Over $3B worth of bitcoin has been removed from exchanges in the last month. People are waking up after the FTX exit scam. In March 2022, the FTX Exchange announced that it was expanding its operations into the European market.

FTX obtained a license to operate in Europe by partnering with a Cyprus-licensed financial company called K-DNA Financial Services, LTD. According to FTX’s regulatory disclosures page:

FTX Europe’s domain is approved through K-DNA Financial Services Ltd., a duly incorporated Investment Firm in Cyprus that is passported to the European Economic Area. FTX is a brand operated by K-DNA Financial Services Ltd. and regulated by the Cyprus Securities and Exchange Commission, with license number 273/15.

At first glance, this might seem to be an ordinary transaction. After all, it would make sense to team up with an already-licensed firm rather than creating a new company and going through the entire regulatory process from scratch. However, it turns out that K-DNA Financial Services was no ordinary financial firm.

Prior to its purchase by FTX, K-DNA was one of many companies involved in one of the largest financial fraud schemes in recent history: the binary options industry.

BINANCE CEO: SBF is one of the greatest fraudsters in history and a master manipulator of the media. CZ-Binance wrote a long Twitter thread explaining the wrong narratives he’s seen recently.

A list of wrong narratives I have seen recently.

— CZ ? Binance (@cz_binance) December 6, 2022

BLOOMBERG, knew the FTX situation MONTHS before as Marc Cohodes AlderLaneEggs handed them the info. They REFUSED TO PUBLISH it, saying: “It wasn’t good for the business. People got fired. FTX is paying a lot for ads.”

What are binary options, and how are they tied to fraud?

Binary options are an investment product that enable traders to bet on yes-or-no outcomes. For example, a trader could buy a binary option stating that the price of a certain stock will go up 5% or more in a day. The option has pre-determined payout odds and does not involve the trader taking a direct position in the underlying assets, unlike traditional options contracts. Binary options have no connection to the underlying asset or event.

A slightly more complex version of a binary option is the “contract for differences” (CFD). Like binary options, CFDs are cash-settled and never result in any delivery of the underlying security. Unlike binary options, the payout or loss on a CFD tracks the price movement of whatever the underlying asset might be. Consequently, the payout or loss on a CFD is uncapped.

Both binary options and CFDs are generally illegal in the United States due to the obvious potential for abuse. However, a massive binary options industry operating in Europe has flourished for well over a decade. Many of the firms in the binary options space originated in Israel. By the mid-2010s, the binary options industry employed thousands of people multiple countries and generated annual revenues in the hundreds of millions of dollars.

In 2016, a bombshell exposé by The Times of Israel revealed that many binary options firms were engaging in consumer fraud. Operating massive call centers reminiscent of a scene from The Wolf of Wall Street, the firms would cold-call people across Europe and use high-pressure tactics to convince their marks to try trading binary options products. If investors later tried to withdraw their deposited funds, the firms would stall them or, in some cases, simply abscond with the money.

The binary options industry also has ties to one of the biggest corporate scandals in Europe. Wirecard, a payment processing company that became the darling of the German stock market, collapsed after the company’s frauds were exposed. Wirecard functioned as a money laundering service for a number of different criminal enterprises, including the binary options industry.

After a series of reports by The Times and other outlets, in 2017 the Knesset responded by outlawing the entire binary options industry in Israel. However, binary options-style scams have continued to flourish throughout Europe, frequently operating out of Eastern European nations with limited regulatory capabilities.

Sam Bankman-Fried dictating terms to a Congressperson is just incredible.

Ben Armstrong tweeted, There are so many names with the most ridiculous history all related to one another via poker scandal, and now they’re all here running this industry. Dan will pay in due time, there’s some very intriguing info and incriminating data on Mr. Friedberg. However, the smaller fish must fry first, then we’ll take down the big tunas and serve their salty secrets for the world to taste. It’s gonna be like playing a game of human dominos.

If you haven’t figured it out yet, Dan Friedberg created the FTX scam.

Ultimate Bets 2.0.

We need @phil_hellmuth to spill what he knows about his former lawyer

— Bitboy Crypto (@Bitboy_Crypto) December 1, 2022

Also, where did Alameda Trabucco disappear too? It’s amazing how he “retired” an “stepped down” from Alameda Research just months before this meltdown.

SBF confirmed that users on FTX was just trading “notional” assets when asked by Cryptomanran. Which means none of it was real and funds was stored “elsewhere”. Isn’t this the same as the QuadrigaCX scam where the founder ended up “dead”? Ben Armstrong Wrote;

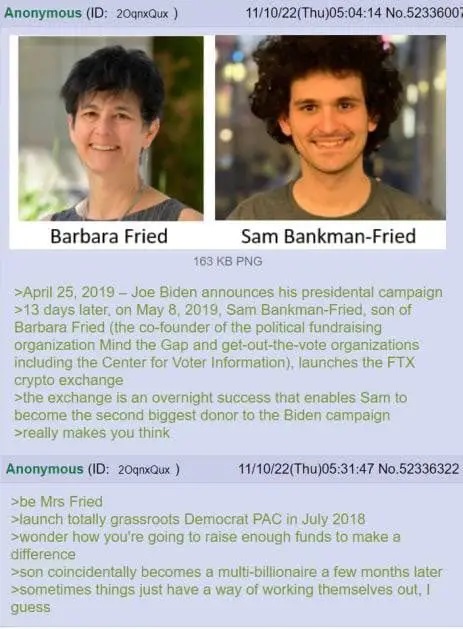

It’s actually pretty sad to watch SBF/FTX. The people behind this scam are Joe, Barb, and Dan Friedberg, Sam has blame. PLENTY. But over time, you are going to find out just how evil Sam’s parents are. They are literally allowing their son to incriminate himself for their benefit.

Sam Bankman Fried talking with Tiffany Fong via YouTube, says he gave just as much money to Republicans but did it via PACs (dark money). He never had a side. He was just trying to bribe enough people to get the scam “crypto” industry regulated by the CFTC.

The Economist recently asked whether “Crypto could be useful for anything other than scams and speculation” post-FTX collapse. We underestimate how much the FTX scandal has now frightened non-tech folks (ex. doctors, lawyers, artists) into thinking all of Crypto and Blockchain tech may be a scam.