In 2018, I wrote a simple post and a Kenyan member of parliament asked to speak with me. I had written that the ordinance which Kenya was trying to approve WeChat Pay in the nation could pose challenges to its banking system:

“The Kenyan banking regulator has run a regulatory regime where market forces are allowed to play. Allowing WeChat and Alipay in Kenya would certainly have real challenges to the Kenyan banking system. Even in China, WeChat has become so popular that local banks are having liquidity problems as what users do is to move their monies from their bank accounts into WeChat, and from there spend as they want. The banks have become pipelines into and out of WeChat and nothing more.

“For the banks, this is a very huge test because if WeChat warehouses lots of cash in its platform, some banks may fold. Interestingly, that is what Alipay and WeChat plan to do”. Kenya changed the structure!

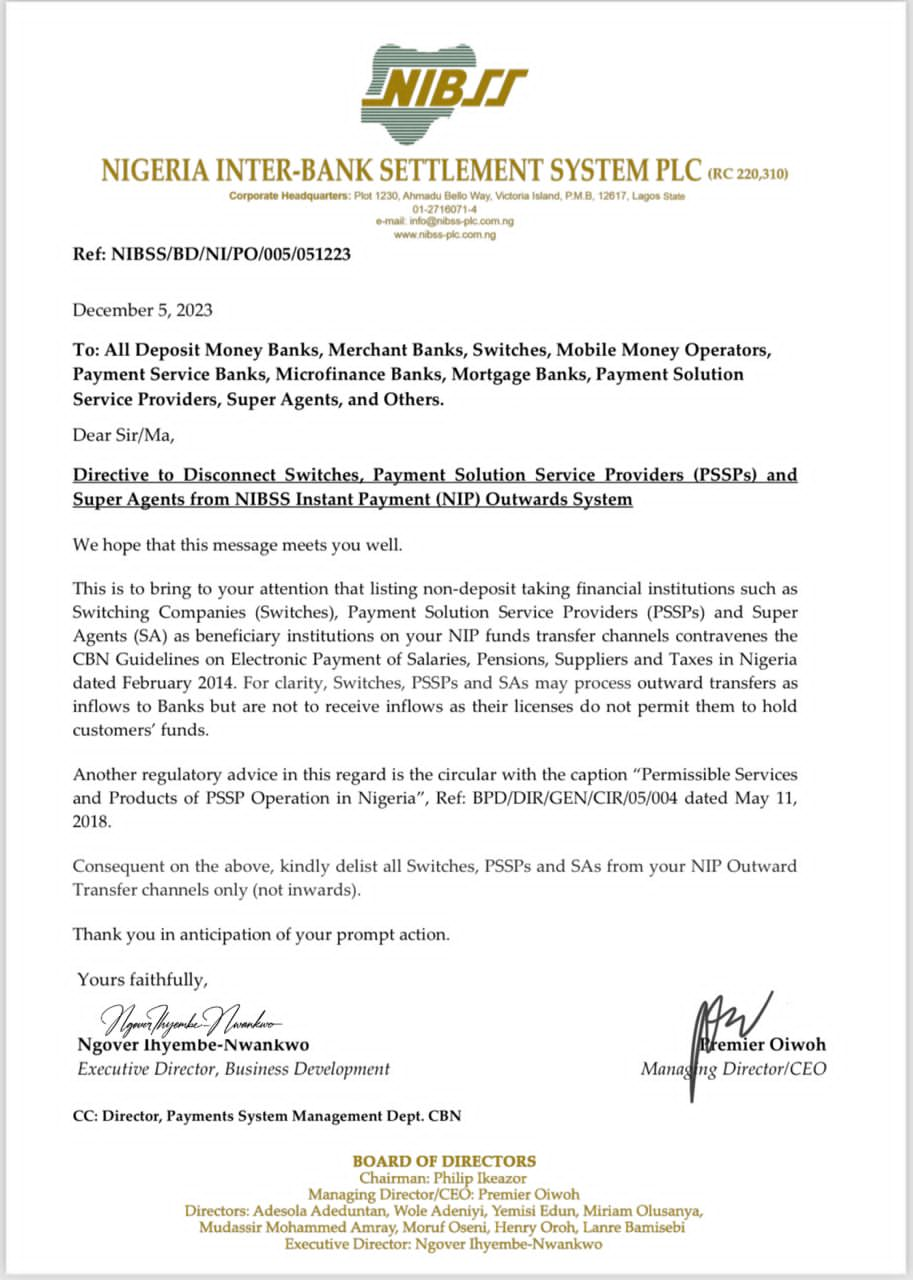

On Dec 5, 2023, the Nigeria Inter-bank Settlement System (NIBBS) sent a circular, and asked for switches, superagents, and payment solution service providers, to be disconnected from the NIBSS instant outward payment system. NIBBS noted that these companies are “non-deposit taking financial institutions”, and by implication should not “hold customers’ funds.”

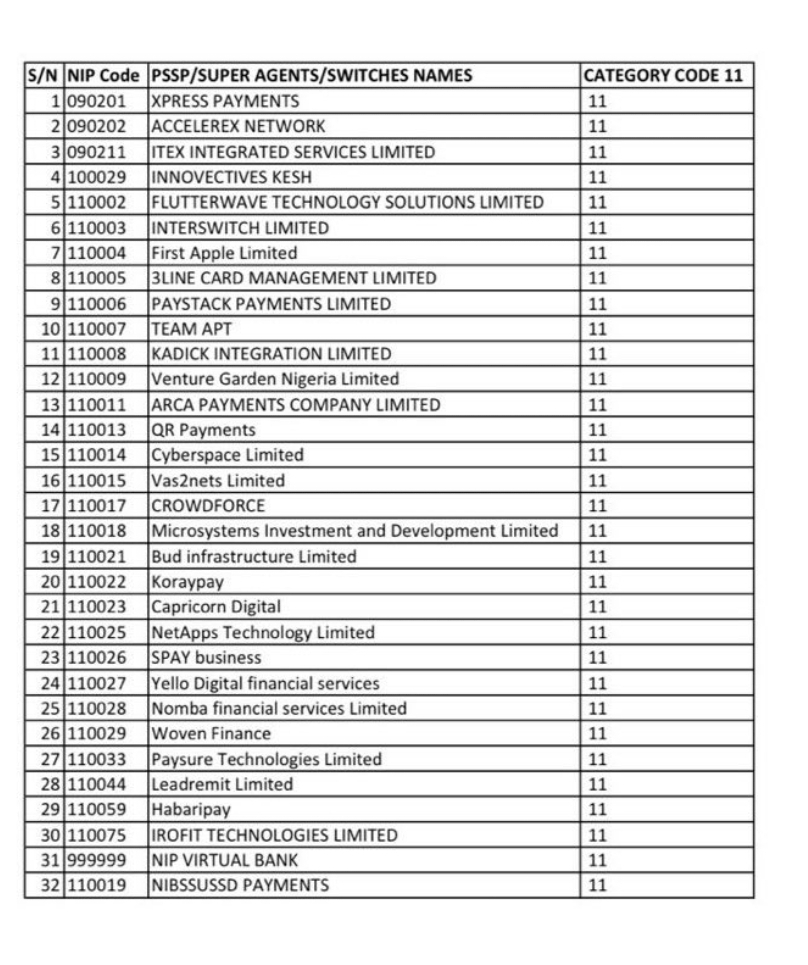

The next day we received a list of companies which are alleged to have contravened this policy. Simply, most of the major fintech companies in the payment space are affected.

Good People, while these fintechs are not the real culprits, but if you are paying attention you will notice that Nigerian banking is under stress despite the “huge profits” they declare yearly. Those profits are vapour-profits, powered by mindless fees on customers and FX-anchored arbitrages. When it comes to real banking, which is interest-anchored banking, Nigerian banking has disappointed.

And that disappointment is evident as there is no catalytic project in Nigeria which any bank can come and claim that it funded. In America, banks tell you dams, bridges, etc they financed and challenged Americans to support them so that they can finance the future for shared prosperity and progress.

Why are banks under stress? It has to do with the aggregation business model. These fintechs which have figured out how to aggregate users are capturing value, making it challenging for banks. In other words, one fintech handles $14 billion monthly in Nigeria and if a huge part of that stays in its wallet, that is money not for the banks to lend. It is key to note that Nigeria’s largest financial institution does not have a bank license; it is a fintech aggregator which delivers APIs which millions of users use to collect payments.

And the big one, when these startups operate, they stay at the edges of the smiling curve where they capture value. What that means is clear: they can quickly improve gross margins at a pace banks which fund the foundational stacks cannot.

So, in the end, the government wants to help the banks, to ensure the deposit funds stay with them so that they can fund businesses via loans. This is not a new policy across nations; in small regions in China, fintechs are mandated not to allow funds to stay more than 3 days in wallets without moving them to banks. China did that to save many small banks which were running into liquidity problems due to WeChat and AliPay.

It does seem like Nigeria just woke up. Yet, this should not affect these fintechs as their business models are not built on lending. So, not holding the customers’ funds will not derail them at scale.