In Africa, there is going to be a lot of disintermediation in the banking sector: many providers would be cut-out as companies reach end consumers. And that disintermediation will be enabled and anchored by the internet. So, if that is the case, winning the game of future banking would be driven by the quality of digital service experiences, and internet is going to become the ecosystem where that will happen. Like the disruption of Kenyan banking via MPESA which happened through mobile telephony, South Africa expects fintech to cause massive dislocation in the banking order.

Then with that knowledge, what do you do as a bank? You go and protect the flanks: you get a mobile virtual network operator (MVNO) license – “A mobile virtual network operator, virtual network operator, or mobile other licensed operator, is a wireless communications services provider that does not own the wireless network infrastructure over which it provides services to its customers”. Yes, you become a telecom company without physical assets. That is what Standard Bank has done, becoming the second bank in South Africa that has acquired MVNO license.

Standard Bank has finally confirmed one of the telecommunications industry’s worst-kept secrets: it will launch a mobile virtual network operator (MVNO), becoming the second major bank in South Africa to do so.

TechCentral first reported in February that Standard Bank is building an MVNO, revealing at the time that it had hired former Virgin Mobile South Africa CEO Steve Bailey to its executive team.

Standard Bank spokesman Ross Linstrom said in an e-mail in response to questions from TechCentral: “Yes, we are launching an MVNO. We expect to launch soon.”

Standard Bank joins FNB which unveiled FNB Connect in 2015 making it possible to serve its customers at scale without them spending any money on telecom charges. When I put these questions in LinkedIn based on the strategy that FNB has deployed, I got good feedbacks that a bank could technically win by delivering unmetered services to its customers.

1. If you know that a bank in Nigeria makes it possible that you can use its digital banking services (including web app, mobile apps, etc) even when you do not have mobile browsing credit, would it be a factor to open an account in that bank?

2. Then, you come to the bank for a problem, and it offers free WIFI to make it easier for you to deal with some issues you may be having, would that be a factor to open an account?

From the comments on LinkedIn, many people do believe that removing the mobile cost friction on top of delivery at par service quality would make them flip to use a specific banking institution. So, Standard Bank must have seen some movements for FNB to have responded by getting its own MNVO license. It is possible we would be seeing more banks going for MNVO. This is a typical case of moving towards the upstream to deliver unmatched value while your competitors are left in the downstream. When you do that, you would rewire the architecture of the industry competition. Provided the MNVO cost is well managed, this is a clear new basis of competition in the industry and could potentially help nip many fintech challenges.

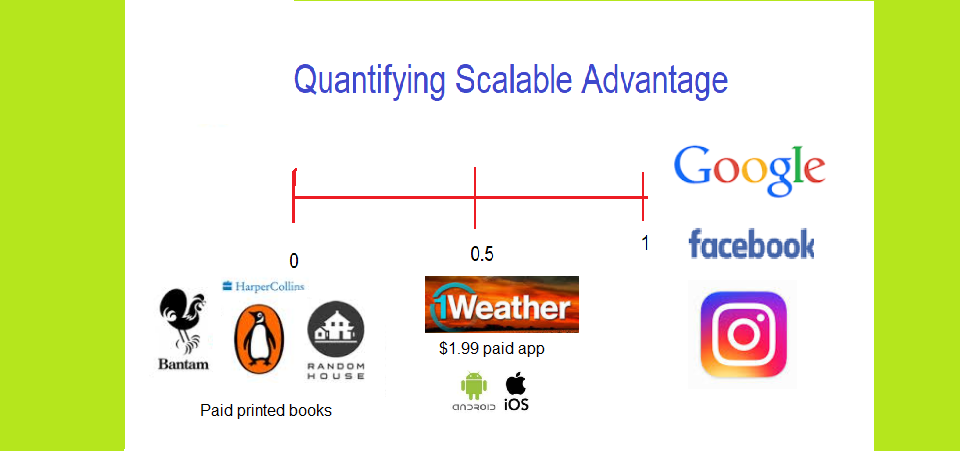

The Accumulation of Capability Construct teaches you how to separate from everyone by going upstream when most are operating at downstream. You get more value because you are handling bigger frictions and targeting severe pain points.

If you know that a bank in Nigeria makes it possible that you can use its digital banking services (including web app, mobile apps, etc) even when you do not have mobile browsing credit, would it be a factor to open an account in that bank?

Then, you come to the bank for a problem, and it offers free WIFI to make it easier for you to deal with some issues you may be having, would that be a factor to open an account?

A bank in South Africa has just executed some components of the above.

“The expansion of WiFi connectivity across our branch network is primarily aimed at giving customers easy access to digital banking platforms. The digital journey is enabled through sustained investment in infrastructure which continues to be intensified through consistent innovation across branches. As we evolve and build the branch of the future, we would like customers to be part of the journey as well,” chief executive officer of FNB Points of Presnece, Lee-Anne van Zyl said in a statement.

As many FNB customers are aware, data used to access the FNB app for smartphones was and still is zero-rated across all major local networks. So why then is FNB giving customers WiFi access at its branches?

I do believe that this strategy makes sense: you can even reduce the cost of service by making it easier for customers to serve themselves. Of course, this will work if the customers are fairly literate. Nonetheless, I expect this to begin to make way at scale in Nigeria.

Since I mentioned NIPOST (Nigerian Postal Services) in a recent post, I have been getting InMails and notes from people telling me that NIPOST has now improved. I must disclose that I have not used any of NIPOST’s recent services. This is a comment a user left in an old piece: largely, NIPOST is improving on its mission.

Very cool analysis Prof, as per your post about NIPOST they seem to be making moves

they’ve been quite active on social media and seem to be getting good reviews from Nigerians

In a piece in Vanguard, I can read of promises but no specific transformation which has been practically deployed by NIPOST. Yet, there is a very clear roadmap which the government is pursuing and which is interesting as the government wants to unbundle NIPOST to make it more efficient.

I pay a lot of attention on NIPOST: everything I have written on ecommerce (not an online store) is anchored on my thesis that if you do not deal with the marginal cost challenge associated with delivery and broad logistics in Nigeria, ecommerce would not be competitive compared with our open markets and supermarkets across Nigeria. The biggest element of marginal cost is distribution cost since transaction cost is always there. Only NIPOST can reduce distribution cost for ecommerce firms in Nigeria.

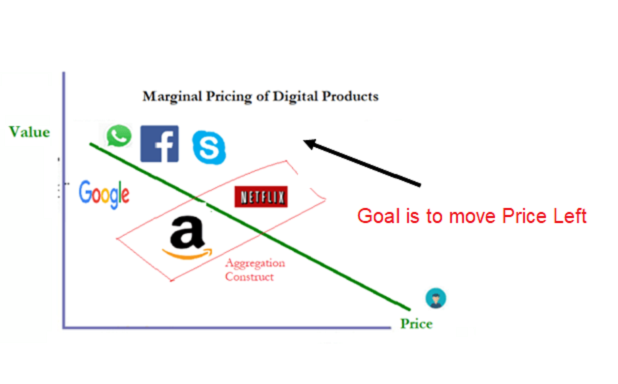

In a perfect market, the marginal cost of a digital product is zero. This means that the price of a digital product tends to zero: welcome freemium and ad-supported business. However, only firms with network effects dominate and benefit. The core reason is that if in a perfect market, and the marginal cost of producing digital product is zero, the price will inevitably go to zero.

NIPOST Impact

If NIPOST improves, the marginal cost problem will be solved, meaning that ecommerce companies can ship items at better cost margins. Possibly, that would help them compete better with open markets and supermarkets. Yes, if NIPOST takes over the distribution challenges, ecommerce companies will then become unbounded and unconstrained by geography, making them national players. Today, our ecommerce firms are not exploiting the true value of the web since most are focusing on specific cities – you cannot be doing a web business and be restricted to a small locality. So, if NIPOST helps to fix distribution, the ecommerce firms would become more valuable as the scalable advantage has improved.

All Together

As I noted when I commented on seeing my book on print for the first time, logistics is at the heart of ecommerce. I had written a book, submitted it to Amazon and waited for the royalties to arrive. I did not even bother to get a print version of this book! Amazon is handling all and selling the book across America and beyond. Amazon does what it does because the United States Postal Service provides deep support to reach any city and location.

If NIPOST can offer that in Nigeria, a new dawn will emerge in the ecommerce sector in Nigeria. Ecommerce companies will simply focus on making sales while NIPOST takes care of the distribution for them. And when that happens, they would have scale which will then make them very competitive on pricing compared with local open markets and supermarkets across Nigerian cities. That trajectory is how the ecommerce sector will blossom in the land.

The Nigerian Senate is inviting the Central Bank of Nigeria (CBN) governor to explain the amalgam of fees in the banking industry. Everything you do, there is a fee in the industry. It is extremely unfortunate that our banks have innovated excellently on extracting fees from customers at scale. Yet, I must note that some of those fees are not kept by banks; government is part of the party. Case in point: stamp duty fee for electronic transaction!

The Senate on Wednesday asked its committees on Banking, Insurance & other Financial Institutions and Finance to invite the Governor of Central Bank of Nigeria (CBN), Godwin Emefiele, to explain why its approved official charges are skewed in favour of banks as against ordinary bank customers.

The committees are also to investigate the propriety of ATM Card maintenance charges in comparison with international best practices and report back to the Senate.

These resolutions were sequel to a motion sponsored by Gbenga Ashafa (APC, Lagos East) on “Illicit and Excessive Charges by Nigerian Banks on customers account with particular focus on Automated Teller Machine (ATM) Maintenance and Withdrawal Charges.”

Mr Ashafa noted there have been several complaints from Nigerians generally and on social media concerning illicit and excessive charges by commercial banks on customers’ account with particular focus on ATM maintenance charges and ATM withdrawal charges.

I have written extensively that the clusters of bank fees are actually part of the reasons why the financial inclusion is not working as designed. When an average customer spends around N300 to N500 in a month on fees, you would get the idea why some Nigerians run away from banks.

But in Nigeria, there are many entries on all kinds of fees. I used to work in the bank in Lagos. But then, it was Commission on Turnover (COT) – this is the fee, the bank imposes on your account for actually withdrawing your money. I have called it one of the most ingenious products that propelled the new banking era in Nigeria. Without COT, there will not be many new generation banks. They offered better services than the dinosaurs of the older banks, but needed to monetize the obvious preferences of their services in order to invest in technology and new operational models. Customers knowing the value in better service did not complain. The COT provided easy cash and they triumphed, took market share from old banks. So, even if they do not make loans to earn interests, provided that customers are coming and withdrawing money, they would make money. That is a setup that will never fail. They bring the customers with efficient services and then charge fees on their accounts as they do transactions.

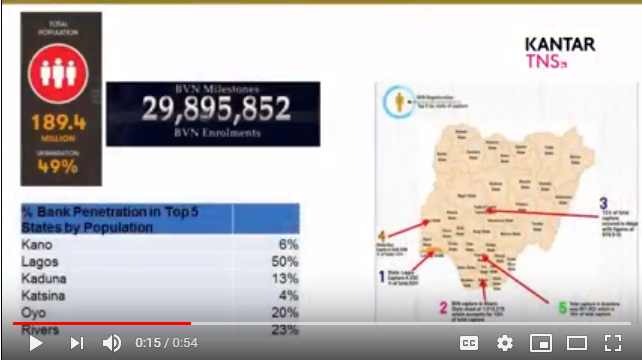

Get me right, the fees are actually a better deal if you are a middle class with change. It is far cheaper to save your one hour to watch Zee World by parting with N52 which you may pay as a fee to send money electronically. But that N52 does not come easily to many Nigerians. That is the reason why our financial inclusion remains low, according to some numbers from NIBSS (Nigeria Interbank Settlement System). Yes, Katsina has about 4% banking penetration using BVN (Bank Verification Number) data which is the most reliable in the nation.

The Bank Fees

According to the piece by Premium Times which was refereed above, the maintenance fees charged by banks on card maintenance stand at N600 per year as contained in “Guide to Charges by Banks and other Financial Institutions” which CBN published. It used to be N100 per year.

Of course the most troubling fee is the N65 which happens when one uses an out-of-network ATM from the 4th time in a month. In other words, there is no fee for the first three uses for any 3rd party ATM but once that is exceeded, any subsequent use attracts N65. While that fee is disclosed, the problem here is that some banks do rig the system by making sure people pay that fee not necessarily by choice. These are issues the consumer protection watchdog should be dealing with in the nation.

Mr Ashafa also expressed worry that most banks have deliberately manipulated their ATM not to dispense more that N10,000 per withdrawal in some cases and in most cases not more than N20,000.

“This is a deliberate ploy to manipulate the ATM machines which are ordinarily manufactured to dispense as much as N40, 000 per transaction, in order to attract more bank charges from customers who are forced to carry out more transactions due to the manipulated machines.

“It appears the CBN is becoming insensitive to the plight of Nigerians who are already complaining of excessive charges by commercial banks. If the CBN is trying to encourage a cashless Nigeria, why should they be making it more difficult and expensive for Nigerians to do transactions,” he said.

Of course while the Consumer Protection Council (CPC) has been going after DStv, protecting the interest of rich Nigerians who can afford shows, the real ordinary Nigerians are not protected by CPC when it comes to bank fees. The banking fees are more urgent issues than what DStv does with its pricing: we can live without DStv but there is no nation without banking!

CPC should focus more on bank fees on all Nigerians over pursuing fees DStv is charging Nigerian middle class.

For most Nigerians, you cannot charge them N1,200 for card issuance or renewal and then collect another N600 yearly on top of that. And whenever they make a transfer, there is a stamp duty for an electronic transaction. In all these cases, the customer cannot opt out because the alternative, using tellers is even more expensive. So, due to these fees, the only thing most poor customers do is to stop banking and use their pillows to store the little money they have. That may not be the expected thing CBN had hoped for, but its policies and what the banks are doing are simply enabling such decisions across the nation.

NIPOST Stamp Duty

The Federal Government of Nigeria is planning to privatize Nigerian Postal Services (NIPOST). I expect the price tag to be at least N100 billion. Why? Provided the electronic stamp duty remains in the Act, there would be no risk for buying NIPOST. You can recover at least N40 billion from its real estate across Nigeria. The balance will come from stamp duty which banks help you collect as Nigerians make electronic transactions daily.

The Bureau of Public Enterprises (BPE) on Thursday announced plans to generate N400 billion from the privatisation and concession of six Federal Government enterprises, including Afam Power, NIPOST and four others this year. The N400 billion, according to BPE, is part of its funding for the 2018 budget, which it ought to generate.

Yes, you just wait for banks to send you N50 for any electronic transaction as stamp duty. The good news is that you do not even have to print any stamp since the “stamp” now is digital. This is how lucrative NIPOST is: it is making money without having to move any package because Nigerians pay for stamps which are electronically issued!

What transactions attract 50 Naira Stamp Duty Charge

All received credit alerts to your bank account (current or savings) attracts a 50 Naira stamp duty charge.

The Receiver pays the 50 Naira, not the sender. So you don’t get charged stamp duty for debit transactions.

Where does all revenue from Stamp Duty Charges go

All stamp duty charges collected by Deposit money banks and other financial institutions are paid into the Nigeria Postal Service (NIPOST) collection account with the Central Bank of Nigeria 3000047517.

What the federal government chooses to do with this new revenue stream is yet to be established.

All Together

Nigeria needs to reform fees which banks and the government charge bank customers if the nation ever hopes to move the needle on financial inclusion. You do not expect extremely price-sensitive citizens to not factor these fees into considerations as they decide to join the industry. Yes, those fees could be discouraging the very people the government wants to attract into the banking sector. For someone making N18,000 monthly and having to part with N300-N500 on fees and associated SMS charges, it could be a disincentive to bank.

When do you know when to waive the opportunity to send invoice to a client? And when do you know how to intermittently freeze sending invoices to a long-term client? And when do you offer your structures to help your clients save money by relying on your systems? And when was the last time you brought a business to your client?

There is a clear advantage on running a consulting boutique not tethered to big global consulting firms: freedom to innovate on relationship building. Building a business relationship and making yourself a trusted ally would not happen overnight: you must earn any trust by investing in your clients, demonstrating that you want them to WIN.

Do not make money to anchor your advisory engagements: focus on value to be created to that client. If you do that, you would have a separation from competitors. Yes, it is incumbent on you to demonstrate why you are unique and demand to be paid by perhaps more experienced business legends. If they see the value to be created, the vaults will open, for you. When companies are looking for business insights, they know they would pay. But just as they are “confused” [they do not have all the answers], they would not like to retain and pay for “confusion”. That is why inertia exists to just hire: they want certainty on the value to be expected.

Interestingly, the easiest way is to start working even before the client finalizes on some issues, if that opportunity is possible. Send a roadmap with clarity on how you would go about fixing the business friction. Before the client knows it, you have something on the table. I know many people are fearful of others stealing their knowledge; I have always seen that concern as pure ignorance. If people can steal your ideas through a written document, you have nothing to offer at a deeper level! If you do not get out of that thinking, you would not even have a way to demonstrate capability before clients.

As you work, you must make efforts to understand the pain points, working to fix the main friction in that business. As you design roadmap, present what I have called Unification of Three: a concatenation of World, Africa and Nigeria. Then posit why your client in Nigeria will win with a specific action plan. You can only build confidence in that client if you demonstrate you have a clear understanding of the world and the continent even though the game would be played in Nigeria. Do not give him the opportunity to remind you what they are doing in New York and Kenya: offer them and then architect a roadmap taking into considerations the local terrains and realities in Nigeria.

Numbers matter but I can assure you that what is really catalytic is measuring the important things. Yes, do not be too fixated on capturing every metric. Find ways to know what matters. How do you grow or help that client scale? My message is to watch the marginal cost and from that elemental business component of scalable advantage, develop a model. If you miss it, you will never scale.

No matter what the engagement is – think growth because at the end every firm wants to grow. Do not limit your imagination on the written scope for the sake of it – liberate and while adhering to scope, find vistas to unlock value for your client.

There are things that bring more engagements – one of the key is making clients WIN and that is simply GROW. If you do not have a game plan on how clients can grow, go and acquire the capability and return. Yes, without the growth capability, no one will remember you afterwards, as the clients did not experience moments after your encounters. By looking at the end goal, even an IT engagement will be correlated to business objectives. By linking all those nexus, you become a trusted ally who can figure out how technology expands the business and not just IT department.

Have a great week ahead.

Comment from LinkedIn

You cannot manufacture a car by simply reading a book with a title: How To Manufacture Car. What makes the engine to come alive is not in that book, it’s located somewhere else. Same goes for ideas that can be stolen, the originality of such ideas is obviously debatable.

If you can bring universal problem to specifics, and tailor it down to client’s challenge; and on the other hand, can extrapolate specific challenge to solve universal problems, you will remain eternally relevant.

At the end of the day, it boils down to EXECUTION. It’s not so much about what was said and how it was said, but rather who acted on what was said, and the level of conviction and enthusiasm therein.

Like the Divine Master admonished in the holy book: Go and Do Same!