Mary Meeker’s annual State of the Internet report is out. There is nothing new – China and U.S. run the web of business. Europe makes the tough laws because it has few key creative participants to hurt. Africa provides the IP addresses to help the U.S. firms get more valuations from Wall Street. That is it – nothing has changed. Yet, if you have more time, read below:

Image is now a big way to communicate.

Twitter and Amazon are making small in-roads into the Facebook-Google ad duopoly

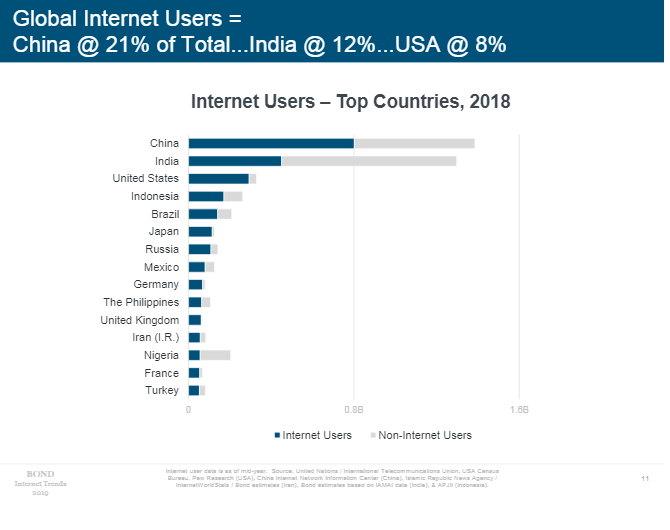

Some 51 percent of the world — 3.8 billion people —are now on the web.

7 of the 10 most valuable companies in the world are tech firms. The non-techs are bolded.

Microsoft

Amazon

Apple

Alphabet

Berkshire Hathaway

Facebook

Alibaba

Tencent

Visa

Johnson & Johnson

E-commerce is now 15 percent of retail sales.

Out of the top 25 most valuable tech firms in U.S., 60% were founded by 1st or 2nd generation immigrants.

Read the report here: https://www.bondcap.com/report/itr19/13

Nigeria is a key regional player in West Africa, with a population of approximately 197 million. The nation accounts for about 47% of West Africa’s population, and has one of the largest populations of youth in the world and GDP of 376 billion USD (2017) – a 4-year record low from 569 billion USD (2014), about a difference of 66%. Operating as a federation that consists of 36 autonomous states, Nigeria is a multi-ethnic and culturally diverse society. With an abundance of resources, it is Africa’s biggest oil exporter, and also has the largest natural gas reserves on the continent.

The country has recently held national elections in 2019, for the sixth consecutive time since its return to democracy in 1999. The incumbent president, Muhammadu Buhari, won the elections and has been sworn in for a second term on May 29, 2019. He has identified fighting corruption, increasing security, tackling unemployment, diversifying the economy, enhancing climate resilience, and boosting the living standards of Nigerians as main policy priorities his government seeks to continue to pursue in his second term up till 2023. Nigeria’s federated structure gives significant autonomy to states.

Between 2006 and 2016, Nigeria’s gross domestic product (GDP) grew at an average rate of 5.7% per year, as volatile oil prices drove growth to a high of 8% in 2006 and to a low of -1.5% in 2016. While Nigeria’s economy has performed much better in recent years than it did during previous boom-bust oil-price cycles, such as in the late 1970s or mid-1980s, oil prices continue to dominate the country’s growth pattern.

Moreover, the volatility of Nigeria’s growth continues to impose substantial welfare costs on Nigerian households. The onset of the oil price shock in mid-2014 confronted the government with the pivotal challenge of building an institutional and policy framework capable of managing the volatility of the oil sector and supporting the sustained growth of the non-oil economy.

Nigeria emerged from recession in 2017, with a growth rate of 0.8%, driven mainly by the oil sector. Growth was higher in 2018 (at 1.9%) and more broad-based; however, it still fell below the population growth rate, government projections and pre-recession levels. The oil and gas sector reverted to contraction from the second quarter of the year and the non-oil economy was thus the main driver of growth in 2018. While agriculture slowed down significantly due to conflict and weather events, non-oil, non-agricultural growth, which remained negative up to the third quarter of 2017 strengthened through 2018 – but remained weak – with services (primarily information and communications technology) resuming as the key driver.

As the oil sector is not labor-intensive, and the non-oil economy was still relatively weak, nearly a quarter of the workforce was unemployed in 2018; and another 20 percent under-employed. With 3.9 million net entrants into the labor force (now 90.5 million people) during 2018 (up to September), but virtually no growth in the stock of jobs, unemployment rose by 2.7 percentage points since end-2017, and more than doubled compared to the pre-recession levels (9.9% in Q3 of 2015).

Economic growth is expected to hover just above 2% in 2019 and over the medium term. The oil sector is likely to stagnate in the face of regulatory uncertainty, limiting investments in the sector. Agriculture may remain affected by conflicts and climate and weather events; and the non-oil-non-agriculture will likely continue to struggle in the face of sluggish demand and constrained private sector credit growth.

Development Challenges & Growth

While Nigeria has made some progress in socio-economic terms in recent years, its human capital development remains weak due to under-investment and the country ranked 152 of 157 countries in the World Bank’s 2018 Human Capital Index. Furthermore, the country continues to face massive developmental challenges, which include the need to reduce the dependency on oil and diversify the economy, address insufficient infrastructure, and build strong and effective institutions, as well as governance issues and public financial management systems.

Inequality in terms of income and opportunities has been growing rapidly and has adversely affected poverty reduction. The North-South divide has widened in recent years due to the Boko Haram insurgency and a lack of economic development in the northern part of the country. Large pockets of Nigeria’s population still live in poverty, without adequate access to basic services, and could benefit from more inclusive development policies. The lack of job opportunities is at the core of the high poverty levels, of regional inequality, and of social and political unrest in the country.

Nigeria’s heavy reliance on Oil & Gas earnings year on year has proved to be curse rather than a gain, this has left all other sector like Agriculture, Mining, Automobile, Technology, Manufacturing, Steel & Power, Local Healthcare Infrastructure Development, Textile, Transportation and Construction industry.

Now that H.E President Muhammadu Buhari and National Assembly are inaugurated, focus must shift to the legacy Mr. Buhari wishes to leave behind. Nigeria’s problems appear to be mounting by the day and it would be a herculean task for anyone to address them all. However, in the minimum, they needs to tackle the following key issues:

Weak economic growth in agriculture & oil

With a 25% contribution to GDP, Agriculture is Nigeria’s largest sector and employer of labour but the sector grew by only 2.12% in 2018 (down 30% from 2017), this despite the government’s numerous intervention programs in rice and other areas. The truth is that without tackling the herdsmen – farmers clashes in the Middle-Belt, which happens to house the country’s most productive farmlands, little growth will be achieved in the agriculture space. The government must bring that issue to a satisfactory close in order to get agriculture on track.

At the other end of the agricultural spectrum is the oil sector, which only directly contributes 9% to GDP but over 80% of government revenues. Refineries One of the greatest tragedies that has bedeviled the nation’s downstream sector is the non-functional existing four refineries with a combined production capacity of 445,000 barrels per day (bpd).

Up until recently, the term ‘turnaround maintenance’ became an annual incident in the lives of these refineries but never worked to 50 per cent capacity after such exercises that usually gulped huge sums of money. For instance, according to the NNPC only the Warri Refining and Petrochemical Company (WRPC) Limited, got all its process units running at over 70 per cent unit throughput during the year, this is even as industry experts question the authenticity of this figure.

The National Gas Policy, was signed gazette and implementation is said to have been fully commenced. The regulation emphasizes the gas flare commercialization. However, the sector has two main setbacks that had hitherto hindered its growth and development. These are infrastructure development as well as gas pricing in the local market which is said to have remained the obstacle of the gas to power initiative. NNPC secured financial assistance from China for the execution of the Ajaokuta-Kaduna-Kano (AKK) gas pipeline project in 2018. In June 2018, the country signed MoU with the Kingdom of Morocco on a regional pipeline that will supply gas to most of West African countries and extend to Morocco and Europe.

Finally, with FDI falling to record lows, it is imperative the President and the team he will assemble to begin the hard work of reassuring foreign investors as well as actually creating an enabling environment and 4 years measurable programs to encourage them to return with their funds to the oil & gas sector.

Mr. Buhari, President of Nigeria

I propose a 4 years term program tagged “Gas & Refinery Market Development Plan” it’s should include strategic roadmaps, performance metrics and lifespan for Phase I of 4 years starting August 2019 and ends 2024, with LNG Local Capacity utilization roadmap, investment long-term incentives, market opportunity analysis, industrial advantage the Oil&Gas of the country has in sub-Saharan Africa, Local Gas Technology & Talent Dev, Strategic Plans on Gas to Industry for West Africa market corridors, Gas to Power for both local & other rich market in SSA, Gas to Power Manufacturing and Steel Rolling Mills and Cooking route to market Plan within Nigeria and Africa Consumers.

Agriculture is a key economic sector in many countries around the world. In Sub Saharan Africa (SSA), the sector contributes, on average, 15% to the GDP of the region. More importantly, agriculture’s contribution to GDP reaches as high as 50% in Chad and ranges from 20-40% in the most populated countries in the region such as Nigeria, DRC, and Ethiopia. The sector is also important for employment – more than half of the total labor force in SSA is engaged in agriculture on smallholder farms (less than 2 hectares in size) that constitute approximately 80% of all farms in the region.

These smallholder farms are for the most part of the cultivation year rain-fed and heavily exposed to the impact of adverse weather patterns, which can be significant, also these smallholder farmers engage in a variety of plant or crop (purpose fit modern agro-extension) year-round is a most, if these group can concentrate on major produce or commodity per region yield year round, producing/supplying at ultra-scale enough for industrial utilization and market development, it’s would have huge trajectory effect on national agro-produce capacity and production Growth y/y, enough to feed a nation of 180 million consumers and yet export excess capacity( raw farm produce and processed commodities) to other state in Africa and beyond.

The reason behind shortage in supply across all major farm commodity y/y is basically because these Small Holder Farmers who forms 74% of farming industry, engage in a mixed variety of cultivation yearly, rather than concentrate effort, land, & time on a singular farm produce thereby reducing their supply capacity across the different major commodities.

E.g Tomatos Jos, as a foreign owned Tomatos Processor Plant situated in the Northern part of the country but this group activities had been bottle-necked with short-supply or epileptic produce of Tomatos (which an input for their own plant).

Thus, the local agro-processing and value chain would attract more investment and players that are able to process and sell to the Nigerian market and export excess capacity. The Federal Government needs to establish more Smalholder’s Agro-Development Finance program: this can transfer of such risks from individuals and institutions facing such risks to counter-parties that are better able to diversify and manage them. However, in Africa and across much of the emerging world, insurance and reinsurance companies have done a sub-optimal job of identifying, capturing and transferring these (Agro-related & small holder’s farmers risks) to market players who are best able to underwrite them.

Power

Nigeria has 12,522MW of installed capacity, but due to maintenance, gas, water and transmission constraints, an average of only 3,879MW of capacity is operational (January to 15 August, 2015). The majority (85%) of installed capacity is fuelled by gas. Availability of gas molecules is low due to insufficient production, economic disincentives, inadequate infrastructure and frequent vandalism.

The country’s transmission system has the capacity to transmit ~5,300MW but its disrupted by system collapses and frequent forced outages. Currently, transmission capacity is higher than operational generation capacity, but transmission will rapidly become a constraint due to increasing operational capacity. Although Nigeria distribution companies suffer losses, with ~46% of energy lost due through technical, commercial and collection issues. Nigeria remains world’s highest importer of personal generating sets with citizens spending large portions of their income on power generation while Africa’s largest economy struggles to generate and transmit 4 gigawatts of electricity – a fraction of what the city of London generates daily.

Thus, critical third tier energy infrastructure must now form a crucial and important area of focus of the Presidency administration this second term. I recommend an unbundling of the 3 in 1 ministry such that power is separate from works and housing in order to give it the focus it so deserves.

Crucially, there is a need to engage world leading power groups with long term strategic Joint Venture for local capacity and utilization development. I propose “Third Tier Power Infrastructure Strategy”, this strategy would help develop local energy infrastructure and deepen our capability has a nation to export excess capacity in Energy infrastructure to other developing countries in Africa and beyond (as energy infrastructure EOM country), while Local Disco, Genco, Operational and energy network infrastructure is upgraded, replaced and further strengthened with newer parts and machines in sharing formula model: Contributive ratio

– Disco & affected/benefiting Genco’s contribute 30%,

– FGN 50% (partly in kind, supply of gas, 3 free energy infrastructure industrial development parts in Lagos, Kano & Port Harcourt and provide all other possible resource to attract global players)

– Tax freedom 10% (for 10 years term)

With sincerity of purpose the likes of Enegie, Enel, Siemens, KEPCO, State Grid Corporation of China, TEPCO, RWE AG of Germany would come in and set industrial hubs for their energy infrastructure development that further serves the entire Africa energy market.

Insecurity

An ill equipped and poorly trained Nigerian military has struggled to press initial gains and hold on to territory, while the insurgents have become free to pick and choose when and where to stage attacks. This conflict has already caused irreversible damage to large areas of Adamawa, Borno and Yobe states, causing millions of Nigeria’s to be displaced internally and externally. Clearly a different approach is needed, perhaps a total revamp in the doctrine and training for law enforcement and military personnel in addition to funding.

Beyond the North East, the North Western states of Zamfara and Kaduna have opened new fronts of violence and now Sokoto has started to succumb as well. President Buhari must show that northern lives matter not only for votes.

I propose the creation of a “National Guard and a Special Forces Unit” in the Nigerian military. The National Guard (which some countries also refer to as the Republican Guard), will have chapters in all the states of the federation, be federally controlled, and tasked with the responsibility of protecting the Nigerian state from external aggressors. They should be trained in counter-terrorism strategies and tactics, asymmetric warfare, and desert warfare.

Besides, we should create a Special Forces Unit in the military that will be skilled in Search and Rescue Operations and endowed with the ability to launch precision strikes at enemy targets whenever the need arises. The issue of funding for these proposed security agencies does not arise as neighbouring countries with smaller populations and smaller economic resources already have these institutions operational in their security apparati. That is the reason why “Boko Haram” has been unable to gain a foothold in those countries or cause any significant damage unlike in Nigeria.

Corruption

Despite a below average performance in fighting corruption, this has perhaps been last administration most defining element. Having started strongly by implementing the previous administration’s Treasury Single Account initiative, and several high-profile arrests, the anti-corruption drive appears to have fizzled out.

Finally, a law should be enacted creating Federal Tribunals for Corruption offences (FTCO). The powers of such courts, sitting in Abuja and State capitals, and the form of sentences within their scope must be carefully spelt out, and the court or courts of final appeal specified.

Every American is wary of the US Internal Revenue Service (IRS), because it can land on anyone’s doorstep, at any time and indeed, the IRS has the power to examine anyone’s lifestyle and to ask for explanations about one’s sources of income, and woe betides anyone who is unable to account for any newfound wealth. That in a nutshell is the sort of social environment that must be established in Nigeria if a credible start is to be made in the difficult job of corruption prevention and eradication. I propose an arm established from both EFCC & FIRS, and modelled to work independently/autonomous like US IRS. e.g FCIR Financial Crimes & Internal Revenue TEAM…FCIR-t.

Federalism

Regardless of ethnicity and religion. Asides taking considerable time to reach crucial decisions nepotism and ethnic bias are the areas where this administration faces the greatest criticism. The federal government reluctance to entertain discussions around restructuring and true federalism may be rightly or wrongly attributed to ethnic bias but we all understand that Nigeria as currently constituted is not working and cannot support the aspirations of its citizens.

Thus, a need for national Dialogue and true Referendum on exactly what her citizens at every geographical territory and ethnicity truly wants and desire of a country called Nigeria, with no single group or particular people at disadvantage.

States in Nigeria

Electoral Reform

Many have believed the elections that delivered President Buhari’s second term were amongst the most flawed in Nigeria’s history. This administration failed to sign the electoral amendment acts in their first term at office, this would have ensured that the gains made in

2011 and strengthened in 2015 were made institutional. This is largely seen as disadvantage to a growing democratic system and a true independent electoral umpire in Independent National Electoral Commissions INEC activities.

The Federal government needs to swiftly start displaying true democrat from handling of national issues, to resource distribution and appointments of key government actors because this are most visible to the citizens. The administration needs to further build strong electoral agencies, structure and institution that are truly independent.

In conclusion, the new administration needs to swiftly focus on macroeconomic and structural reform priorities articulated in the country’s Economic Recovery and Growth Plan (ERGP 2017-2020)-breaking it into feasible and execution modular plans of 4yrs, that is measured and can be accelerated, that citizens and the economy as a whole can have a breath of New Growth.

A coolest aspect concerning jumpers watches, is that they are among the hardest watches on earth. These profoundly particular games watches are planned with usefulness first on the watchmaker’s need list. This is on the grounds that as a watch is exposed to more noteworthy profundity, the harder it must be to ensure safe activity in a pressurized situation.

How Divers Watches Are Tested

There is a severe worldwide standard that a genuine jumpers watch must fulfill so as to be a guaranteed plunging watch. Watches must breeze through a progression of tests spread out in ISO 6425, to acquire the privilege to print the words “DIVER’S WATCH” working on this issue. Any watch bearing this checking will have fulfilled the ISO 6425 testing technique that is an uncommon sort of certification that the watch will hold up under submarine conditions.

The primary test in the ISO 6425 technique is a buildup test. The test includes warming a plate to around forty to forty five degrees centigrade, the watch is then set on the plate and left for a time of ten to twenty minutes. Over this period the watch will warmth up to this particular temperature. Onto the watch’s precious stone face, a drop of water at room temperature is set and left for one moment and after that cleared off.

In the event that there is any buildup seen to shape underneath the gem face, at that point the watch comes up short the testing. No further testing is directed starting there on.

Another test in the system necessitates that watches be tried at profundities that are 25% beneath their evaluated profundity in still water conditions. Slight climate varieties can make the thickness of seawater vary from somewhere in the range of two and five percent and it is likewise settled by science that seawater is denser than new water.

Warm stun testing is likewise connected to the jump watch as a feature of the testing technique. The testing includes quick temperature changes. For a time of 60 minutes, the watch is first put in forty degree water, at that point when the time lapses, is quickly moved to five degree water. The watch is left for a further hour before being moved back to the forty degree water again for a last hour.

By a wide margin the longest test in the ISO methodology is to test the watch’s protection from the destructiveness of seawater and includes the plunging watch being submersed in thirty centimeter water for a time of more than two days. This is the reason most jumping watches are fabricated from hardened steel, titanium, plastics or earthenware production as these materials don’t rust.

Utilizing A Diver Watch Under Water

Jumping watches are additionally tried for the down to earth use of utilizing a games watch submerged. It is compulsory that all jumping watches have some system for monitoring the aggregate sum of time since the beginning of the plunge.

Most simple plunging watches utilize a unidirectional pivoting bezel to track jump length, the bezel must be turned one path and as a feature of the standard is required to have unmistakable markings at five moment interims and a size of an hour. The watch is required to have its 60/0 moment imprint be decipherable at twenty five meters beneath the surface and the perusing of the time intelligible itself. Simple plunging watches accomplish this with luminescent watch hands, while most advanced jumping watches execute this with an illuminated oris divers sixty-five watch screen.

Jumpers watches should likewise demonstrate that they are working, both at 25 meters and in complete murkiness. Simple watches have a running second hand with luminescent tip. At the point when the battery runs out they should introduce an “EOL” (end of life) pointer.

Jumpers watches are among the most thoroughly tried games watches on the planet, which means a decent one will probably last you for a long time and be totally sheltered to use in and around seawater, regardless of whether you are scuba jumper or not.

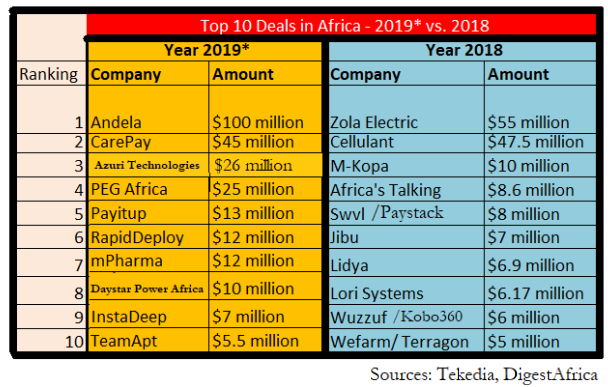

In recent times, the Nigerian FinTech ecosystem has witnessed strong drive and campaign across various frontiers including payments, personal savings, financial services, financial inclusion and mobile lending. This has precipitated the attention on FinTech companies and led to unprecedented growth in the industry in a short period. According to the Nigerian Start Up Funding Report, in 2018, Nigerian technology companies attracted investments of over N42 billion and 73% of this sum was invested in FinTech Companies. Also in 2018, wallet.ng, a Nigerian FinTech company was listed among the Top 100 FinTech companies in the world, in a report published by KPMG and H2 Ventures- the 2018 FinTech 100.

According to the Nigerian Startup Funding Report by Techpoint, Nigerian startups raised $17.6 million in Q1 2019, 8.5% higher than they did in Q1 2018. With the likes of Microsoft setting up digital villages in Nigeria, more Nigerian FinTech startups are leading the drive for financial inclusion in the continent.

Possibly, a large part of the industry growth is directly related to the amount of funding being pumped in by investors in the Nigerian FinTech ecosystem, as it is widely agreed that funding is important for FinTech companies to thrive.

FinTech companies like other companies in Nigeria, can have various sources of funding including debt or equity. With respect to debt, most startups may be permitted by their Articles of Association, to raise capital through debt from banks, financial institutions and the capital market, subject to regulatory requirement.

For a lot of tech companies, funding can be a major challenge at the onset, particularly when the product/concept is novel and innovative. Typically, the founders would raise the initial capital from individuals/family for the first few months or years of the business, before they are able to access external funds through seed funding or series round, to scale their business. This lack of funds or access to credit has resulted in the exit of some promising tech companies in recent years. As mentioned above, equity, debt and mezzanine financing are available funding options for new and growing tech companies, however what we see, is that most FinTech companies raise equity instead of debt, as investments have mainly come from venture capitalists and private equity firms.

These venture capitalist are incentivized to provide these funding, by the provisions of the Venture Capital (Incentives) Act LFN 2004 which provides some tax benefits for the Venture Capital Firms including; accelerated capital allowance for equity investment by a venture company in a venture project for the first 5 years of the investment; reduction of withholding of tax on dividends declared by venture projects to venture companies for the first 5 years from 10% to 5%; export incentives such as export expansion grants if the venture project exports its product; exemption of payment of capital gains tax from gains realized by venture companies for a disposal of equity interest in the venture project; and exemption from companies income tax for a period of 3 years , which may be extended for an additional final period of 2 years.

Most startups would go through a Series A, B and C round, and believe they have gained sufficient funding to grow and scale their business, add new products to their portfolio, and return good profit to investors. Still, there is the option of listing in the capital market and conducting an Initial Public Offering (IPO) to offer shares to the public, and this is not uncommon in international markets. In 2002, Paypal which was founded in 1998, raised the sum of $70.2 billion via IPO, and is presently listed as a Forbes Fortune 500 company. Also Facebook raised $16 billion via Initial Public Offering in 2012, and has become one of the biggest companies in the world. However, raising fund from the capital market seems not to be a popular option for most tech companies, as a result of the perceived difficulties in managing a public company and the stringent reporting requirements.

In recent times, the Nigerian Stock Exchange have indicated that it is planning to reposition the Alternative Securities Market “ASEM” which is the NSE initiative for SMEs as a “Growth Board” that will provide listing opportunities and capital formation for Startups, SMEs and Venture Capital/Seed companies with a keen focus on startups creating value with transformational impact on the market. Basically, the initiative allows the target companies to float shares with a more flexible regulatory system than is applicable to the main board or premium board.

The Growth board has an entry stage which is primarily targeted at startups, tech companies and venture businesses. It is imperative that the company is a public limited company in legal form i.e as prescribed by Section 24 of the Companies and Allied Matters Act. Other requirements include that the company shall have a market capitalization of N50m – N500m and a public float/minimum shareholders of 10% and 25 shareholders respectively. Continuing obligations and reporting include semi-annual and annual company’s statements, while the Nigerian Stock Exchange will provide strong support structures for the company including accounting, audit and legal services at a pre agreed and prepaid rate with the startup.

For these companies, the benefits of listing on the Nigerian Stock Exchange above other funding options include the highly liquid nature of the market, value creation and corporate governance. There is also the issue of optimal price discovery, greater brand profile and visibility for investors, customers and consumers. Through listing, these start ups are also sure of business continuity, recognition in global markets, transparency/credibility and an exit route for private equity and strategic core investors.

The companies listed on the growth board are supported by the 3 pillars of designated advisers, growth ambassador and NSEs institutional services. While the regulatory and governance pillars are designed to facilitate the growth and institutionalization of these companies, the institutional services relate to the NSE’s initiative via partnership with strategic providers to offer companies access to expert services such as leadership development, succession planning and formalization of business processes. This enhances the company’s capacity to define its business model and integrate it with its structures, systems processes and people. Some proponents also opine that accessing funding through the capital market would give these tech companies an easier capital flow while reducing the cost of funding.

It is believed that this option of capital market should be considered by FinTech companies, as it will boost global recognition, ensure customer confidence and good corporate governance which is the hallmark of stable and successful companies.

Chuma Akana is a FinTech lawyer and writes from Lagos.

DHL is scaling its eShop in partnership with MallforAfrica. Jumia operates in 14 countries – DHL eShop is in 20 countries. The biggest competitor Jumia has now is DHL. It has brought excess of 200 U.S. and European top brands like Neiman Marcus and Carters online to Africans. If you take DHL’s supply chain advantage through its existing delivery structure built over decades, you can see that its claim that it is “Africa’s Largest Online Shopping Platform” makes sense.

Why? Ecommerce in Africa will be won on logistics as that is where the marginal cost issue required for scaling is domiciled. According to McKinsey & Company consumer spending will hit $2.1 trillion by 2025, with e-commerce accounting for up to 10%, in Africa. Many will put money in this sector but if you do, do not ignore what DHL is doing as it is mopping the best online sellers – typically foreign brands – at scale.

All Together

When you look at the whole elements, ignoring the open market [the one everyone wants to take down], and Facebook and Instagram which are auxiliary competitors, the main competitor to Jumia now is DHL. With DHL’s logistics capability, it has the easiest route to become the Amazon of Africa that can help people buy things on Kenyan e-stores and get them next two days in Lagos. Those e-stores could be DHL eShops and that is why its positioning is strong in the continent’s ecommerce sector.