The President of Nigeria has signed the 2018 Nigeria budget. This is the breakdown of the signed budget, according to Premium Times. You can refer to the 2017 Nigeria’s federal budget here.

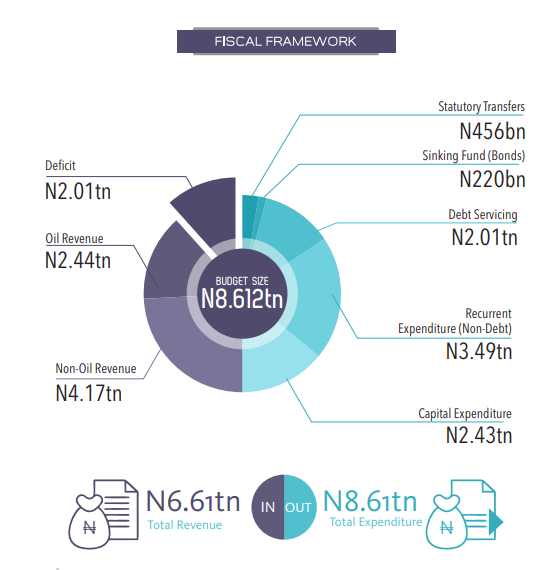

The total budget is N9.1 trillion, up from the N8.6 trillion estimates he submitted to the Assembly on November 7, 2017. The National Assembly raised the total figure by N500 billion.

They also increased the oil benchmark proposed by the executive from $45 to $51 per barrel.

The Assembly, however, retained oil production volume proposed at 2.3 million barrels per day and an exchange rate at N305 to $1.

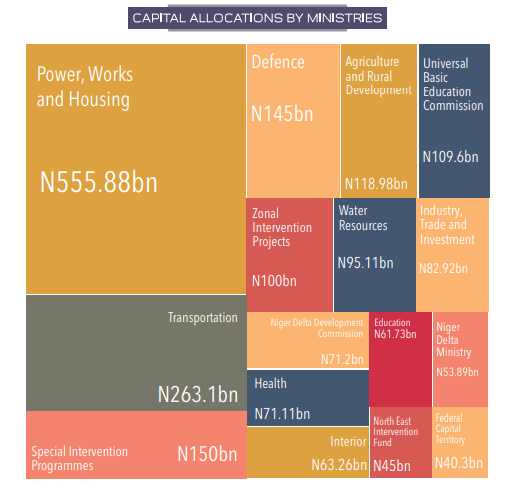

The budget as passed by the two chambers also has N530.4 billion as statutory transfer; N2.2 trillion for debt service; N1,95 trillion as fiscal deficit.

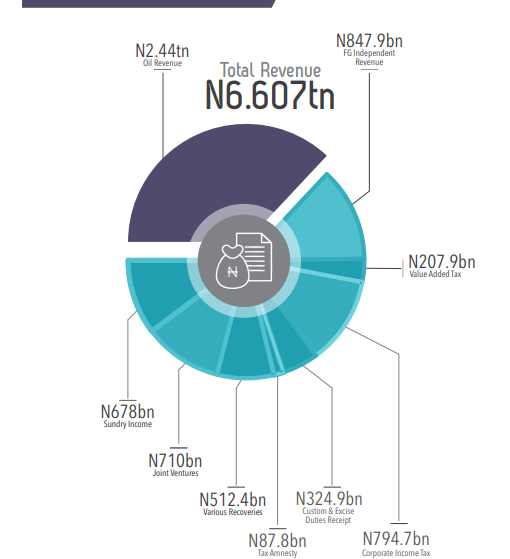

Notice that the official rate of Naira to $1 is N305. The full proposed budget before the National Assembly added the N500 billion is here (pdf).

2018 Nigeria Budget (source: BudgIT). Note this plot did not capture the additional N500 billion added by the National Assembly.

General Electric (GE) fades. The Dow is replacing the iconic American conglomerate with Walgreens Boots Alliance. Yes, the GE Management Factory seems to have stopped working as the paralysis continues with no break.

S&P Dow Jones Indices announced on Tuesday that the iconic maker of light bulbs and jet engines will be replaced in the 30-stock index by Walgreens Boots Alliance. GE was an original member of the Dow in 1896 and has been in it continuously since November 7, 1907.

Being ousted from the Dow is the latest indignity for GE, which is dealing with a serious cash crisis caused by years of bad deals. GE has replaced its CEO, slashed thousands of jobs and cut its coveted stock dividend in half.

The decline of GE should teach us a lesson on management. At its peak during the golden years of Reginald Jones and Jack Welch, GE was the management factory where American companies went to hire their leaders. That was then – a really long time indeed as GE needs vision with the fierce urgency of now.

GE used to be the gold standard on the development of management systems and processes. At its zenith, GE was known as a factory where some of the finest business leaders were incubated, nurtured and prepared for leadership. With peerless business management and training systems, GE supplied a generation of CEOs to corporate America. The company pioneered and scaled many industrial age management systems and sold them across the world. One of those systems is the Six Sigma: Six Sigma was invented in Motorola, GE through its former leader, Jack Welch, popularized it when the company adopted it. As Toyota perfected its Kaizen and Japan pursued Total Quality Management, GE gave America management systems for growth and success. But that was the old GE; the present GE is sick

Today’s GE is using the management principles of the industrial age conglomerates in knowledge-based economies. For a company that prides itself as a center of management systems to fade in this way is unfortunate. The implication is that GE may be out of sync with the tenets of modern business processes. The industrial age has passed, and now it needs to learn what works. The strategic mistakes over the last ten years have been constant, and if GE does not stop making them, this iconic American company may go.

As GE makes way, Amazon, Alphabet (parent of Google) and Alibaba are pioneering new models of conglomerates. These new breeds are not called industrialized conglomerates but digital conglomerates. They do not require huge capital (relatively) and they are built on platforms which generate moats through network effects and positive continuum of the winner-takes-all. They could have taught GE some things but GE was far with its own disappearing world.

Yes, as the dawn of the knowledge economic systems was evolving, GE was selling its financial services to invest deeper in the old business of power generation and turbines. With solar and digital systems, most of those big pockets power turbines are “disintermediated” and that is partly why GE is struggling. Who needs a power plant with capacity of 4,000MW when you can get pieces of 1MW of solar plants across the country? Without those big huge contracts, the business model of GE was affected, and with the cash cow financial services already gone, GE was left bare.

The company would be back but it is certainly not going to be as powerful as it was. But no matter what, it needs to send its managers to Alibaba, Amazon and Alphabet for the modern management tutors, structured for the 21st century markets. Whatever GE Management Factory has been teaching in the last ten years is not working – it needs to update its curricula. No matter how you see it, GE needs to update its management curricula!

I was still in secondary school when Diamond Bank introduced its peerless and highly acclaimed Diamond Integrated Banking System (DIBS) in early 1990s – a solution that made it possible that you can operate your bank account irrespective of the domicile. Before DIBS, in a world dominated by First Bank, Union Bank and defunct Afribank, if you have an account in Aba and you happen to be in Lagos, to get your money, you must physically return to Aba branch of the bank.

For most businesspeople, there was no need of running bank accounts; they moved with their Alvan Ikokus. As Lomaji Ugorji helped us in his memorable adverts for defunct Equatorial Trust Bank, going to a bank was only possible if you could go with your mat. Yes, spending a whole day – 6 hours – to get money from your account was typical.

As I have written, DIBS reduced armed robbery along Onitsha-Lagos road more than any effort put by the Nigerian Police. How? Merchants would open accounts in Diamond Bank Onitsha branch. They would travel with their cheque books to Lagos. Reaching Idumota and Alaba, they would go to the bank’s branches to collect their monies. Magically, robbers who robbed luxurious buses like Young Shall Grow and Chisco which used to carry tons of cash would not find cash! With success factor very low, many criminals exited the routes at scale.

Human-Platform Banking

I really love this bank; I worked in Diamond Bank. It is a matchless institution when I was there. I was extremely motivated to work in the bank because it was extremely innovative. That was the only interview I ever attended in Nigeria and the only job I applied post-graduation. The other job offers came without interviews typical for class best graduating students in Federal University of Technology Owerri. I remain thankful they hired me.

Fast-forward, the bank is at a new game: human-platform banking. People call this agency banking. That is fair, but for me, it goes beyond agents if you read one of the key components of the CLOSA account (the bolded section below).

“Part of our activities in this space include the development of products such as the BETA and CLOSA accounts. BETA targets market traders and also supports small and medium enterprises (SMEs). The BETA account employs agents (called BETA friends) who go to the areas of comfort of these market traders and offer them all the financial services they need without impacting on their way of life, whilst the CLOSA account was created for those without Banks in their areas. People of influence in the community were selected to act as agents of the bank to ensure trust and those in the community were assured that the Bank would assume responsibility for their money once it was deposited with the agents.” Diamond Bank

In most parts of the world, you would build digital platforms to build that intermediation between partners (see my Aggregation Construct). But in Nigeria, we are way behind on the enabling infrastructures and elements for such. Yes, many of our citizens are not yet in digital ecosystems. So, to fix that problem and drive financial inclusion, the bank is seeding the human equivalents of those digital platforms. The “people of influence” like headmasters, imans, and local preachers would become the platforms between the bank and their customers.

All Together

Diamond Bank redesigned Nigerian banking with technology by inventing DIBS, a perception product as I have noted many times. It wants to re-invent it in a new way. With this human element, pioneering at scale human-platform banking, the agency banking will pick up massively.

Agency banking with proprietary technology supported with tokens, phones, BVN and mobile kiosks will deliver the magic. The transactions will be capped to avoid fraud and risk-management tools embedded. As these agency banking systems mature, banks can close and sell off expensive branches which may not be necessary in 5 years as the immersive digital economy evolves.

The path to onboard many Nigerians into the financial systems would involve reaching them at the levels they are, right now. It may involve thinking less of bytes and more of atoms. Yes, human-platform banking over digital-platform banking.

China funds a project. Many Chinese come to town. They have tons of money to spend. Then local companies begin to look for payment systems which can support them. From New York City where AliPay has been implemented (to support Chinese tourists) to Kenya, there are many elements to the New Silk Road. In Kenya, the Chinese expatriates like Alipay and WeChat, and to meet their needs, Kenya needs to have those two solutions which continue to track wherever Chinese go. In a partnership between Equitel and Red Dot Payments, Alipay and WeChat would be available in Kenya.

According to Finserve’s Managing Director, Jack Ngare, the partnership will see Kenyan businesses benefit from having one more option of accepting payment, which is meant to encourage an increase in international trade. “The key purpose of Equity is to empower businesses. We still believe there’s a lot of room for more payment options to come into this market,” he said.

Alipay founder, Jack Ma, was in Kenya a few months back and hinted at Alipay looking for a partner to do business within the country, we are not sure if this is the result of that hint but the inclusion of WeChat Pay could be pointing us to a different direction.

Once the service goes live, anyone with an Alipay or WeChat Pay account will be able to make seamless payments to Kenyan businesses that will have signed up for the service, through their respective platforms. The long-term plan, according to Equitel, is to allow Kenyans to be able to hold Alipay and WeChat Pay accounts through them and thus facilitate international payments.

MPESA Challenge

This is certainly not good news for MPESA. I do predict that MPESA will lose market share because MPESA is a mobile money solution while WeChat is a living ecosystem with capabilities to do anything you can do online, from shopping to gaming. Yes, MPESA is a payment system; WeChat is an internet operating system (WhatsApp, Facebook, Twitter, and Instagram, all in one).

That feature is why the more the users the better, and that means the best in technology will re-grow even when broken apart provided it has enough users to seed that moment. Over time, there will be convergence. WeChat is the Internet first operating system which practically does everything: WhatsApp, Facebook, Twitter, Instagram, all in one. It is a seed that will keep growing, and breaking it will have minimal impacts, unless you want another name, not WeChat, to do the same thing tomorrow in China.

All Together

The Kenyan banking regulator has run a regulatory regime where market forces are allowed to play. Allowing WeChat and Alipay in Kenya would certainly have real challenges to the Kenyan banking system. Even in China, WeChat has become so popular that local banks are having liquidity problems as what users do is to move their monies from their bank accounts into WeChat, and from there spend as they want. The banks have become pipelines into and out of WeChat and nothing more.

For the banks, this is a very huge test because if WeChat warehouses lots of cash in its platform, some banks may fold. Interestingly, that is what Alipay and WeChat plan to do in Kenya as noted in the quoted piece above: “Kenyans to be able to hold Alipay and WeChat Pay accounts through them and thus facilitate international payments”. Yes, they could enable even remittance and international payments cutting out the banks further. This would be huge and as usual Kenya is testing the limits of what ICT utilities can do in Africa, a key point I noted in a recent Harvard Business Review article.

The interesting thing in WeChat and AliPay is that they are making it easier for users to stay longer in their ecosystems through different solutions, services and products they offer to customers. And if they do just that, the need for the typical banking fades. This is already causing major problems with some small Chinese banks where liquidity has become a challenge.

Specifically on that, the Chinese banking regulator has to request that the BAT( Baidu, Alibaba and Tencent) move funds from their wallets to their bank accounts within 72 hours as local banks were having liquidity issues [yes, that does not help local banks. It only helps the banks where the BAT bank]

I am not sure if you read this ebook – The Geography of Science &Technology Innovation Clusters in Nigeria. It was a project my non-profit, African Institution of Technology, conducted on innovation clusters in Nigeria. The Tony Elumelu Foundation funded it, generously.

Sponsored by the Tony Elumelu Foundation, the Nigeria Innovation Cluster Mapping project is poised to uncover the pockets of industry clusters where companies with similar attributes co-exist in Nigeria. The research will provide government and business community with data and tools for understanding what drives clustering, in every region of Nigeria, and how policy can boost its efficiency. This project will help take guesswork out of innovation policymaking by assisting government to know where innovations are occurring, their forms, and how to nurture them.

Globally, data shows that clusters play major roles in regional job growth, wages and formation of new companies. It is now strategic to develop ways to support clusters because of their impacts on sustainable economic growth. This project will help find an objective, quantitative measure to understand the critical drivers of regional competitiveness with consistently based statistical methods that will help improve the welfare of Nigerians.

After this project, I developed a higher level of confidence on Nigerians. I saw across cities and communities that Nigerians are just as inventive as any other group of people I have met. We met engineers who refined crude oil by building local refineries. We noticed that the “refineries” were usually built between high elevations to prevent the Nigerian Navy in seeing the production smokes.

We met artisans with the minds of Thomas Edison in Aba, Kano and Lagos. We meet Nigerians at different levels of making things. We accumulated data of more than 8,500 entities. It was comprehensive and detailed. But one thing was evident – Nigeria is simply an inventive society. We saw inventions – many of them– but minimal innovations.

It is innovation that brings prosperity; invention is largely an idea, innovation is commercialized idea.

The Geography of S&T Innovation Clusters in Nigeria. The Nigerian Innovative Clusters Project aims to uncover the pockets of industry clusters where companies with similar attributes (structure, location, interest, sector) in Nigeria co-exist. The African Institution of Technology (AFRIT) headed by Dr. Ndubuisi Ekekwe developed and conducted the research for the Clusters Project.

In this cast, I discuss some of the big challenges of inventive societies characterized by so many ideas but little products and services to show for them. I explain why nations must transition into innovative societies where solutions are provided and where human welfare accelerates.