In the past, moguls built business empires by controlling Supply. By controlling supply, they were able to move the price equilibrium points to their advantages. Demand (the users) just went along. So, in the grand scheme of competition, rivalries evolved out of the needs to control Supply. If you control the supply of rice into Nigeria, you would make tons of money, as you can fix the price. If you control the supply of cement, the same happens. That same applied across markets and industrial sectors, from banking to real estate.

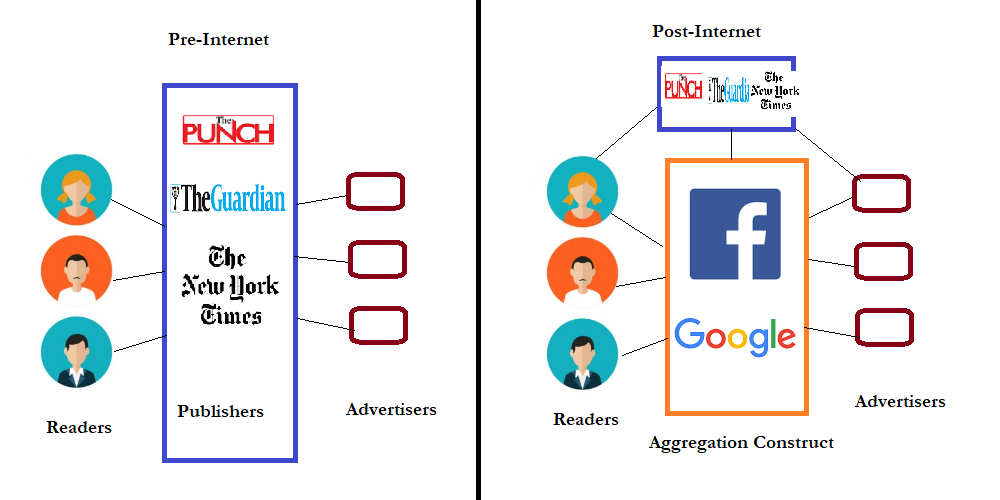

Today, in the digitizing internet world, the game plan is to control Demand (not Supply). It is assumed that Supply is already unlimited and there is no need to build capabilities to control it. If you want to control Supply, you would break in the Internet because you are absolutely going to fail. Yes, how could you control supply of all news posted on the web, from Twitter to Punch to Facebook? You have no chance – only aggregators are positioned for such.

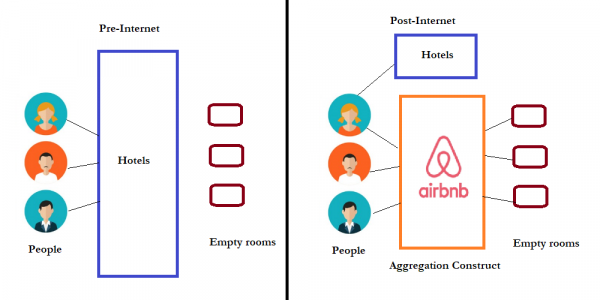

Airbnb controls Demand

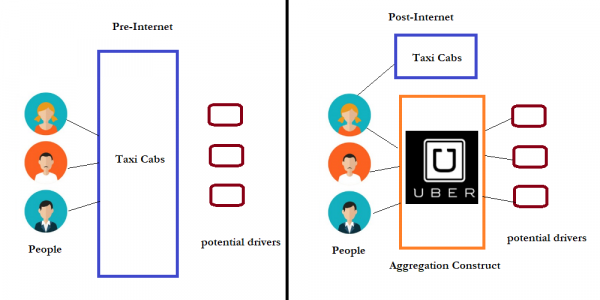

Uber controls demand

But in that web economy, there is a smarter strategy: control Demand. Simply, in a market that is unbounded by distribution mechanism and unconstrained by geography, the only remaining opportunity is controlling how all the supplies reach Demand (the users).

Magically, companies like Facebook, Twitter and Google focus on just that. They provide platforms that control Demand leaving the unlimited suppliers to provide the goods. Yes, you have the news (the contents), but if Google does not help to deliver them to the readers, you are in trouble. When Facebook revoked access to some websites after the debacle of Cambridge Analytica, many went bankrupt in days. Those firms had supply but they have been cut-off from Demand.

Facebook is going through a redesign with its privacy policy and strategy. The social media giant has started to significantly limit data access to Facebook’s Events, Groups and Pages APIs. It has also shut down part of the Instagram API. This is expected as the company battles scandals with the mess it found itself with the Cambridge Analytica related privacy violations.

Now, you can see why that your old book may not be helping your strategy as what worked in the industrial age economy might crash in the web economy. Sure, you can call Facebook and Google the modern supplies. But you must know they have no factories to produce the items you consume on their platforms. Google depends on all open global sites in the world to do that “supply”; Facebook feeds on stuffs we post. So, it is clearly not the type of supplies which used to break banks to execute. If you can “supply” their types of supplies, you are in control of Demand!

Comments on LinkedIn on this Topic

In this era of abundance on the supply side, the game has shifted to demand, turning entities with capabilities to control demands into the newest emperors. The digital supply chain even supports this model, where your superiority and differentiation is on your ability to stimulate demand, and also going ahead to decide who gets what.

It’s a radical shift, because for centuries, many things have been rigged from the supply side: just create artificial scarcity, and suddenly – more billions in your bank account! Times have changed, inventories are managed better, with less losses, meaning that you can technically stimulate demand, control the levers, without having ‘leftovers’ anyway.

With the way many things have been democratized, aided greatly by internet and web, tearing geographic boundaries along the way; households are turning themselves into mini factories, schools, markets, consulting firms, etc, without needing to break banks just to manage assets.

Human capital remains the most valuable asset in this knowledge economy, everything else is just a supporting cast.

This is the greatest time to be alive, if you are not living now; I am sorry!