seem to be this ‘sidon dey look’ posture that even simple complaint mails do not receive any personal response.

Someone recently posted his unpalatable experience with one of the Air lift companies in Nigeria aviation industry with myriads of commentators unanimously agreeing that there is no such thing as regulatory bodies in Nigeria. Organizations such as NAICOM, SEC, among others basically seem contented with collecting salaries. My aim is not to call them out on this piece but it is my wish that more attention be paid to regulatory agencies effectiveness in Nigeria. This will lighten the pains of ordinary Nigerians like yours truly.

If steps are not taken to hold the leaders of these agencies accountable to their duties, faith in the system will keep eroding.

Oh, you may be wondering why I am not talking about legal redress. The legal system is a several years dance in the market square by the end of which the Ngwo tree may have being scourged dry of its last pint of palm wine. That in itself has to be a last resort, in this financial and regulatory circuit show, of the more you look, the less you see.

Nigeria needs better regulatory systems and NAICOM must step forward to help deepen the growth of the insurance sector.

More customer experience narration

The guy is a smooth talker.

I had noted that while watching him diffuse the anger of other customers from where I sat. Though I couldn’t quite make out the conversations, I could tell an angry customer when I see one. I admired Smooth Talker’s skill – at least, until it got to my turn.

As I narrated what brought me to their head office, all the way from Kano, he listened with rapt attention.

‘You mean you surrendered your claim since 10 months ago?’ Smooth Talker asked and went ahead to paraphrase all I said earlier.

I nodded as I handed him a copy of my returned voucher and the letter my Lawyer had written to them about seven months ago. He examined it, went in to verify and came back. I could see he is ‘feeling my pain’ in that professional trained ways as he went on to tell me how that his company is undergoing liquidity challenge. How they have lots of assets but are struggling to get buyers to settle claims. How a court order froze their bank accounts. How they were going to send me an email detailing their payment plan.

I scratched my head at that last one knowing these people don’t even pick calls any more nor do they reply to customer emails. The last time I checked, the globally excusable practice is for the debtor to initial this communication process long before a big-headed creditor like me show up at their corporate head office all the way from over several hundred kilometers.

Notwithstanding, I listened as he went on and on narrating what, from my view, was a pathetic story of a corporate organization that has failed in its responsibility towards its customers. For me, what he was reeling out was a once-upon-a-time tell tale of how some big corporate executives have used customers money to ‘chopulate life’ and now wants to subject mere social expendables like me to their well-practiced corporate bullying.

Once I sensed Smooth Talker’s tank was empty, I dipped into my Great Grand Mother’s Tortoise folklore bag and brought out a few of my personal recollections to refill Smooth Talker’s eardrum.

My wife’s shop rent is four months overdue; the last two terms of my children’s school fees were unpaid and school is resuming in three weeks; all my village people are sick and as their breadwinner, I am been looked on to foot their medical bills; and to cap it all, I borrowed money to make this journey and don’t even have money to return back to Kano. I produced my kwashiokored wallet to validate my story. Finally, I indicated I don’t mind sleeping on the chair where I sat while waiting for them to pay my money for as long as it may take.

From his look, I could tell my moonlight tales was a sucker punch – he sure wasn’t expecting that! He obviously was expecting the same angry reaction like those he has dealt with earlier. I watched as Smooth Talker rose with difficulty. My tale of woes surely was weighing heavily on his shoulders as he walked into their inner office to meet his superiors with a copy of my voucher.

Few minutes later, he returns to say they are cascading it up to see what can be done – even if it means having to pay the money in two or three installments. That news was a left hook on my jaw and I staggered under its force. I was tempted to remind him the law places a limit on the length of time within which an insurance company must settle a customer’s claim. That same law failed to empower customers toclaim compounded interest where the Insurer fails to pay within limit. So, like some prey-hunting teething cub, I gathered my wits and waited for them to commit.

For a complainant who turned up exactly 10am that morning, it was till sometime around 4:30pm that another less skilled Smooth Talker came to inform me they will ‘do something but that has to be tomorrow.’

I came prepared to wait.

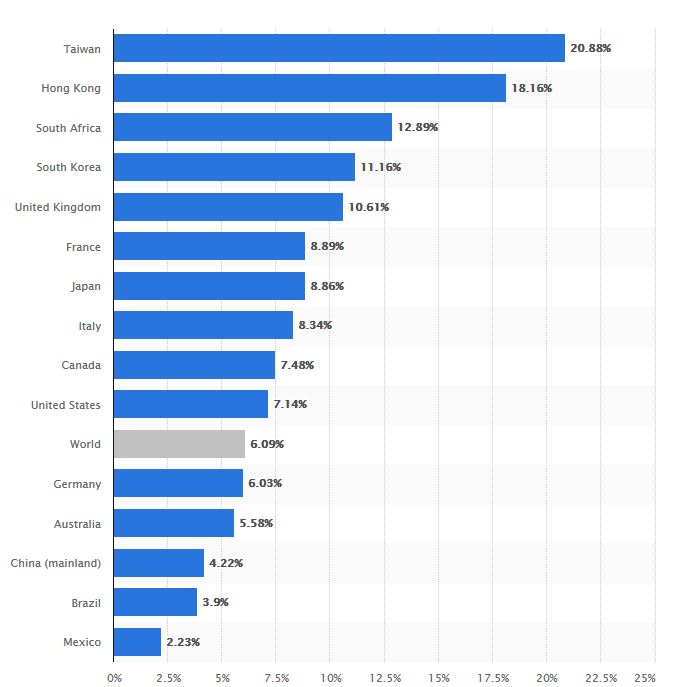

Global insurance penetration for 2018 (source: Swiss Re)

Accommodation sorted out, I was there the next morning 10am dot.

Smooth Talker came again that morning. This time, he said they are able to raise me about one-third of my money and will give me a written commitment on when the rest will be paid. I protested. Smooth Talker literally told me to either take it or leave it and added with raised voice that ‘it is impossible for them to pay me more than that now. The money was gathered from some office stationary imprest cash.

Corporate bullying was fully in action now.

Having seen how all the other customers who raised voices and threats yesterday left there with nothing and also the presence of some Official Intimidation Dogs in black Uniform waiting for instruction to bundle anyone fool-hardy enough as to make a scene into their Cell, I played it cool and agreed. After all, what can I do to these big bullies in very tall several story building?

Two hours later, Smooth Talker came again.

This time he informed me they are sending someone to the bank to process the payment but added, more importantly, that they can’t issue me the already agreed commitment letter (he had obviously forgotten their bank accounts were supposed to be frozen and the money ought to be coming from cash impress). At that, thick black smoke came out of my ears, nose and mouth – I was now ready to end in that Police Cell.

Wise Smoothie sensed that they can’t twist my hand again and went back to produce they letter. When it arrived, it had the presupposed balance split into two further installments in three-to-four-month time.

“That balance has to come in one lump sum. You can’t make a total mess of my plan because of your corporate inefficiency,” I thundered. “What kind of circuit trick are you guys playing on customers here?”

Smoothie ventured further but I immediately let him know that will be calling for trouble there and then. He must have noticed I was past caring and quietly went in to alter the letter as I requested. Even with the letter, I knew it was nothing else but a promise that can be broken with further stories that touch the heart.

Other unprintable dramas followed regarding the about one-third they agreed to pay so much so that I had to spend the next 3 in Lagos days before receiving that annoying and pacifying Bank alert confirming the part payment.

All these trouble, time and monetary expenses just to recover one-third of money I should normally receive without lifting a finger in climes where things are done properly. I thought of a prominent US personality who said something pertaining to ‘shit holes.’

Where things are properly done, Insurance customers would receive their settlement maximum 48hours after returning voucher.

Little wonder, the reputation of Nigerian Insurance industry is in tatters. Little wonder Nigeria Insurance sector still have one of the lowest insurance penetration levels in Africa at 0.3% against South Africa’s 12.8% as at 2018. Little wonder industry gladiators hold several conferences and yet are unable to positively influence the poor awareness and perception of the industry. Little wonder what is supposed to be a great way to save and provides security against risk and uncertainty has turned out to be such terrible customer nightmare.

Where things are properly done, the law and the supervisory body ought to have swung into action after receiving my complaint.

For emphasis, Section 70 of the Insurance Act 2003 requires that claims must be settled within 90 days of the insurance company accepting liability and issuing its discharge voucher. If the company fails to pay within this period, as IGi has done, I as a customer have the right to approach the insurance supervisory body, National Insurance Commission (NAICOM), and ask the Commission to pay me. May be I will have to remind the commission that about this right.

Where things are properly done, and by law, IGi should have notified me in writing on why they are unable to pay in 90 days, and again, if I am not satisfied I can approach the regulatory agency for settlement. But that is only where things are properly done.

As I noted above, NAICOM has failed to even respond formally to my complaint, except for an automated computer response. Where does this kind of industrial irresponsibility leave our insurance industry?

It still beats me why NAICOM are still lingering on the recapitalization that is long overdue.

While they are at that, I am collecting stories of poor customer experiences in this sector, with a focus on IGi, to share with readers on this platform. I will keep shouting through my keyboard until someone do things right in Nigerian Insurance Industry.

Meanwhile, if you want me to write about your plight and raise awareness on the bad practices of our Insurance service providers; you can share your poor customer experiences in this and other industries with me via 08129901475.

“One cup N50, three cups N100,” shouted a woman selling boiled groundnuts while she was busy attending to numerous customers surrounding her and her wheelbarrow filled with boiled groundnuts.

“One salt N80, two N150, three N200,” this time from a man pushing a wheelbarrow loaded with packets of salt.

“Don’t spend too much on clothes for your children. Buy better clothes here. Two, two hundred; two, two hundred. Three for 600; six for 1000.” This one is from a woman and her son selling second-hand clothes.

“Buy three, get one free.” This was blasting from a loudspeaker mounted by a local herb seller.

These are just a few out of the numerous ‘noisy’ advertisements that characterises Nigerian markets. To be honest, I always wonder how these people make their profits especially those that sell things that are of good quality. But the fact that they don’t fold up after some time shows that they have ways of surviving. I am not a business analyst but I believe the following strategies kept them afloat:

One thing I’ve noticed is that these sellers make large sales. And if you consider the amount discounted, you will find out that they will realise it through the quantity of sales made.

If not for anything else, these people attract new customers and their old ones keep coming back. However, customer retention depends on so many other things, one of which is the quality of goods sold or services rendered. But when a new customer is satisfied with what he or she paid for, he/she will keep coming back for more.

I noticed that these traders sometimes use this discount strategy to attract customers who will find out when they come that there are better commodities that are not discounted. Most times, the buyers will find what they need from the undiscounted goods and will buy them. This has happened to me several times.

Some of the goods given out on discount are those that may spoil if left in the shop or warehouse for longer time. So, instead of losing those goods entirely, they’ll sell them off at give-away prices and still benefit from the exercise. The traders may also decide to sell off some commodities so as to make space for new stocks.

One thing these traders have learnt so well is the effect of loud advertisement. I called it loud because they make their advertisements so forceful. In fact, they don’t consider whether you were disturbed by their ‘noise’ or not. Theirs is to make sure that as many people as possible heard about their business, and the discount. In other words, they know the powerful effect of the combination of discount and forceful advertisement.

I know that some of us feel that this type of business strategy employed by these traders may not work in large scale businesses, but who knows. Some businesses have made so much name that they don’t think they need to waste their resources on discounts and adverts. But those are not my interest right now, because they have experts that study the markets for them and recommend what they should do to increase sales. My interest for now is on Naija start-ups.

One of the major challenges of Nigerian emerging businesses is how they can pave their way into the market, which has already been dominated by large and rich conglomerates. I want to inspire these new emerging and would-be-emerging companies with the success story of a school I know so well.

There is this school somewhere in FCT, I’ll call it School A. When School A’s structure was still under construction, someone that lives on the street where School A is located, immediately converted her residence to a school (School B). Maybe she all of a sudden realised that there wasn’t any school around that area and that School A will make much profit. So she decided to open hers first and establish very well before School A’s building is completed. Well, when School A was ready to receive her students, the owner pulled a stunt that nobody thought of – she offered scholarship based on the number of students that come from a family. Look at the way she did it: for families that register up to three children, the 3rd ones will have 50% scholarship. For families that register up to four children and above, the youngest ones among them will have full scholarship until he/she finishes from the school. This information was included in the flyers and circulated. Did this bring students for her? Of course it did.

Dear Naija Start-ups, nobody said it was going to be easy. But we can’t fold our hands because we believe it’s difficult. So, what do you think about giving discounts to attract new customers and retain the old ones? Have you ever thought of the form of discount you will give?

What about advertisement? How do you plan to go about it? Which form do you want to use? You don’t have to spend so much on that. You can spread the words around through the internet. You also can do that through spreading flyers and posters. Ever thought of letting your contacts spread the words for? What about using social media such as YouTube, Instagram, Facebook and the rest? See, make your advertisement loud and don’t apologise to anybody for being ‘noisy’ because the people in the market do not apologise to us for the noise they cause in the market.

Dear Naija Startups, you are not there to compete with the big companies. You are just there to locate your space and keep it. So, I’ll say, “locate your space and keep it by combining discount and loud advertisement.”

On the 27th of May, I got an SMS notification from Zenith Bank that my account has been debited of N52.50, as MasterCard monthly fee, and my balance was at the deficit of N8.42. On the 30th of May, I received another transaction notification: “SMS Notification Charge, Deducted Amount, N12.” My balance deficit climbed to N20.42 by the 23th of June, I was indebted to ZenithBank to the tune of N80. Five days after, my deficit shot up to N141.30, as a result of N8 SMS notification charge for the month of July. All these happened in a savings account.

This means, you can leave N10, 000 in your savings account with a Nigerian Bank, and at the end of the year the Bank will take almost half of the money for charges. It is an extortionist situation applicable to countries like Nigeria, which goes against the ethos of savings account.

Savings account is defined as “a basic type of Bank account that allows you to deposit money, keep it safe, and withdraw funds, all while earning interest.”

Unfortunately, the above definition does not apply in Nigeria, it’s the other way round. Bank customers are being ripped off on a daily basis in the name of “maintenance charges” that has little or nothing to do with transactional charges incurred through banking activities.

I thought about the charges and realized that there has not been significant difference since 2017, when Nigerians went confrontational and demanded that the Central Bank of Nigeria (CBN) reverse some of the rules on banks charges, because it’s becoming more like extortion in the interest of the banks alone, and customers were bearing the brunt. The National Assembly intervened and directed the CBN to quash some of the charges. Well, it’s 2019, and the aforementioned experience is an indication that many of us are working to enrich the banks.

In 2012, Innoson Nigeria Ltd, a customer to Guaranty Trust Bank (GTB) was unlawfully imposed such charges upon, and its current account was debited of N700 million. It took a careful audit for the company to find that out, and it became an eye opener to others who lodge huge sums with the banks. But then it took arbitrary turns before we know it, and every bank account holder in Nigeria is at the receiving end.

In the first quarter of 2019, top 5 Nigerian banks made a total of N15.7 billion from account maintenance charges. They are as follows:

Zenith Bank: N5.238 billion.

First Bank: N3.218 billion.

GTB: N3.045 billion.

Access: N2.212 billion.

UBA: N1.967 billion.

This whooping sum was extorted from the monies that should be yielding interest to Depositors, a reason why Nigerians embarked on a #Endbankingfraud campaign on Social Media for months. Well, the campaign didn’t change anything if not that it created the awareness that Nigerians are getting ripped off by banks, and the enormity is alarming.

ATM cards are issued to customers to ease the number of people on the counter trying to withdraw, so in a way, customers are helping the banks to do their job by using their ATM cards. Therefore, they should be compensated through interests for doing the job they did not sign up for. But that’s not the case, and that’s not the only pain that Nigerians go through in using the ATM. The three withdrawal limit when you are using other banks ATMs, and N20, 000 cash maximum on the withdrawal menu of many ATMs are to ensure that customers who have more cash to withdraw pay charges for doing so.

The Consumer Protection Council seems helpless as the charges are backed by the CBN. And there is less people can do other than complain and seek refuge in Thrift Collectors (Alajos). However, the sundry charges have become a hurdle to banking inclusion advocacy. A student who is counting on the N1000 left in his account would be disappointed seeing that he can’t access the money because his bank has debited N200 from his account for sundry charges. The next time he would keep his money to himself however else he can. The banking recapitalisation is an evidence that Nigerian Banks can function without ripping their customers off. There is a whole lot of lucrative businesses and ideas to invest in. So instead of counting only on depositors money to stay in business, the CBN should ensure policies that will make banks business innovative.