When organizations accumulate capabilities, they can put themselves in positions to win. Usually, capabilities help them move from the downstream operations to upstream operations where they can do business and command higher price premiums in the markets. This jockeying requires knowing the best product, and how new products can support it, and how the existing products can seed new ones in future (one oasis strategy). Amazon Web Services was created to support Amazon’s best product (the ecommerce), removing any market demand risk from the strategy. But over time, AWS flourished and became a product even though its core value remains to serve the Amazon’s ecommerce.

In this video, I explain how a Kenyan telecommunication company, Safaricom, is using the one oasis strategy to grow. It has a new ecommerce operation, Masoko, which is leveraging the shops which have served the telecom operator. Through this leverage advantage, via the Safaricom retail shops, Masoko will have more pick-up locations overnight than Jumia. With that advantage, it could become a wonder success overnight because Masoko will not just attract more people to the shops (some will buy things), it will expand the growth of another unit of Safaricom, MPESA, a popular mobile money. As more commercial activities take place in the Safaricom ecosystems, it will become more resilient to overcome whatever the banks are plotting against it.

In your business, you need leveraged scaling, which taps into your existing capabilities, to grow.

Yesterday, I received an email from one of the young people I have mentored. His MBA application was not successful. This is my email to you:

Dear [ ],

I got your phone message on the rejection of your business school application. Certainly, that is discouraging and I understand the feeling. But I am writing to let you know that it should be a past tense, right away. They have rejected your application, the same way they have rejected legends and icons across human generations. The key now is how to continue to make progress in your career and quickly activate alternative options. I will share something I read recently in Forbes for you.

One of the greatest investors of all time, the Oracle of Omaha, could not get into Harvard Business School (HBS). Warren Buffet – who spent two years at Penn before transferring to the University of Nebraska – traveled ten hours to Chicago to interview for a spot at HBS. They rejected him within 10 minutes! Yes, Harvard Business School admission team rejected Warren Buffet.

But there was good news for Mr. Buffet. He was accepted in Columbia and he studied under legendary Ben Graham who pioneered value investing philosophy. That philosophy is the reason Buffet is very rich. And today, you may not have Harvard Business School experience without understanding the Buffet business philosophy. The school that rejected him has built a small business around him.

Pick a copy of Harvard Business Review, you will see how Buffet is celebrated. The same Buffet that was rejected within 10 minutes. I write in HBR and I have used Buffet in many examples. He is a legend and the school that rejected him now celebrates him.

This is not to make you feel good. It is bad when the “first option” is not available. Yes, that was failure, Yet, that is not the end of the journey. You liked MBA while I suggested engineering PhD because the latter offers career insurance: there are always schools to teach if everything goes bad.

MBA is life tool. PhD is a life tool. They are all elements to liberate the mind, and then have a better life. But none is like you – the being and the personality. I do believe that only you can shape the future you want because the best way to predict that future is to create it, they say.

A rejected admission cannot stop that creation process: let this motivate and inspire to be better next time. I do think this could work well. If you decide to try again next year and by the time you arrive on campus, you have another year of work experience. Possibly, upon graduation, you will play at a higher level as you re-enter the labour market.

Finally, note this as a setback. Let us work hard to reduce such in America. Being rejected means that we were not the best, and that has to be worked upon. I have no idea what they look for in MBA admission. You need to find out and prepare better.

I fly into Redmond later in the weekend. I will call you.

I wrote many months ago that Interswitch should buy a bank. But of course, you do not expect any bank in Nigeria to sell. Notwithstanding, that suggestion remains valid, especially now that Interswitch is redesigning itself to become a banking institution that does not need a bank license.

Interswitch should acquire a lending license from Unity Bank. That will help it begin to build a credit system in Nigeria in partnership with NIPSS. Post-acquisition, it will focus on digital banking, closing some branches of Unity Bank and dedicate its efforts to build Nigeria’s first internet-only bank. Through this, the bank will use the data from its ecosystems to perfect lending systems which will help drive it growth.

What Interswitch was doing then, piping data across channels (and not making sense of the data), was simply staying at the bottom of the smiling curve. The value there was extremely low and the business was vulnerable with competitors like Paystack, Flutterwave, eTranzact, Visa and MasterCard emerging. I had reasoned that Interswitch must be bold and take the heat to the real banking sector, if it wants a future in Nigeria and Africa.

I got heat on LinkedIn as some people in the community noted that competing with its main partners, the banks, would affect its core business. Some of the views made in the community were solid. Nevertheless, Interswitch was certainly going to struggle if it did nothing, relying on its traditional business. Yet, even the business with the banks could not be assured.

The New Interswitch

There is a new Interswitch in town and that company is designed to feed on data. I had noted that the new vision is the beginning of a new era in retail banking in Nigeria. Simply, despite what some thought about competing with banks, Interswitch did not mind: it wanted to get into the sector because it wanted to have a future.

In the Nigerian financial sector, Interswitch has moved upstream and is extremely positioned to control most elements of the financial systems with the data it controls.

The internet business is not necessarily who generates the most data. It is who can make sense of it. Aggregators like Interswitch are at the centers making sense of all the data passing through the financial system

[…]

I am so happy for this Interswitch strategy. I wrote many months ago that it should buy Unity Bank to get into lending. It has simply done it in a better way without spending any money. Also, it is not taking any risk

The New License

But instead of being a passive player, allowing people to make money using its channels, Interswitch has obtained a super-agent license from the Central Bank of Nigeria. You can read that as “super agency banking” without a bank license. When you talk of fintech, Interswitch is at the Tier 1 in Nigeria. It is the category-king in an industry it pioneered many years ago.

A commercial Super-Agent licence has been granted to Interswitch Financial Inclusion Services (IFIS), a subsidiary of Interswitch Group, by the Central Bank of Nigeria (CBN)

[…]

Trading as Quickteller Paypoint, IFIS aims to increase the availability of digital financial services in financially-excluded locations in Nigeria from 44 per cent to over 70 per cent in five years.

{…]

Its value proposition cuts across entrepreneurs, artisans, small shop owners, traders, supermarkets, trade associations, retail chains, government agencies and service providers

Yes, Interswitch is now working to “increase the availability of digital financial services in financially-excluded locations in Nigeria”. This means, it is essentially running agency banking service. If you marry this license with the Interswitch Lending Service, you have a new player in the retail banking sector in Nigeria. There is no need to do this through a bank anymore: Interswitch is now the boss. And that is why this is exciting.

One of the most important companies in Nigeria in the area of digital banking is Interswitch. Interswitch is now taking action to take advantage of its position in the sector and lead the acceleration of what Paylater and Piggybank are doing. The Nigerian digital payment pioneer is working with six banks and three startups to begin a new era in Nigerian banking sector. The banks will provide the data while the startups will help deliver the products. Interswitch will stay at the back to make sure the data integrity is there. It will also over time build the credit score. The product is named Interswitch Lending Services (ILS). ILS is a very powerful product in the Nigerian financial sector which can bring many citizens into the sector through micro-lending and financial inclusion.

With this new license, the evolution into retail banking services without a bank (and the associated regulation) is on track. Reading the piece from the Guardian, Interswitch has practically focused its energy on areas the banks could have traditionally gone.

Shop owners or existing businesses can earn additional income by adding an array of payment services to their existing bouquet. Commercial and microfinance banks, Telcos, Cable TV providers, Betting companies, Discos, Insurers, Government Agencies etc can deepen penetration for their business by expanding into communities that hitherto, were relatively unreachable

If you can get these companies across the noted sectors through super-agency license, it means the path to retail banking operation has been paved. The only thing remaining is taking customer (direct) deposits. But that may not be necessary: most customers have balances in their digital wallets, without moving them to their bank accounts, and that is money that can be deployed, until the customer ask for it. I have seen PayPal paying small interests to make customers leave the money in their wallets. In other words, PayPal is “deposit” taking without actually asking for deposits: Interswitch can execute such in Africa.

All Together

Interswitch has accumulated capabilities in the digital payment sector over the last few years. Now, it is unleashing that data, creating new products. Interswitch has the capability to change the basis of competition in the Nigerian banking sector. That will be transforming and disruptive. The data business is at edge of a smiling curve and is just getting started. When companies accumulate capabilities, they see themselves operating in the segments of markets with higher value (usually upstream) compared with where their lower-end competitors operate (usually downstream). In the Nigerian financial sector, Interswitch has moved upstream and is extremely positioned to control most elements of the financial systems with the data it controls.

I am predicting that by 2022, Interswitch Bank Nigeria Limited will be born, and it will be a full online-only banking institution. By having a bank license, it will settle, originate, clear, in-bound, and execute directly many transactions without needing a bank partner. Visa and MasterCard are major competitors, vigorously participating in the sector which Interswitch pioneered in Nigeria. To make progress, Interswitch needs to find new ways to grow.

The unbanked, people/entities yet to be in the financial system, are opportunities. However, most of them may not be hugely profitable. It costs money to serve some poor people and that is why charities do excel in that call. So serving the unbanked alone will not be catalytic: a banking license will unlock more value going forward, and help Interswitch build a virtuoso vertically integrated business. Interswitch Bank Nigeria Limited is on the way. I do think it will lead the movement to build the first pan-African product that will be agnostic of currency and location.

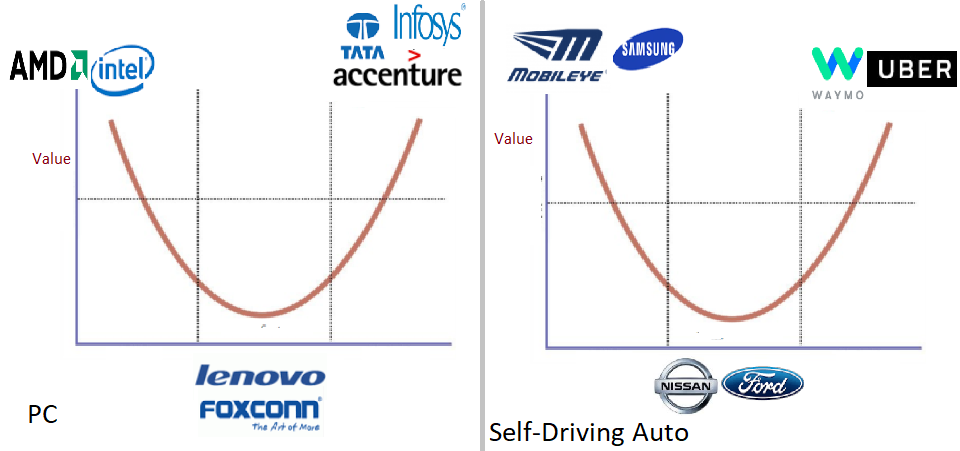

In this video, I explain how value is shifting from the traditional car manufacturers to the companies which are “retrofitting” cars to become driver-less vehicles. When Uber and Waymo receive cars from companies like Nissan and Ford, they take them through engineering processes, turning them into driver-less cars. Systematically, the value now moves from Nissan and Ford to the final products made by Uber and Waymo (this applies even as Uber and Waymo are not selling the cars to the mass market).

If the traditional car companies do not evolve, they will become like PC manufacturers who saw their margins tumble even as chip suppliers like Intel, and IT services firms like Accenture continue to improve margins. Simply, when Toyota Yaris leaves Toyota garage, it could be worth $10,000. But when it has been converted into an autonomous driving car in say Apple facility, it could leave garage at $15,000. Apple could have bought it at $10,000 delivering a margin of say $1,000 to Toyota while it has created an extra value of $5,000 from which it commands a margin of $3,000. The implication is that value has shifted from Toyota to Apple, just as we experiencing in the PC market.

Smiling Curves (PC and Autonomous Auto)

The capacity to do this transformation, by the traditional car companies, cannot be easily captured in typical ranking by management think tanks that look at systematic order in management processes. The Drucker Institute released one ranking few days ago, and it ranked companies like GE and P&G high up there. GE is in a mess right now, but the old management system may still be working. However, Uber may be off the chart, in the ranking, but that does not change where the value is being created at the moment. In other words, being run very well may not be enough, entrepreneurial vision will be necessary, as Jack Ma noted this week. Fortune Newsletter said it brilliantly, thus:

The Drucker Institute, set up to advance the thought of management guru Peter F. Drucker, put Amazon at the top of its inaugural list of the U.S.’s most effectively managed companies. The methodology is based on 37 different rankings including patent registrations and employee reviews on Glassdoor, which explains why companies in the news for chronically falling revenues (IBM) or poor shareholder returns (P&G, GE) fare surprisingly well in the list.

Today, we are opening our franchising opportunity across Africa for people and entities to use Zenvus Boundary to serve their farming communities. We have piloted the administration of this service and the outcome is superb. So, we are scaling the service to the whole African farming market.

Beginning immediately till January 17 2018 [extended to give people time after the long holiday], we are looking for proposals from makers, entrepreneurs and entities that want to build on top of Zenvus Boundary (not Zenvus sensor; that one is coming later). Essentially, you will work with governments, cooperatives, micro-finances, banking institutions, farmers etc and use our technology to map farmers’ boundaries [you decide your market; we want to see from your proposal]. We have reduced the cost of mapping by a factor of 50 through technology.

Zenvus is an intelligent solution for farms that uses proprietary electronics sensors to collect soil data like moisture, nutrients, pH etc and send them to a cloud server via GSM, satellite or Wifi. Algorithms in the server analyze the data and advice farmers on farming. As the crops grow, the system deploys special cameras to build vegetative health for drought stress, pest and diseases. Our system has the capability to tell a farm what, how, and when to farm. It has in-built GPS, compass and accelerometer making it possible for a farmer to map the boundaries of his/her farm which could be useful during loan and insurance applications. One of the solutions available in Zenvus is Zenvus Boundary.

Login into Zenvus Boundary Partner Account

Zenvus Boundary maps farm (land, home, office or any landed property) boundaries and populates them via GIS on Google Map where the survey maps can be printed in our portal. And when done, register with their cooperatives which help them ratify the boundaries with governments. We use this to formalize farmlands and enable financial inclusion. Below is a sample result which the farmer can take to a bank as collateral for loans, after ratification by the local government..

How To Apply

Send us a one page document explaining why we should select you/your entity as a partner in the specific region in Africa where you want to cover [we want to see your scaling strategy. That means how you will get services to map boundaries of farms. Are you going to meet farmers one by one or would you approach a government, NGO, etc to pay you to do so for farmers?]. Your requested geographical coverage cannot be more than a state even though you can start from a state and expand. But at this point, we want you to specify the same or a part of a state you want to focus.

You will use our technology to support farmers in the digitization of their farmlands. We will take a very small commission from your charges to farmers or whoever is paying for the farmers. Also, you will be required to pay a small franchise membership fee (if we select you). Please we want you to see this as an investment, and that is why we are imposing the fees.

Application Deadline: Jan 7, 2018

Email to send application: zenvus@fasmicro.com

We will (privately) announce the selected entities on Jan 15, 2018. Selected partners will automatically join the Zenvus Developer Community.