Online gambling is changing rapidly, but the true revolution no longer comes solely from jackpots or graphics. Today, the industry is adapting above all to a new way of consuming digital content: fast, vertical, emotional and ultra-mobile.

TikTok has profoundly changed digital habits worldwide. Users swipe from one video to the next in seconds, seek immediate stimulation and respond strongly to short, high-emotional-intensity content. This logic is now directly influencing online casinos.

In Senegal, where smartphones dominate digital usage, this evolution is becoming particularly visible. Many users discover mobile platforms through searches like Paripesa bet while looking for faster and more interactive experiences. In this context, Instant Games are experiencing spectacular growth.

Crash games, mini-games, “tap-and-win” formats and ultra-short experiences are increasingly resembling TikTok content transformed into gambling products.

Chance has little to do with it.

Developers have understood that a new generation of players no longer consumes entertainment the way they used to. Classic long sessions are progressively losing ground to fast, emotional and immediately gratifying experiences.

What exactly are Instant Games

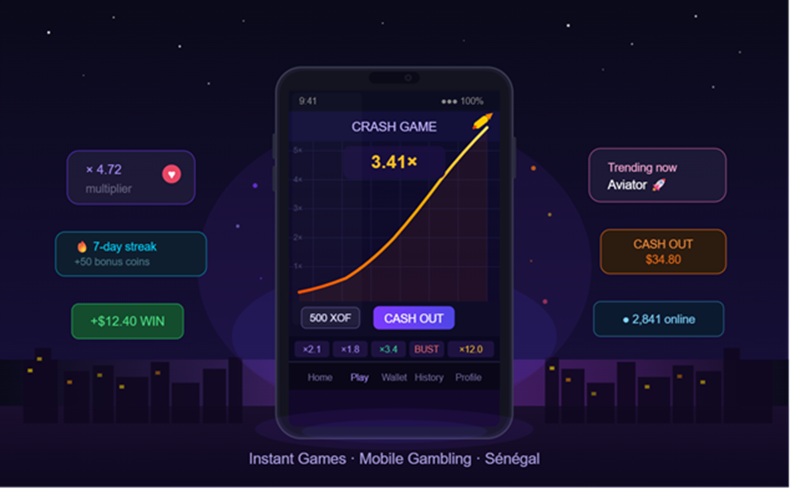

Instant Games are gambling formats designed to produce results extremely quickly.

Unlike traditional slot machines or long poker sessions, these games operate on very short cycles. A round can last just a few seconds before immediately starting again.

Crash games represent the most famous example of this trend. The player watches a multiplier rise progressively until the moment the system “crashes”. The goal is to cash out before this breaking point.

Other popular formats include:

- quick random mini-games,

- instant scratch cards,

- wheel games,

- quick roulette,

- tap-and-win formats.

The central principle always remains the same: reduce the time between action and result.

This structure perfectly matches modern mobile habits where users seek immediate rewards and ultra-fast interactions.

Why TikTok has such a strong influence on modern gambling

TikTok does not only change social networks. The platform is profoundly altering the psychology of digital consumption.

The vertical format, very short videos and rapid emotional loops train users to seek instantly stimulating content. Algorithms reward speed, surprise and emotional intensity.

Online casinos have observed this phenomenon very closely.

Developers now understand that young mobile users often have different attention habits from previous generations. Long waiting phases or slow mechanics become less attractive.

Several analyses show that gambling-related content is exploding on TikTok and similar platforms thanks to big-win clips, emotional reactions and very short formats.

Instant Games reproduce exactly this psychological logic:

| TikTok element |

Equivalent in Instant Games |

| Short videos |

Ultra-fast sessions |

| Continuous scroll |

Repeated game cycles |

| Emotional rewards |

Instant wins |

| Dynamic algorithms |

Unpredictable gameplay |

| Constant stimulation |

Permanent action |

This resemblance is not accidental. Modern mobile gambling mechanics draw direct inspiration from the behaviors created by social networks.

Why young players prefer fast formats

The digital habits of younger generations greatly influence the design of modern casinos.

Mobile users constantly switch between TikTok, Instagram, YouTube Shorts, Telegram and streaming apps. Their digital consumption works in short but repeated sequences.

Instant Games fit perfectly into this behavior.

A quick game can be launched during a break, on public transport or between two videos on a smartphone. It is no longer necessary to commit to a full long session.

Developers therefore seek to maximize:

- emotional speed,

- immediate gratification,

- ease of access,

- visual stimulation,

- mobile interaction.

Crash games illustrate this trend particularly well. Their fast pace and constant emotional tension feel closer to a TikTok feed than to a traditional land-based casino.

This evolution is profoundly changing the very identity of digital gambling.

How platforms optimize mobile attention

Modern gambling is increasingly functioning as an attention economy.

Platforms are no longer just looking to offer games. They attempt to keep the user engaged as long as possible within the mobile ecosystem.

Instant Games are ideal for this because they create extremely fast emotional cycles.

Developers use several techniques inspired by social networks:

- fast animations,

- highly contrasted colors,

- dynamic sound effects,

- frequent rewards,

- instant transitions.

Progression systems and notifications also play an important role. Some platforms now integrate:

- streak rewards,

- daily missions,

- leaderboards,

- limited-time events,

- flash bonuses.

All of this aims to replicate the logic of modern social apps where the user constantly returns for short repeated interactions.

Industry analyses also show that mobile-first now largely dominates global gambling.

Why crash games symbolize this new era

Crash games are probably the best example of TikTok’s influence on gambling.

These formats are extremely easy to understand. Just a few seconds are enough to feel tension, excitement and potential gratification. The emotional loop becomes very intense despite a minimalist structure.

The gameplay resembles almost a short video:

- rapid build-up of tension,

- emotional climax,

- immediate result,

- instant restart.

This dynamic perfectly matches modern digital behaviors based on quick gratification and continuous stimulation.

Crash games are experiencing very strong growth in several African and international mobile markets.

Their success does not come solely from chance or potential winnings. It comes above all from a psychological rhythm extremely compatible with the habits created by TikTok and modern social networks.

Are the psychological risks becoming more significant?

This acceleration of mobile gambling also raises several concerns.

Ultra-fast formats reduce the time for reflection between two actions. Users can chain an enormous number of emotional cycles in very little time.

Digital behavior specialists observe that short and unpredictable content strongly stimulates dopamine mechanisms linked to anticipation and reward.

Instant Games use precisely these psychological mechanisms:

- unpredictability,

- variable rewards,

- rapid tension,

- immediate feedback,

- continuous stimulation.

This does not automatically mean that these games are more dangerous. But their emotional structure resembles modern social networks far more than traditional casinos.

The main problem often comes from speed.

When sessions become extremely fast, some users more easily lose track of time or of the accumulated spending during a mobile session.

This is why discussions on responsible gambling are becoming increasingly important in mobile-first environments.

Why Senegal represents an interesting market

Senegal has several characteristics favorable to the expansion of Instant Games.

The smartphone has become the primary digital tool for a large part of the connected population. Young audiences massively consume mobile content, short videos and social applications.

This digital culture creates an ideal environment for fast, interactive gambling formats.

Platforms are already adapting their interfaces to this reality:

- vertical design,

- simplified navigation,

- short sessions,

- fast payments,

- mobile-first gameplay.

Instant Games fit perfectly in this context because they require little time, little learning and work very well on smartphones.

Senegal thus illustrates a broader global trend: gambling is progressively becoming an extension of modern mobile entertainment.

What the future of mobile gambling might look like

Online casinos will most likely continue to evolve toward even faster and more interactive formats.

The influence of social networks on gambling design now seems impossible to ignore. Developers understand that modern digital attention works differently than it did ten years ago.

The next trends could include:

- native vertical formats,

- personalized AI integration,

- social mini-games,

- interactive live content,

- even more advanced gamification.

The mobile casino of the future may look less like a traditional casino than a blend of TikTok, streaming and social gaming.

Instant Games already represent this transition.

In Senegal as elsewhere, digital gambling is becoming faster, more visual and much more integrated into the daily mobile habits of new generations.

FAQ

What is an Instant Game?

It is a very fast gambling game where results appear almost immediately after the player’s action.

Why does TikTok influence online casinos?

The short, fast and emotional formats of TikTok have changed digital attention habits, pushing casinos to create similar experiences.

Are crash games part of Instant Games?

Yes. Crash games are even considered one of the best examples of this new generation of fast, mobile formats.

Like this:

Like Loading...