This is what is called “head, you win, and tail you also win”. So, WhatsApp desires to make sure that it disrupts phone calls which remain a very popular way of handling customer requests. It imposes fee conditions in a way that it could stimulate demand from users without destroying service experience. So, over time, everyone will adopt WhatsApp because they have gotten quicker responses using it. It is a growth feedback loop which is a positive continuum. I am very confident that AI was used to design this one. This is loop (or circular) pricing model.

After getting acquired by Facebook for $19 billion in 2014, it’s finally time for the 1.5 billion-user WhatsApp to pull its weight and contribute some revenue. If Facebook can pitch the WhatsApp Business API as a cheaper alternative to customer service call centers, the convenience of asynchronous chat could compel users to message companies instead of phoning.

Only charging for slow replies after 24 hours since a user’s last message is a genius way to create a growth feedback loop. If users get quick answers via WhatsApp, they’ll prefer it to other channels. Once businesses and their customers get addicted to it, WhatsApp could eventually charge for all replies or any that exceed a volume threshold, or cut down the free window. Meanwhile, businesses might be too optimistic about their response times and end up paying more often than they expect, especially when messages come in on weekends or holidays.

To all users of Zenvus Boundary, today we added a feature which makes it possible that once a property boundary has been recorded within Zenvus Boundary ecosystem, an alert will be triggered if the same boundary is captured by another user. For instance, if you use Zenvus Boundary to map the boundary of a farm, and next week another person (not in your specific Zenvus Boundary) maps at least part of that farm, our system will detect a conflict, triggering an alert to Zenvus Boundary support. We will contact both customers to note what our system has detected.

Zenvus Boundary maps farm, land or house perimeter boundaries, calculates the areas and populates the data onto Google Earth. From Zenvus portal, the surveys can be downloaded or printed. It supports cooperatives, governments and individual farmers, enabling these entities to have survey reports at a fraction of the typical cost of surveys.

Until that is resolved, our Property Search feature will blank the names to avoid either using the property to access loans and other services. The individuals can resolve the problem via government data, oral history, etc. Zenvus Boundary neither offers legal advisory services nor government support services.

You want to be a Zenvus Boundary partner? Click here.

WhatsApp Payment has arrived in Africa. That has been expected since there is no clear path to monetize WhatsApp without subscription which Facebook has no interest in pursuing. Advertisement may not necessarily work for WhatsApp if Facebook hopes to keep the customers happy. So, here we go: WhatsApp payment is here in Africa.

As of Wednesday (August 1) South Africa’s Absa Group officially rolled out WhatsApp banking as part of its continuing effort to develop a digitally-led bank in Africa. Absa has signed on 10,000 customers since early July, according to Reuters.

{…}

“As technology advances and more customers become connected, bringing banking to where our customers are is important to us, especially as we continue our journey to become a digitally-led business driven by innovation,” chief executive of Absa retail and business banking Arrie Rautenbach said in a statement.

The addition of WhatsApp banking is part and parcel to a growth plan for Absa that observers have called “ambitious.” The goal — once it has completed its separation from Barclays — is to capture (and in some cases recapture) market share in South Africa and double sales across the African continent from 6 percent to 12 percent. WhatsApp allows Absa to offer banking services that are available anywhere, anytime, to customers that want to use it.

Absa’s WhatsApp service, ChatBanking, will mostly be simple banking transactions. Users will be able to check their account balances and make payments to existing beneficiaries using brief and natural sounding conversational commands.

The Massive Dislocation

This will be a huge challenge to African fintechs. Payment is going to see massive dislocation because it is always harder to pull people from the ecosystem where they are to another. In others words, why would I launch a fintech app when I can make that payment via WhatsApp which I am already using with that client? The launch of WhatsApp payment in Africa is a big deal for the local banking and payment ecosystems.

I noted few days ago that WhatsApp’s move into payment would cause massive dislocation in African banking. In this age of chat and social media, transactions have evolved into content, commerce and financial services. To examine the impact in Africa, let us consider what these solutions have done in India where they are already or being deployed. India has about 250 million WhatsApp users, the world’s largest (China is a WeChat nation).

New payment trend in India

All Together

As I wrote few months ago in Harvard Business Review, companies like Facebook, the ICT utilities, can bulldoze themselves into new sectors. Adding payment in WhatsApp is industry-shaping. Largely, we have entered a new dawn where transactions have evolved into content, commerce and financial services – the so called social commerce which WeChat had perfected.

Going forward, I expect new basis of competition with disruptive consequences in the African payment markets. Simply, the game has changed and everyone has to evolve: WhatsApp payment is possible the single African currency; Google Tez is on the way. The good news is that African consumers will experience lesser payment frictions, and that could be a good thing across many communities.

In coming days, I will be on my way to West Africa. We will be spending 6 weeks starting from the Centre of Excellence (Lagos). We will launch a new business and also use that time to meet current and new clients on our advisory services. We remain the largest embedded electronics company in Africa – the larger of only two Intel FPGA partners. We also help startups, banks, insurers, etc deepen their capabilities through seminars and presentations. From agtech to health-tech, electronics to advisory, we have a mini-diversified digital conglomerate. Email me or team (below) and let us schedule time. Let us work together to fix that market friction.

At Fasmicro Group, we do not recite numbers and tell you what you already know: we deliver unparalleled insights through uncommon perspectives shaped by our experiences as entrepreneurs and advisors in the markets. Our moments are unique because things we share with clients are shaped by our direct exposures to the markets. Fasmicro Advisory Services solutions are structured as follows:

Development of Business Roadmap & Strategy: A business plan is not enough to anchor business execution. A Roadmap Document is required especially in a sector which is in a state of flux [changing market, changing model, startup, competition, regulation, etc]. To avoid pursuing many windy paths or dead ends, a roadmap helps to encapsulate a profitable path to the vision with pillars and enablers necessary for success. Read more here.

We will conduct a review of the Firm’s current strategy, and identify the current gaps considering the business needs and market best practices and make recommendations to implement the strategic gaps with fit for purpose solutions in line with global best practices and local realities.

Discovery Innovation Workshop: To innovate is to set a new basis of competition in an economy, business sector or market. Typically, it results to disruption. This workshop will focus on innovation and growth because growth is the reward of innovation. Otherwise, that innovation is actually an invention. I will be the lead instructor with my supporting crew. The table below provides the workshop structure. We can adapt this workshop to two days.

The Category-Kings Benchmarking [Local & International]

Innovation Execution

Discovery Innovation Presentation:This is a two-hour seminar where we will present what is happening in your market, customized for your company, and then offer insights on how you can plot your strategies to win. This goes beyond industry statistics and typical SWOT analysis. We work to help clients see their markets in new ways, providing roadmaps on how they can unlock opportunities. It is an intense talk, combining technology, finance, political economy and strategy. As technology redesigns markets, I break the implications in short, medium and long-terms.

Case: How can a (mall) real estate developer understand that ecommerce is a tangential threat since malls can be disrupted by digital commerce in future? My client now considers triple-play designs where malls can be converted into offices or homes, in case the moment comes.

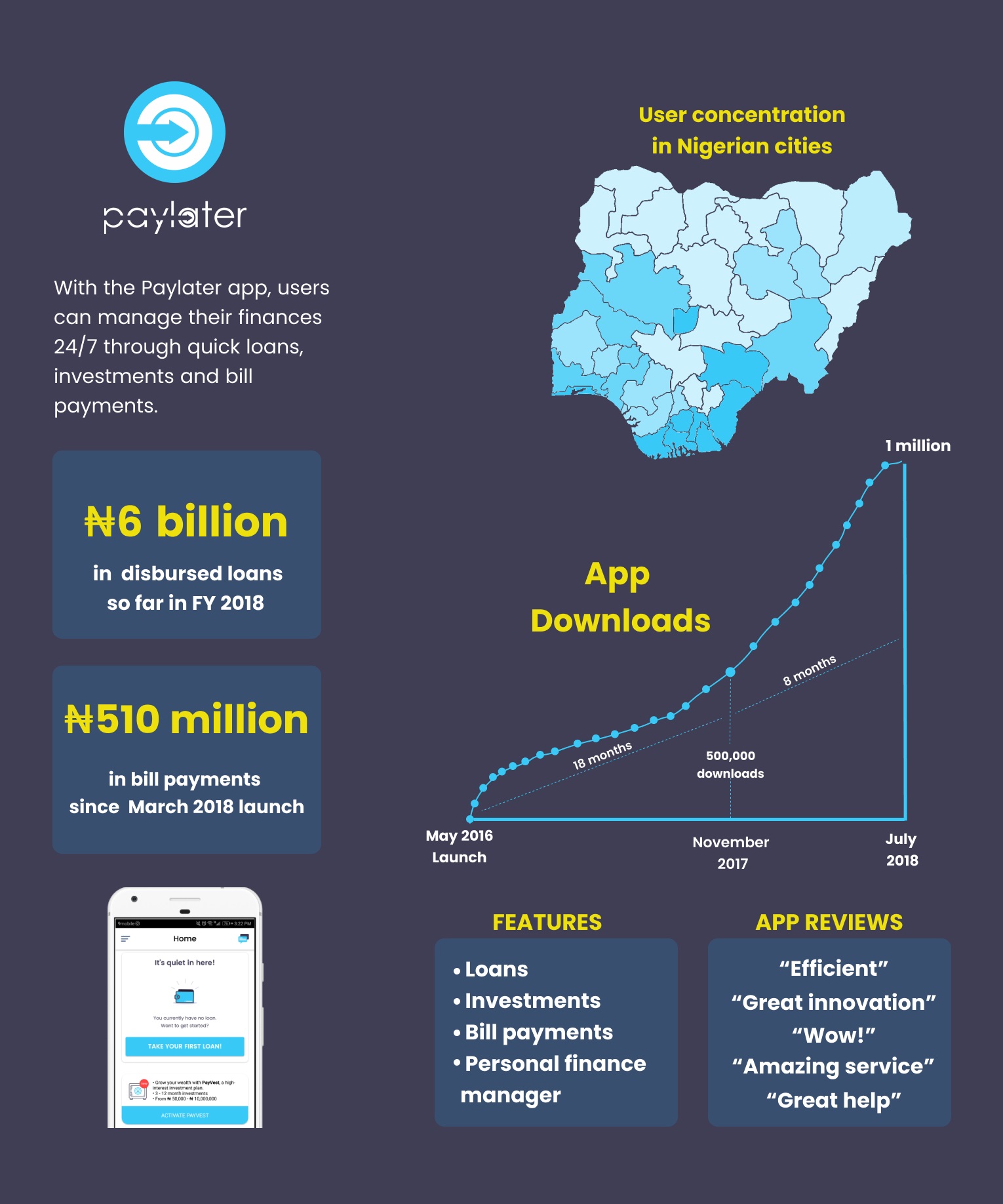

Paylater, the fintech company which pioneered micro-lending in Nigeria, at scale, has hit one million app downloads. I wrote about this company and called it a brilliant business. With this growth rate, Paylater could be the largest “Nigerian bank” with no bank license by 2025. It will eclipse three banks in customer base possibly by the end of 2019.

That is why Paylater is exciting. Owned by One Finance & Investments Ltd,Paylater is going after that market where the highest pain points are found in the Nigerian banking sector. We can surely live without shopping through the modern digital payments. But we know that it is challenging when there is an urgent need for funds and no friend or family can help. That is what happens across Nigerian families today. Challenges go beyond how to move money fast across digital channels. Simply, we want credits. Paylater focuses on short-term loans, mainly for emergencies.

The mobile app provides Nigerian consumers with access to credit. And it does its entire works completely digitally, without seeing or speaking to customers. Call it AI or analytics, it is a leap ahead.

From an email sent to Tekedia, the company has disbursed N6 billion in 2018 alone.

In Nigeria, a country of nearly 200 million people, 61% of the adult population is un- or underbanked. Fintech companies like Paylater represent a tremendous opportunity to get formal banking services in the hands of Nigerian consumers to provide much needed liquidity for entrepreneurial investment, personal development, or unexpected expenses.

Consumer credit is nearly non-existent in Nigeria. But, Paylater is issuing loans to Nigerians completely digitally, without seeing or speaking to customers. Customers can receive funds in their account in as little as 5 minutes, with no need for paperwork, collateral or guarantors. Digital financial services platforms have been well received by consumers and it appears that fintech platforms like Paylater are here to stay.

The evidence is in the numbers. With over 800,000 registered users, across every Nigerian state, Paylater has loaned over $17M USD to Nigerian consumers in 2018 so far. The technology platform has supplemented that loan growth with very strong early adoption of its bill payments and investments features as well.

“We are very excited by the market adoption of Paylater and we believe there is still a significant growth opportunity ahead for digital financial services” – Co-founder and CEO Chijioke Dozie

Before Paylater, only commercial banks?—?with physical branches nationwide and extremely large capital bases?—?had the reach, stability and customer trust to offer financial services to a variety of people. Unfortunately, these same institutions turned record profits by taking deposits from average consumers, and reserving actual ‘banking’ services like loans and investments for large corporate entities and high-net worth individuals.

Access to credit is a fundamental human need and the foundation on which most modern economies are built. Pioneers like Paylater have embraced the difficult task of unlocking the power of financial access for the underserved, and so far, it looks like they are winning.