I have just accepted an invitation to speak in the 2019 Horasis Global Meeting. The event is co-hosted by the Portuguese Government and the City of Cascais. From the invitation letter:

I take great pleasure to invite you to speak at the 2019 Horasis Global Meeting to be held in Cascais, Portugal over 6-9 April 2019. Under the theme Catalyzing the Benefits of Globalization, the Horasis community of more than 600 selected world leaders (including several heads of governments) from 70 countries will gather for an unparalleled experience devising novel ideas to sustain and nurture our development in the future.

Attending this invitation-only event are prime ministers, presidents, chairman of major global banks and CEOs of many Fortune Global companies.

The annual Horasis Global Meeting is one of the world’s foremost gatherings of business leaders who interact with key government officials and eminent thought leaders.

Horasis is an independent think tank based in Zurich, Switzerland. It holds invitation-only meetings of global business leaders. From its Wikipedia page, the think tank has been dubbed “a kind of junior league World Economic Forum for the emerging market set” by The New York Times.

It would be a fascinating moment to spend the days with these world leaders as we continue to deepen our thought-leadership in Africa and beyond.

There is one area I have sympathy for African telecom operations: multiple and excessive taxes and fees. Sure, I do know that customers do end up paying those fees and taxes since the operators transfer them into their pricing models. But that does not mean that it does not hurt the operators; some customers may drop the services if the fees are high which would not have arisen if the telcos did not increase prices to cover the fees and taxes.

According to ATCON, a telecom industry association in Nigeria, operators are exposed to dozens of fees and taxes. Nigeria upped the game recently with 0.005% on electronic transaction bringing everyone in the party, from fintech to banks. Around the continent, it is the same story: telecommunication sector is the default industry to fund one (small) government idea or another, via fees or taxes. With millions of users in the networks, enact the fees, money flows in days into government purses.

The Association of Telecommunications Companies of Nigeria (ATCON) hates that because it would make your phone calls and browsing more expensive since telcos would pass the costs to you. Banks, insurers and fintechs would also help to collect the new levies since anything electronic transaction would be levied the 0.005%.

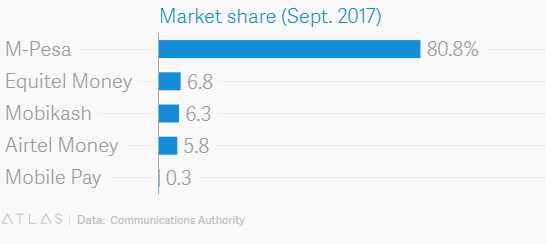

But what is happening in Kenya is taking this to the next level: 2% mobile money tax on transfers.

A proposed tax increase on mobile money transfers in Kenya is drawing protests from several services, including M-Pesa.

As part of a new tax proposal to raise government revenues, Kenya’s government is pushing to raise duties on mobile cash transfers by 2%. The government expects to net around $270 million in additional revenues and claims the extra income will fund a universal health care program to cover all households by 2022.

I hope they do not do it. If they do, some of the gains via mobile money could be gone. That is exactly what Safaricom, the owner of MPESA, noted: ‘it will “negatively impact mobile-led transfer services and payments” and reverse the gains of financial inclusion by making it more expensive to conduct business transactions and make payments using mobile money services”.

MPESA leads Kenya’s mobile money market. I do hope government understands the risks of making transfer very expensive for the citizens. Excessive mobile money tax will not help the poorer citizens; most would go unbanked!

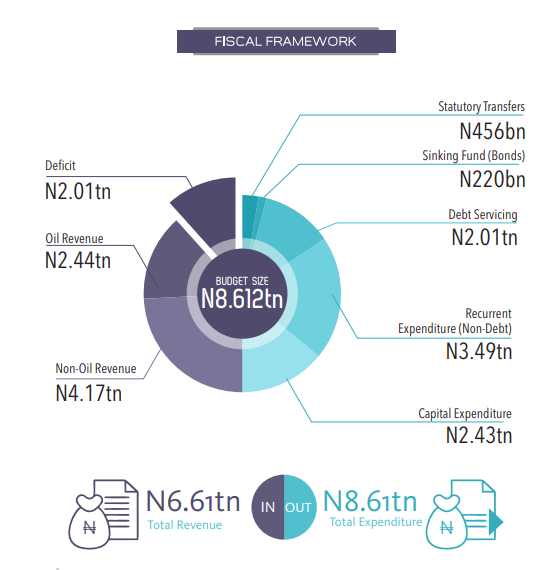

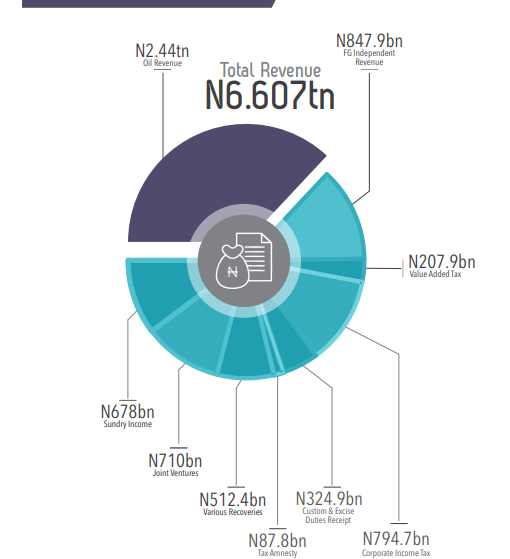

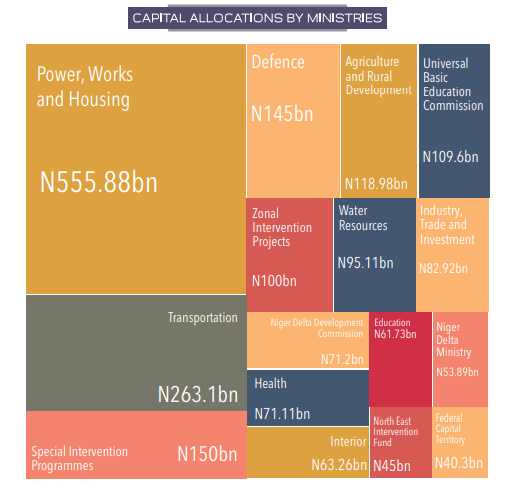

The President of Nigeria has signed the 2018 Nigeria budget. This is the breakdown of the signed budget, according to Premium Times. You can refer to the 2017 Nigeria’s federal budget here.

The total budget is N9.1 trillion, up from the N8.6 trillion estimates he submitted to the Assembly on November 7, 2017. The National Assembly raised the total figure by N500 billion.

They also increased the oil benchmark proposed by the executive from $45 to $51 per barrel.

The Assembly, however, retained oil production volume proposed at 2.3 million barrels per day and an exchange rate at N305 to $1.

The budget as passed by the two chambers also has N530.4 billion as statutory transfer; N2.2 trillion for debt service; N1,95 trillion as fiscal deficit.

Notice that the official rate of Naira to $1 is N305. The full proposed budget before the National Assembly added the N500 billion is here (pdf).

2018 Nigeria Budget (source: BudgIT). Note this plot did not capture the additional N500 billion added by the National Assembly.

General Electric (GE) fades. The Dow is replacing the iconic American conglomerate with Walgreens Boots Alliance. Yes, the GE Management Factory seems to have stopped working as the paralysis continues with no break.

S&P Dow Jones Indices announced on Tuesday that the iconic maker of light bulbs and jet engines will be replaced in the 30-stock index by Walgreens Boots Alliance. GE was an original member of the Dow in 1896 and has been in it continuously since November 7, 1907.

Being ousted from the Dow is the latest indignity for GE, which is dealing with a serious cash crisis caused by years of bad deals. GE has replaced its CEO, slashed thousands of jobs and cut its coveted stock dividend in half.

The decline of GE should teach us a lesson on management. At its peak during the golden years of Reginald Jones and Jack Welch, GE was the management factory where American companies went to hire their leaders. That was then – a really long time indeed as GE needs vision with the fierce urgency of now.

GE used to be the gold standard on the development of management systems and processes. At its zenith, GE was known as a factory where some of the finest business leaders were incubated, nurtured and prepared for leadership. With peerless business management and training systems, GE supplied a generation of CEOs to corporate America. The company pioneered and scaled many industrial age management systems and sold them across the world. One of those systems is the Six Sigma: Six Sigma was invented in Motorola, GE through its former leader, Jack Welch, popularized it when the company adopted it. As Toyota perfected its Kaizen and Japan pursued Total Quality Management, GE gave America management systems for growth and success. But that was the old GE; the present GE is sick

Today’s GE is using the management principles of the industrial age conglomerates in knowledge-based economies. For a company that prides itself as a center of management systems to fade in this way is unfortunate. The implication is that GE may be out of sync with the tenets of modern business processes. The industrial age has passed, and now it needs to learn what works. The strategic mistakes over the last ten years have been constant, and if GE does not stop making them, this iconic American company may go.

As GE makes way, Amazon, Alphabet (parent of Google) and Alibaba are pioneering new models of conglomerates. These new breeds are not called industrialized conglomerates but digital conglomerates. They do not require huge capital (relatively) and they are built on platforms which generate moats through network effects and positive continuum of the winner-takes-all. They could have taught GE some things but GE was far with its own disappearing world.

Yes, as the dawn of the knowledge economic systems was evolving, GE was selling its financial services to invest deeper in the old business of power generation and turbines. With solar and digital systems, most of those big pockets power turbines are “disintermediated” and that is partly why GE is struggling. Who needs a power plant with capacity of 4,000MW when you can get pieces of 1MW of solar plants across the country? Without those big huge contracts, the business model of GE was affected, and with the cash cow financial services already gone, GE was left bare.

The company would be back but it is certainly not going to be as powerful as it was. But no matter what, it needs to send its managers to Alibaba, Amazon and Alphabet for the modern management tutors, structured for the 21st century markets. Whatever GE Management Factory has been teaching in the last ten years is not working – it needs to update its curricula. No matter how you see it, GE needs to update its management curricula!

I was still in secondary school when Diamond Bank introduced its peerless and highly acclaimed Diamond Integrated Banking System (DIBS) in early 1990s – a solution that made it possible that you can operate your bank account irrespective of the domicile. Before DIBS, in a world dominated by First Bank, Union Bank and defunct Afribank, if you have an account in Aba and you happen to be in Lagos, to get your money, you must physically return to Aba branch of the bank.

For most businesspeople, there was no need of running bank accounts; they moved with their Alvan Ikokus. As Lomaji Ugorji helped us in his memorable adverts for defunct Equatorial Trust Bank, going to a bank was only possible if you could go with your mat. Yes, spending a whole day – 6 hours – to get money from your account was typical.

As I have written, DIBS reduced armed robbery along Onitsha-Lagos road more than any effort put by the Nigerian Police. How? Merchants would open accounts in Diamond Bank Onitsha branch. They would travel with their cheque books to Lagos. Reaching Idumota and Alaba, they would go to the bank’s branches to collect their monies. Magically, robbers who robbed luxurious buses like Young Shall Grow and Chisco which used to carry tons of cash would not find cash! With success factor very low, many criminals exited the routes at scale.

Human-Platform Banking

I really love this bank; I worked in Diamond Bank. It is a matchless institution when I was there. I was extremely motivated to work in the bank because it was extremely innovative. That was the only interview I ever attended in Nigeria and the only job I applied post-graduation. The other job offers came without interviews typical for class best graduating students in Federal University of Technology Owerri. I remain thankful they hired me.

Fast-forward, the bank is at a new game: human-platform banking. People call this agency banking. That is fair, but for me, it goes beyond agents if you read one of the key components of the CLOSA account (the bolded section below).

“Part of our activities in this space include the development of products such as the BETA and CLOSA accounts. BETA targets market traders and also supports small and medium enterprises (SMEs). The BETA account employs agents (called BETA friends) who go to the areas of comfort of these market traders and offer them all the financial services they need without impacting on their way of life, whilst the CLOSA account was created for those without Banks in their areas. People of influence in the community were selected to act as agents of the bank to ensure trust and those in the community were assured that the Bank would assume responsibility for their money once it was deposited with the agents.” Diamond Bank

In most parts of the world, you would build digital platforms to build that intermediation between partners (see my Aggregation Construct). But in Nigeria, we are way behind on the enabling infrastructures and elements for such. Yes, many of our citizens are not yet in digital ecosystems. So, to fix that problem and drive financial inclusion, the bank is seeding the human equivalents of those digital platforms. The “people of influence” like headmasters, imans, and local preachers would become the platforms between the bank and their customers.

All Together

Diamond Bank redesigned Nigerian banking with technology by inventing DIBS, a perception product as I have noted many times. It wants to re-invent it in a new way. With this human element, pioneering at scale human-platform banking, the agency banking will pick up massively.

Agency banking with proprietary technology supported with tokens, phones, BVN and mobile kiosks will deliver the magic. The transactions will be capped to avoid fraud and risk-management tools embedded. As these agency banking systems mature, banks can close and sell off expensive branches which may not be necessary in 5 years as the immersive digital economy evolves.

The path to onboard many Nigerians into the financial systems would involve reaching them at the levels they are, right now. It may involve thinking less of bytes and more of atoms. Yes, human-platform banking over digital-platform banking.